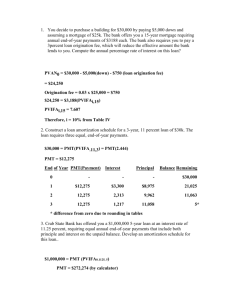

Chapter 6

advertisement

Chapter 6:

Residential Financial Analysis

Incremental Borrowing Cost

– Two loans, one for a greater sum than the

other. How should borrower compare the

alternatives? Calculate marginal or

incremental cost of borrowing.

Loan 1: $80,000, 12%, 25 years = $ 842.58/mo.

Loan 2: $90,000, 13%, 25 years= $ 1,015.05/mo.

$10,000

$ 172.47

IRR?

-10000=PV

172.47=PMT

300 = n

IRR = 20.57% = incremental cost of

extra

$10,000

What if loan is repaid early (say after 5

years)?

Loan 1: OLB after 5 years = 76,523

Loan 2: OLB

= 86,640

10,117

IRR?

-10,000=PV

172.47=pmt

10,117=FV =OLB Differential

60 =n

IRR = 20.83%

If there were origination fees?

Loan 1: 1,600 Fees

Loan 2: 2,700 Fees

IRR? 8,900=PV= {(90,000-80,000)-(2,700-1,600)}

172.47=pmt

300=n

IRR = 23.18%

LOAN REFINANCING

If interest rates fall, should loan be refinanced?

Compare costs of refinancing to benefits or

savings. Calculate IRR or NPV.

Five year old loan ($80,000 orig., 30 years, 15%)

vs. new loan of $78,976.50 (OLB of old loan) 25

years, 14%.

Loan Refinancing (con’t)

Costs = $4,105

Benefits = pmtold - pmtnew

(1011.56 - 950.69= 60.87)

IRR? : 4,105=PV

60.87=pmt

300=n

IRR = 17.57%

NPV = ? depends on borrower’s req’d rate of

return.

What happens if loan is repaid early?

Assume loans were prepaid after 15 years

(old loan) or 10 years after refinancing.

IRR? :

4,105 = PV

60.87 = pmt

889 = FV (OLBold-OLBnew)=(72,27571,387)

120 =n

IRR =

14.21%

What if refinancing costs can be

financed?

1

2

Simply compare new payments (based on

OLB & refinancing costs) to old payment. If

new payment is lower, refinance.

Alternatively, calculate the effective cost of

refinancing.

IRR?: 78,976.50 = PV (loan disbursment)

1,000.10= pmt (OLB &Financed

refinance cost)=(78,976.50+4105)

300 = n

IRR = 14.81%

What if the borrower wanted to

refinance for a lower interest rate,

but wishes to continue making their

current monthly payment? The

impact of this approach would be to

shorten the payback period. Let’s

revisit the first refi example. The

interest rate drops from 15% to

14%, and a refi fee of $4105 is

charged. The original loan had 25

more years (300 months) until

maturity. How long would it take to

amortize the outstanding loan

balance at the 14% rate?

PV= OLB= $78,976.50

PMT= $1011.56

I= 14%

N=?= 208.43months vs. the 300 months

remaining on the original loan

What would the lender’s yield be on the

refi loan?

PV= $74,871.50 = (78976.50 OLB – 4105

refi fee)

PMT= $1101.56

N= 208.43 months

I= ? = 14.99%

Early Loan Repayment: Lender

Inducements

If interest rates rise, lenders would like to

retire old loans. Lender might offer to

discount loan if prepaid.

Old loan $75,000; 8%; 15 years. 10 years

later OLB is $35,348. If current rates are

12% and lender offers to accept

repayment of only $33,348.

What is the return to the borrower?

IRR?: 33,348 = PV (OLB - 2000 discount)

716.74 = pmt (orig. loan pmt)

60 = n

IRR = 10.50% = return on “investment” to

buy back the loan.

Market Value of a Loan

Simple - compute the present value of the

remaining payments at the market

interest rate.

Old Loan of $80,000; 10%; 20 years. Five

years later, the OLB is $71,842. If market

rates were 15% today, what is the loan

value?

PV = ?:

772.02 = pmt

180 = n

15% = i

PV = $55,161 is the “discounted” value of

the loan.

Makes sense if the borrower has the $$ to

pay off loan and the IRR represents on

attractive yield to alternative investments

Effective Cost of Two or more loans:

Situations exist when borrower takes a

second mortgage or perhaps assumes a

loan and needs additional funds.

You wish to buy a property priced at

$115,000. An existing mortgage can be

assumed (OLB=$75,331), payments are

$726.96 and the loan will mature in 20

years. A second mortgage for $16,669

($115,000 x .80 - $75,331) can be obtained at

14% for 20 years. Alternatively, the

purchase can be made with an 80% LTV

loan ($115,000 x .80) at 12% for 20 years.

Is the assumption attractive? IRR of

combined assumption plus second

mortgage?

IRR?:

726.96 + 207.28 = 934.24 = pmt

240 = n

92,000 = PV

IRR = 10.75%, which is lower than cost of

First mortgage financing

(12%)

Usually second mortgages have short

maturities. If the above situation called for

a 5 year second mortgage, would the

assumption make sense?

IRR?:

726.96 + 387.86* =1,114.82 = pmt

*pmt. On 2nd mtg.,i=14% ,N=5YRS

1-5 for 1,114.82 = n

6-20 for 726.96 = n

92,000 = PV

IRR = 10.29%

Wraparound Loans

Used to keep an old (low interest rate) loan

in place. Wrap lender makes loan for an

amount equal to existing loan balance plus

the additional financing required. Wrap

lender pays off old note and borrower pays

off wraparound loan. Can be used in lieu of

assumption and second mortgage in an

acquisition or as a means to borrow

against equity in a property.

$90,000 = OLB old loan (8%, 15 years remaining)

$860.09 = old pmt.

$150,000 = property value

$30,000 = desired new financing

Options:

1. New first mortgage $120,000 at 11.5% for 15

years.

2. Second mortgage of $30,000 at 15.5% for

15 years.

3. Wrap loan of $120,000 at 10% for 15 years.

Obviously the wrap rate of 10% is favorable

compared to a new first mortgage at 11.5%.

Is the wrap better than adding a second

mortgage? Calculate the incremental cost

on the additional $30,000 acquired via

wrap financing. Compare this rate to the

second.

IRR?:

30,000 = PV

429.44 = pmt

(1289.53 wrap loan

180 = n

pmt-860 old loan pmt)

IRR = 15.46% which is slightly lower than

rate on the second.

*

Original mortgagee gets screwed.

That is why the original mortgage

probably disallows further

encumbrances or includes a due-onsale clause.

BUYDOWNS

Seller (often builder) helps buyer

(borrower) qualify for mortgage

financing by “buying down” early

mortgage payments. Used most

often when interest rates are very

high. Often buydowns are executed

with graduated payments for 3-5

years.

Assume buyer seeks a $75,000 mortgage

and current rates are 15%. If loan maturity

were 30 years, payments would equal

$948.33. Borrower can’t qualify at this

payment, but if rate were 13% ($829.65

pmt) they could qualify. Builder/Seller

offers to “buy down” the interest rate from

15% to 13% for the first five years of the

loan.

How much would builder pay lender to

buydown the loan? Calculate present

value of payment short fall $118.68 (948.33

- 829.65) at 15% over 5 years.

PV = ?

PV = $4,988.67

118.68 = pmt

15% = i

60 = n