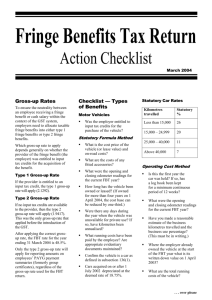

Streamlining the taxation of fringe benefits

advertisement