Chapter 16

Short-Term

Financial Planning

0

McGraw-Hill/Irwin

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

1-116-1

Key Concepts and Skills

• Be able to compute the operating and

cash cycles and understand why they are

important

• Understand the different types of shortterm financial policy

• Understand the essentials of short-term

financial planning

1

1-216-2

Chapter Outline

• Tracing Cash and Net Working Capital

• The Operating Cycle and the Cash Cycle

• Some Aspects of Short-Term Financial

Policy

• The Cash Budget

• Short-Term Borrowing

• A Short-Term Financial Plan

2

1-316-3

Sources and Uses of Cash

• Sources of Cash

– Obtaining financing:

• Increase in long-term

debt

• Increase in equity

• Increase in current

liabilities

– Selling assets

• Decrease in current

assets

• Decrease in fixed

assets

• Uses of Cash

– Paying creditors or

stockholders

• Decrease in long-term

debt

• Decrease in equity

• Decrease in current

liabilities

– Buying assets

• Increase in current

assets

• Increase in fixed

assets

3

1-416-4

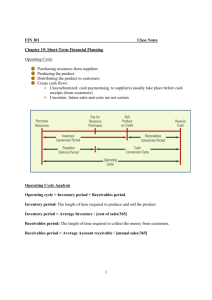

The Operating Cycle

• The time it takes to receive inventory, sell

it, and collect on the receivables

generated from the sale of the inventory

• Operating cycle = inventory period +

accounts receivable period

– Inventory period = time inventory sits on the

shelf

– Accounts receivable period = time it takes to

collect on receivables

4

1-516-5

The Cash Cycle

• The time between payment for inventory

and receipt from the sale of inventory

• Cash cycle = operating cycle – accounts

payable period

– Accounts payable period = time between

receipt of inventory and payment for it

• The cash cycle measures how long we

need to finance inventory and receivables

5

1-616-6

Table 16.1

6

1-716-7

Example Information

Item

Beginning

Ending

Average

Inventory

200,000

300,000

250,000

Accounts

Receivable

160,000

200,000

180,000

75,000

100,000

87,500

Accounts

Payable

Net Sales = $1,150,000

Cost of Goods Sold = $820,000

7

1-816-8

Example: Operating Cycle

• Inventory period

– Average inventory = (200,000+300,000)/2 =

250,000

– Inventory turnover = 820,000 / 250,000 = 3.28

times

– Inventory period = 365 / 3.28 = 111 days

• Receivables period

– Average receivables = (160,000+200,000)/2 =

180,000

– Receivables turnover = 1,150,000 / 180,000 = 6.39

times

– Receivables period = 365 / 6.39 = 57 days

• Operating cycle = 111 + 57 = 168 days

8

1-916-9

Example: Cash Cycle

• Accounts Payable Period = 365 /

payables turnover

– Payables turnover = COGS / Average AP

• PT = 820,000 / 87,500 = 9.4 times

– Accounts payables period = 365 / 9.4 = 39

days

• Cash cycle = 168 – 39 = 129 days

• So, we have to finance our inventory

and receivables for 129 days

9

1-10

16-10

Short-Term Financial Policy

• Flexible

(Conservative) Policy

– Large amounts of cash

and marketable

securities

– Large amounts of

inventory

– Liberal credit policies

(large accounts

receivable)

– Relatively low levels of

short-term liabilities

• High liquidity

• Restrictive

(Aggressive) Policy

– Low cash and

marketable security

balances

– Low inventory levels

– Little or no credit sales

(low accounts

receivable)

– Relatively high levels of

short-term liabilities

• Low liquidity

10

1-11

16-11

Carrying versus Shortage Costs

• Carrying costs

– Opportunity cost of owning current assets

versus long-term assets that pay higher returns

– Cost of storing larger amounts of inventory

• Shortage costs

– Order costs – the cost of ordering additional

inventory or transferring cash

– Stock-out costs – the cost of lost sales due to

lack of inventory, including lost customers

11

1-12

16-12

Temporary versus Permanent Assets

• Are current assets temporary or

permanent?

– Both!

