Chapter Four

advertisement

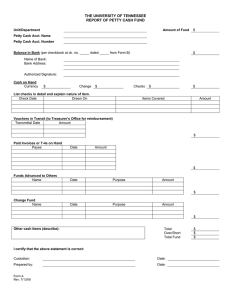

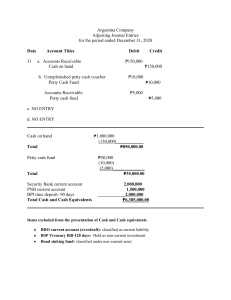

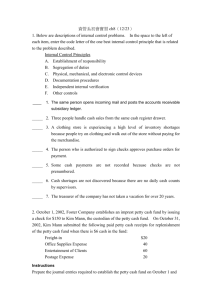

Cash and Internal Control Fraud Triangle STRESS OPPORTUNITY PRESSURE Separation of Duties Physical Controls Proper Authorization Employee Management RECONCILATIONS--- Cash, Inventory, A/R, A/P PERFORMANCE REVIEWS Recording Transactions Sound Personnel Policies BRIEF EXERCISE 4-3 PG 193 EXERCISE 4-4 PG 197 E4-6, 4-7 4-8 PG 197 INTERNAL CONTROL Cash on hand Cash in the Bank Petty Cash Cash Equivalents: anything that turns into cash in 90 days or less : Treasury Bills, 90 day CD CASH SALES Cash receipt = checks, cash, debit card Credit Card = credit card payable not cash BE 4-4 PG 194 E 4-5 PG 197 Bank = -o/s checks +Deposit in Transit Book +interest -bank charges +N/R & interest -NSF Checks +EFT -debit/svc fee Pg 178 Bank Statement CASH ACT –G/L PG 178 Pg 180 Bank Reconcilation Always has a debit (increase) or credit (decrease) to cash Cash Increase is revenue or notes receivable Cash Decrease is expenses, assets or Accounts receivable Pg 181 Do 4-12 Do 4-13 pg 198 pg 198 Petty means small JE for Set up and increase Petty Cash Cash JE to Replenish Expenses Cash Ex 4-14, 4-15 Net income that is backed by cash is more likely to persist into the future than is net income not backed by cash. Operating – Cash inflows, Cash outflows Investing- investing in yourself and others Financing – debt and equity (company’s stock) Direct and Indirect Methods Direct used by CFE – pg 186 illustration 4-11 Indirect mostly used by corporations E4-16 Classifications E4-17 Net Cash Flows Pg 199 P4-2A , P4-3A Bank Reconciliation P4-5A Cash Acct and Cash Flow Statement