Health Care Reform - Employers

advertisement

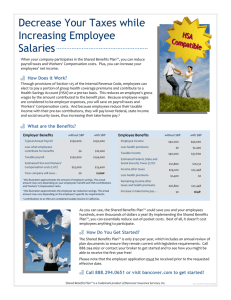

HSAs Health Care Reform Prepared for Oklahoma City Chapter of OSCPA July 16, 2015 1 Beale Professional Services (BPS) owned by Jennifer Beale, Joe Strunk and Guy Strunk Alexander & Strunk, Inc. (A&S) owned by Joe Strunk and Guy Strunk Oklahoma Bar Association - 1955 Oklahoma Society of CPAs - 1967 Association of Oklahoma Nurse Practitioners - 2013 Oklahoma Association of Realtors - 2014 Oklahoma Dental Association - 1972 Oklahoma Association of Optometric Physicians - 1994 3000 Insurance Group (3iG) established by Joe, Jenn and Guy to streamline operations and handle carriers representing multiple associations under one contract. Separately and together, we are independent agencies representing hundreds of insurance carriers and working with many types of businesses, associations, non-profits and individuals, primarily in Oklahoma. 2 Combines an affordable qualified High Deductible Health Plan (HDHP) and a tax-favored Health Savings Account (HSA) Part 1: HDHP – Intended to cover serious illness or injury once the deductible has been met Part 2: HSA – Used to cover small and routine medical expenses until the deductible is met, or used as a savings vehicle for future medical expenses The HSA grows tax-deferred, and if you use your HSA funds for eligible medical expenses, you never have to pay taxes on those funds Any adult can open and contribute to an HSA if they: Have coverage under a qualified “high deductible health plan (HDHP)” Have no other first-dollar medical coverage Are not enrolled in Medicare Cannot be claimed as a dependent on someone else’s tax return 3 Contributions to your HSA can be made by you, your employer and/or any other third party, but the total contributions are limited annually Employer contributions are excludable from income and employment taxes and employee contributions are deductible “above the line” Employer contributions must be made on a comparable basis 4 Withdrawals from an HSA are tax-free provided the funds are used to pay qualified medical expenses (Section 213(d) of the IRC), but only to the extent they are not covered by insurance otherwise You can use the money in the account to pay medical expenses for yourself, your spouse, or your dependent children, even if they are not covered by your HDHP At age 65, unused HSA money can be withdrawn for non-medical reasons without penalty (ordinary income tax still applies) You can generally not use the money for medical insurance premiums, except under specific circumstances, including: Any health plan coverage while receiving federal or state unemployment benefits COBRA continuation coverage Qualified long-term care insurance Medicare Premiums (but not Medicare Supplement Premiums) 5 6 Any amounts used for purposes other than to pay for “qualified medical expenses” are taxable as ordinary income and subject to an additional 20% penalty Examples include: Medical expenses that are not considered “qualified medical expenses” under federal tax law (e.g. cosmetic surgery) Other types of health insurance unless specifically described above Medicare supplement insurance premiums Expenses that are not medical or health-related Upon the accountholder’s death, the assets in the HSA become the property of their named beneficiary Spousal beneficiaries may treat the account as their own Non-spousal beneficiaries must pay ordinary income taxes on the funds If no beneficiary is named, the assets go to the accountholder’s estate 7 Plan Deductible $4,500 ($1,500/person) $12,700 ($6,000/person) Savings Annual Premium $15,047.64 $8,484.60 $6,563.04 HSA Contribution N/A $6,650.00 HSA Tax Savings N/A $2327.50 (@35%) Total Annual Savings Out of Pocket Max Total OOP and Prem and Cont -$4,322.50 $2,240.54 $10,500.00 $25,547.64 $12,700.00 $18,857.10 $6,690.54 8 9 Guaranteed Issue coverage for all ages No pre-existing conditions imposed on anyone Individual Mandate • As of 1/1/2014 most US citizens must have minimum essential coverage (MEC) or pay a penalty. • The penalty fee for not having health coverage is calculated one of two ways: either a flat fee or a percentage of your household income that falls above the tax filing threshold, whichever is higher. In 2015 the flat fee penalty is calculated as $325 per adult and $162.50 per child under age 18, subject to a maximum of $975. The percentage penalty is 2% of household income, subject to a maximum equal to the national average premium for a bronze plan. 10 Exemptions from the Penalty Income-related exemptions The lowest-priced coverage available to you, through either a marketplace or employer plan, would cost more than 8.05% of your household income You don’t have to file a tax return because your income is below the level requiring you to file Health coverage-related exemptions You were uninsured for no more than 2 consecutive months of the year You lived in a state that didn’t expand its Medicaid program but you would have qualified if it had Group membership exemptions You’re a member of a federally recognized tribe or eligible for Indian Health services You’re a member of a recognized health care sharing ministry You’re a member of a recognized religious sect with religious exemptions to insurance, including Social Security and Medicare 11 Other exemptions You’re incarcerated You’re a US citizen living abroad, a certain type of non-citizen or not “lawfully present” You experienced one of the hardships below Homeless Evicted in the past 6 months or facing eviction or foreclosure Received a shut-off notice from a utility company Recently experienced domestic violence Recently experienced the death of a close family member Experienced a natural or human-caused disaster (fire, flood) that caused substantial damage to your property Filed for bankruptcy in the last 6 months Had medical expenses you couldn’t pay in the last 24 months that resulted in substantial debt You experienced unexpected increases in expenses caring for an ill, disabled or aging family member Your individual plan was cancelled and you believe other Marketplace plans are unaffordable 12 Open Enrollment Period The 2016 Open Enrollment period begins November 1, 2015 and ends January 31, 2016. If you submit an application between the 1st and 15th of the month, your coverage will be effective the first of the following month. If you submit your application between the 