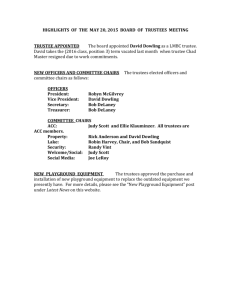

trusts - UVic LSS

advertisement