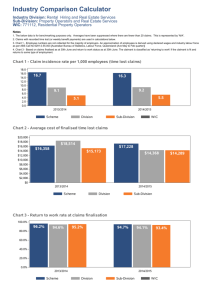

Future direction for interim payments

advertisement