16th and the last day of the month, in most cases, your coverage will be effective the 1st day of the second following month. For instance, a member who enrolls February 16th will not have coverage until April 1st. Deductibles reset each January 1 When you change plans during the year, deductible resets 13 Special Enrollment Periods Coverage can only be purchased outside an Open Enrollment period if you have a Qualifying Life Event. This period of time is referred to as a Special Enrollment Period (SEP) and provides a 60-day window in which you can make changes or enroll in a new plan. 14 Qualifying Life Events that create a Special Enrollment period include: Getting married Getting divorced Having, adopting, or placement of a child Dependent child reaches age 26 Permanently moving to a new area that offers different health plan options Losing other health coverage (for example due to a job loss, divorce, loss of eligibility for Medicaid or CHIP, expiration of COBRA coverage, or a health plan being decertified). Note: Voluntarily quitting other health coverage or being terminated for not paying your premiums are not considered loss of coverage. For people already enrolled in coverage, having a change in income or household status that affects eligibility for tax credits or cost-sharing reductions 15 Preventive care covered 100% in-network Insurer Fee, Transitional Reinsurance Fee, Risk Adjustment Fee Fees payable by insurance companies and passed on to consumers, sometimes as a separate line item on your health insurance bills. Community Rating, i.e. rates can no longer differ based on gender, health history or claims. Rates are based on geographic location, age and tobacco use. Age factors are subject to a 1:3 maximum premium ratio, with 3 age bands: under 21, 21-63, and 64+ Minimum Loss Ratio (MLR): carrier requirement to spend 80-85% of premium dollars on healthcare. Carriers must provide a rebate or premium credit to customers if they did not meet the MLR. 16 No annual or lifetime limits on essential benefits All plans include coverage for 10 Essential Health Benefits Ambulatory services Emergency services Hospitalization Habilitative and rehabilitative services Labwork services Preventive and wellness services Maternity and newborn services Mental and behavioral health Prescription drugs Chronic disease management Pediatric services 17 18 Eligibility: Household income falling between 100-400% of FPL, AND Employer does not provide affordable coverage that includes minimum essential health benefits, AND Not eligible for Medicare, AND Not eligible for Medicaid In addition to generous premium subsidies, people with incomes up to 250% of poverty also are eligible for reduced cost sharing (e.g., coverage with lower deductibles and copayments) paid for by the federal government. 19 20 What is considered Affordable Coverage? Employer coverage is considered affordable if the employee’s share of the annual premium for self-only coverage is no greater than 9.5% of annual household income. Do I have to register with or purchase coverage through healthcare.gov? If you are not seeking a premium or cost-sharing subsidy, then there is no need to register with or purchase insurance through healthcare.gov. Whether you purchase your next plan on or off the exchange, an agent can help you. 21 Subsidy Eligibility calculator http://kff.org/interactive/subsidy-calculator Apply for Qualified Health Plan on Public Exchange – In Oklahoma, use Federally Facilitated Marketplace (FFM) available at healthcare.gov OR your local agent Advanced Premium Payment or Tax Credit 22 Requirements affecting ALL employers: Effective 10-1-2014: Provide “Notice of Coverage Options” to all employees – applies whether or not group health coverage offered Provide Summary of Benefits and Coverage (SBC) to covered employees Small Business Tax Credit Available to companies with fewer than 25 FTE, average compensation under $40,000 – beginning 1/1/2014, must purchase coverage through a public SHOP exchange in order to apply for the credit 23 Does my employer have to offer health insurance coverage to me? Employers with fewer than 50 FTEEs – No Employers with 50-99 FTEEs – Yes, beginning 1-1-2016 Employers with 100+ FTEEs – Yes, beginning 1-1-2015 Full Time Equivalent Employees (FTEEs) Employees working on average at least 30 hours of service per week. Two Part-time employees each working 15 hours/week = 1 FTEE Ex: An employer has 40 full-time employees working 35 hours/week, 5 parttime employees working 20 hours/week and 5 part-time employees working 10 hours/week. The employer has 50 FTEEs. 24 Can employers reimburse employees for health premiums purchased via an exchange or from an agent in lieu of setting up their own plan? The Internal Revenue Service addresses these arrangements - known as "employer payment plans," in IRS Notice 2013-54. The IRS considers these plans to be group health plans, and when undertaken by an employer who is otherwise required to establish a group health plan and provide benefits to qualified employees, is not in compliance with the ACA. According to the IRS, employers who do this in lieu of establishing a required ACA compliant health plan may be subject to an excise tax of up to $100 per day per employee. This could amount to a tax of up to $36,000 per employee per year, under Section 4980D of the Internal Revenue Code. 25 The IRS recently distributed Notice 2015-17 that allows a measure of relief for some employers from the above excise tax in four circumstances: The plans are 'employer payment plans' as defined in Notice 2013-54, provided the plan is not sponsored by an Applicable Large Employer (ALE) as defined in Paragraph (c)(2) of IRC 4980H (shared responsibility for employers regarding health coverage) and sections 54.4980H-1(a)(4) and -2 of the application. The employer payment plan is an S corporation arrangement for shareholder employees who own 2 percent of the company or more. The arrangements in question are to reimburse employees for Medicare premiums, or The arrangements in question reimburse employees for TRICARE premiums within a health reimbursement arrangement (HRA). Note also that the IRS allows for some temporary relief for small employers (those not designated as ALEs by IRC 4980H) for 2014 and up to July 1, 2015. Generally, this relief will apply to employers with fewer than 50 full-time equivalents in the prior year.) 26