NAIS CORE SAMPLES

advertisement

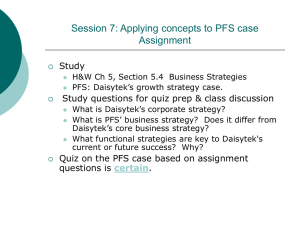

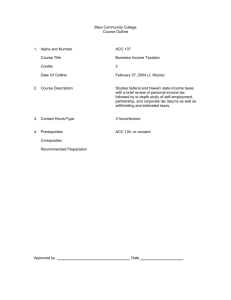

School and Student Service For Financial Aid 2003 NAIS/SSS Financial Aid Workshop Series Mark J. Mitchell, Leslie Bunting, NAIS Margie Nelcoski, ETS Using Tax Returns for Better Decision-Making The avoidance of taxes is the only intellectual pursuit that carries any reward. John Maynard Keynes Copyright National Association of Independent Schools 2003 Why Collect and Review Tax Returns? VERIFY information reported on PFS IDENTIFY unreported resources PROTECT the integrity of your resources and process Copyright National Association of Independent Schools 2003 VERIFY Family income U.S. income tax paid Interest/dividend income Business profit/loss Other – Household size, family members – Alimony paid and/or received – Deductions, medical, dental, child care expenses Copyright National Association of Independent Schools 2003 IDENTIFY Paper losses, other write-offs that mean little to cash flow Unreported and/or underreported assets Items not asked for on PFS Value of assets sold—capital gains or losses Copyright National Association of Independent Schools 2003 PROTECT Ensures accuracy in information Broader knowledge base to support and document objective decision-making Assists responsible distribution of limited funds Recalculate SSS EFC to better represent all information on hand Copyright National Association of Independent Schools 2003 Reviewing 1040 Page One -- Income and Adjustments Lines 1 – 6 – family information Line 7 – wages, salaries Lines 8a, 8b and 9 – interest and dividend income Line 11 – alimony received Line 12 – business income Line 13 – capital gain Line 17 – rental income Line 18 – farm income Copyright National Association of Independent Schools 2003 Reviewing 1040 Page Two -- Taxes, Credits, Payments Certain items here should appear on PFS as untaxed income Line 56 – self-employment tax Line 61 – total tax Line 62 – tax withheld (from W-2) Line 64 – earned income credit; untaxed income Signatures -- be sure they are signed by the right person(s) Copyright National Association of Independent Schools 2003 Schedules A & B Itemized deductions – Cross-check medical and dental expenses shown on PFS #16A – Mortgage interest flag Interest and dividend income – Sources and amounts – PFS #9C – Clarify differences if unexplained Copyright National Association of Independent Schools 2003 Schedule C/C-EZ Sole proprietorship profit or loss DEPRECIATION Consider expenses to identify paper losses, write-offs – auto expenses – meals and entertainment Type and location of business SSS Business/Farm Statement Copyright National Association of Independent Schools 2003 Schedule D Capital gains and losses Short-term vs. long-term Note amount of loss/gain Consider sales price – Represents asset flow – Tax paid based on gain amount not sales amount Tax benefit on losses incurred Copyright National Association of Independent Schools 2003 Schedule E Rental income and expenses DEPRECIATION – Buildings typically appreciate in value – View carefully as paper loss – May refer to items inside the building, as well Cross-check with PFS #19, “All Other Real Estate” Copyright National Association of Independent Schools 2003 Supporting Documents W-2’s to identify personal income, some sources of untaxed income Form 4506 authorizing release of original forms submitted to IRS Form 1065 Partnership return Non-paper filers – Form 8453 – TeleFile worksheet with filer’s confirmation number Copyright National Association of Independent Schools 2003 Complicating Factors Roth IRA, rollovers (Form 8606) Sale of home(s) Partnerships (Form 1065, Schedules K, K-1) S Corporations (Form 1120S, Schedules K, K-1) Children’s taxes, assets (Forms 8615, 8814) Farm assets and depreciation Electronic filing (Form 8453) Copyright National Association of Independent Schools 2003 Highlights of Changes in 2003 Tax Laws Educators’ deduction—up to $250 of out-of-pocket expenses, even if filer doesn’t itemize Taxation rates have been reduced across the board – Fewer taxes paid=more discretionary income Standard deduction raised for married filing joint and qualifying widow – Higher deduction=lower taxable income=fewer taxes paid=more discretionary income Maximum child tax credit increased to $1000 per child (up from $600 per child max) Taxation rates on certain forms of capital gains have been reduced Copyright National Association of Independent Schools 2003 Resources Annotated 1040 and PFS Staff accountant, CPA Guidebooks and IRS publications Tax preparation courses www.irs.gov – Download forms, publications – Highlights, summaries of new tax laws Copyright National Association of Independent Schools 2003 www.irs.gov Copyright National Association of Independent Schools 2003 www.irs.gov Copyright National Association of Independent Schools 2003