Coca-Cola mini-case

advertisement

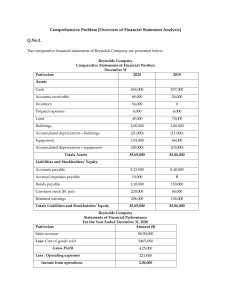

Coca-Cola mini-case Projected financial statements Prospective analysis is the final step in the financial statement analysis process. It can only be undertaken once the historical financial statements have been properly adjusted to accurately reflect the economic performance of the company. As we will discuss in this course, these adjustments may include, for example, eliminating transitory items in the income statement or reallocating them to past or future years, capitalizing (expensing) items that have been expensed (capitalized) by management, capitalizing operating leases and other forms of off-balance sheet financing, and so forth. Prospective analysis includes forecasting of the balance sheet, income statement and statement of cash flows. Prospective analysis is central to security valuation. Both the free cash flow and residual income valuation models require estimates of future financial statements. The residual income model, for example, requires projections of future net profits and book values of equity in order to estimate current stock price. Prospective analysis is also useful to examine the viability of companies’ strategic plans. For this, we analyze whether a company will be able to generate sufficient cash flows from operations to finance expected growth or whether it will be required to seek debt or equity financing in the future. We are also interested in analyzing whether current strategic plans will yield expected benefits. And finally, prospective analysis is useful to creditors to assess a company’s ability to meet its debt service requirements. Assignment: 1. Read WSH chapter 10 on projections. 2. Download the Coca-Cola data set (KO 10Y 10-K.xls). Using this data, and the projection assumptions provided below, prepare a forecasted income statement and balance sheet for 2004. Projection assumptions: Sales growth ......................................................................................................... Gross profit margin .............................................................................................. Selling, general & administrative expense/ Sales ................................................. NOPAT/ Sales ...................................................................................................... Depreciation rate (Depreciation expense/ Prior year gross PP&E) ...................... Interest rate (Interest expense/ Prior year long-term debt) ................................... Tax rate (Income tax/ Pretax income) .................................................................. Cash dividend per share ....................................................................................... Asset turnover—ATO (Sales/ Average net operating assets) ............................... Accounts receivable turnover—ART (Sales/ Average accounts receivable) ....... Days sales outstanding—DSO ............................................................................. Inventory turnover—INVT (COGS/ Average inventory) .................................... Days inventory outstanding .................................................................................. PP&E turnover—PAT (Sales/ Average PP&E) ................................................... Accounts payable turnover—APT (COGS/ Average accounts payable) ............. Days payables outstanding ................................................................................... Working capital turnover—WCT (Sales/ Net operating working capital) ........... Capital expenditures/ Sales .................................................................................. Taxes paid rate (Tax payable/ Tax expense) ........................................................ © 2003 by Robert F. Halsey 7.56% 63.1% 31.5% 21.8% 9.4% 2.3% 20.9% $0.89 1.01 10.05 36.32 6.10 59.86 1.17 2.00 182.22 7.16 3.4% 0.80