Incomplete Records - St Kevins College

advertisement

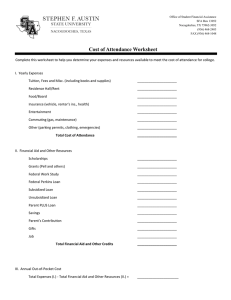

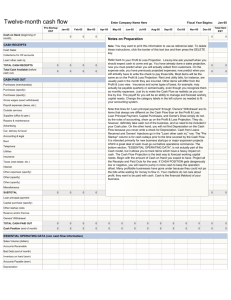

Incomplete Records Aim: To show how an accountant can prepare the Final Accounts of a Sole Trader from minimal unfinished information There are three main forms of Incomplete Records Questions: 1. Cash Book Method: here you have some starting information, some payments and receipts made, usually a loan to handle, and some of the information from the closing Balance Sheet. The secret to doing the question in the time available is to lay out the question in blank form and fill in the information/figures as they are found. You start by doing 6 roughwork T accounts Opening Balance Sheet to calculate Goodwill (the value put on the reputation of the firm, ie the difference between what the firm is worth and what was actually paid for it) 1. Cash Account to find Cash Sales (since we spent lots of cash, it must have come from Cash Sales) 2. Bank Account to find the Closing figure for Bank to go into the Balance Sheet 3. Debtors Control Account to find Credit Sales (now you have total Sales for the Trading Account) 4. Creditors Control Account to find Credit Purchases (which helps find total Purchases for the Trading Account) 5. The total of Drawings (stuff taken from the business for the owners use) The tricky issues are: The loan when set up is interest separate from the loan. The interest is paid by standing order each month. Repaying the principal is provided for by opening an Investment Account (Fixed Asset). Money will be transferred to it each month and eventually the loan will be repaid when the Investment Account reaches the value of the loan. The Drawings differentiate between the amount used and amount paid of some of the expenses There will be prepaids and dues for the expenses which will have to be calculated A bank receipt of Dividends is actually a Capital Injection, ie more money invested by the owner in the firm 2. Balance Sheet Method: quite similar to the Cash Book Method but the way we complete the question is different. The initial roughwork is The Opening Balance Sheet A list of Drawings Again we lay out the documents blank and focus on completing the Balance Sheet first. We can calculate Net Assets and the Reserves is a missing figure to make the Balance Sheet balance. Working backwards we can find Net Profit. Then we add on the Expenses to find Gross Profit. Using the Gross Mark Up, we can find Cost of Sales and Sales. 3. Ratios Method: we are given some figures for the final accounts with some ratios. We put the figures into the blank documents and use the ratios to find the Working Capital first, followed by Net Assets. We then find reserves and work back to find Sales.