• Permanent current assets refer to the level

of current assets that the company retains

regardless of any seasonality in sales

• Temporary current assets refer to the

additional current assets that are added

when sales are expected to increase on a

seasonal basis

12

1-13

16-13

Figure 16.4

13

1-14

16-14

Choosing the Best Policy

• Best policy will be a combination of flexible

and restrictive policies

• Things to consider

– Cash reserves

– Maturity hedging

– Relative interest rates

• Compromise policy – borrow short-term to

meet peak needs, and maintain a cash

reserve for emergencies

14

1-15

16-15

Figure 16.5

15

1-16

16-16

Cash Budget

• Primary tool in short-run financial

planning

– Identify short-term needs and potential

opportunities

– Identify when short-term financing may be

required

• How it works

– Identify sales and cash collections

– Identify various cash outflows

– Subtract outflows from inflows and determine

investing and financing needs

16

1-17

16-17

Example: Cash Budget Information

• Expected Sales by quarter (millions)

Q1: $57; Q2: $66; Q3: $66; Q4: $90

• Beginning Accounts Receivable = $30

• Average collection period = 30 days

• Purchases from suppliers = 50% of next quarter’s

estimated sales

• Accounts payable period = 45 days

• Wages, taxes, and other expenses = 25% of sales

• Interest and dividends = $5 million per quarter

• Major expansion planned for quarter 2 costing $35

million

• Beginning cash balance = $5 million with minimum

cash balance of $2 million

17

Example: Cash Budget – Cash

Collections

Q1

Q2

Q3

1-18

16-18

Q4

Beginning Receivables

30

19

22

22

Sales

57

66

66

90

Cash Collections = Beg.

Receivables + 2/3(Sales)

68

63

66

82

Ending Receivables =

1/3(Sales)

19

22

22

30

18

1-19

16-19

Example: Cash Budget – Cash

Disbursements

Payment of A/P = 50%

of sales

Wages, taxes, other

expenses

Capital Expenditures

Long-term financing

(interest and dividends)

Total Disbursements

Q1

Q2

Q3

28.50 33.00 33.00

Q4

45.00

14.25 16.50 16.50

22.50

35.00

5.00

5.00

5.00

5.00

47.75 89.50 54.50

72.50

19

Example: Cash Budget – Net

Cash Flow and Cash Balance

Q1

Q2

Q3

1-20

16-20

Q4

Total Cash Collections

68.00

63.00

66.00

82.00

Total Cash Disbursements

47.75

89.50

54.50

72.50

Net Cash Flow

20.25

(26.50)

11.50

9.5

5.00

25.25

(1.25)

10.25

Net Cash Inflow

20.25

(26.50)

11.50

9.50

Ending Cash Balance

25.25

(1.25)

10.25

19.75

Minimum Cash Balance

-2.00

-2.00

-2.00

-2.00

Cumulative surplus

(deficit)

23.25

(3.25)

8.25

17.75

Beginning Cash Balance

20

1-21

16-21

Short-Term Borrowing

• Unsecured loans

– Line of credit – prearranged agreement with a bank that

allows the firm to borrow up to a certain amount on a

short-term basis

– Committed – formal legal arrangement that may require

a commitment fee and generally has a floating interest

rate

– Non-committed – informal agreement with a bank that

is similar to credit card debt for individuals

– Revolving credit – non-committed agreement with a

longer time between evaluations

• Secured loans – loan secured by receivables,

inventory, or both

21

1-22

16-22

Example: Factoring

• Selling receivables to someone else at a

discount

• Example: You have an average of $1 million in

receivables and you borrow money by

factoring receivables with a discount of 2.5%.

The receivables turnover is 12 times per year.

• What is the APR?

– Period rate = .025/.975 = 2.564%

– APR = 12(2.564%) = 30.769%

• What is the effective rate?

– EAR = 1.0256412 – 1 = 35.502%

22

1-23

16-23

Short-Term Financial Plan

Q1

Q2

Q3

Q4

Beginning Cash

5.00

25.25

2.00

10.05

Net Cash Inflow

20.25

(26.50)

11.50

9.50

New Short-Term Debt

0.00

3.25

0.00

0.00

Interest on Short-Term Debt

0.00

0.00

0.20

0.00

Short-Term Debt Repayment

0.00

0.00

3.25

0.00

Ending Cash Balance

25.25

2.00

10.05

19.55

Minimum Cash Balance

-2.00

-2.00

-2.00

-2.00

Cumulative Surplus (Deficit)

23.25

0.00

8.05

17.55

Beginning Short-Term Debt

0.00

000

3.25

0.00

Change in Short-Term Debt

0.00

3.25

-3.25

0.00

Ending Short-Term Debt

0.00

3.25

0.00

0.00

23

1-24

16-24

Quick Quiz

• Suppose your average inventory is $10,000,

your average receivables balance is $9,000,

and your average payables balance is $4,000.

Net sales are $100,000 and cost of goods

sold is $50,000.

– What are the operating cycle and the cash

cycle?

• What are the differences between flexible and

restrictive short-term financial policies?

• What factors do we need to consider when

choosing a financial policy?

• What factors go into determining a cash

budget and why is it valuable?

24

1-25

16-25

Comprehensive Problem

• With average accounts receivable of $5

million, and credit sales of $24 million, you

factor receivables by discounting them

2%. What is the effective rate of interest?

25