Hedging of M&A Transactions

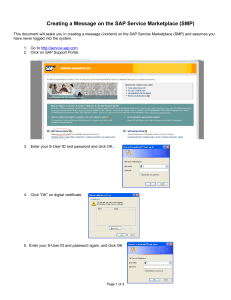

Jörg Wiemer

Senior Vice President

Head of Global Treasury

October 27th 2010

Public

Agenda

1. Introduction

About SAP

Sybase tender offer

2. Financial Risks in M&A Transactions

Liquidity risk

Interest rate risk, counterparty risk, settlement risk, FX risk

3. Hedging of Financial Risks in M&A Transactions

Driving forces for M&A hedging decision process

Decision matrix: Hedging instruments

© SAP AG 2010. All rights reserved. / Page 2

Public

The World’s Leading Provider of Business

Application Software

Undisputed market leader with >100,000 customers in 120 countries

– the largest customer base in enterprise applications

A solid track record of growth and return to

investors

Strong sales opportunity into installed base –

business with existing customers accounts

for ~80% of order entry

Steadily increasing share of recurring

revenues – over 50%

Recognized global brand (27th most valuable

in the world according to BusinessWeek*)

Deepest industry knowledge with more than

25 industry solutions available

Strong focus on ecosystem to foster coinnovation

Leading product and technology innovation

with ~14,500 developers

* Source: Interbrand / BusinessWeek 2009

© SAP AG 2010. All rights reserved. / Page 3

Public

SAP’s Long-Term Success – Selected KPI’s

Total Revenue

SSRS Revenue

Operating Profit

CAGR 7.7%

CAGR 10.2%

CAGR 13.9%

11.7

8.5

9.4

10.3

5.1

1999

8.6

10.7

7.4

6.0

8.2

1999

2.5

2.9

6.6

3.1

2005 2006 2007 2008 2009

2.3

2.7

3.3

0.8

2005 2006 2007 2008 2009

1999

2005 2006 2007 2008 2009

Free Cash Flow*

Operating Margin

CAGR 25.7%

27% 27% 26% 28% 27%

2.8

1.8

16%

1.3

1.5

1.5

SAP’s business model

continuously proved to be

sustainable, robust and

long-term oriented

0.3

1999

2005 2006 2007 2008 2009

1999

2005 2006 2007 2008 2009

Note: 1999 and 2005 based on US-GAAP; 2006 and 2007 based on IFRS; 2008 and 2009 based on Non-IFRS; in € billion, unless stated otherwise

* Cash flow from operations less capital expenditure

© SAP AG 2010. All rights reserved. / Page 4

Public

Sybase Tender Offer

On May 12th, 2010, SAP and Sybase Inc. signed a definitive merger agreement

SAP America, a subsidiary of SAP AG, makes an all cash tender offer for Sybase representing

an enterprise value of approximately USD 5.8bn

The transaction is funded from SAP’s cash on hand (partially USD) and a €2.75bn loan facility

Closing of tender offer is conditioned of a majority of outstanding shares (50,1%) and clearance

by the relevant antitrust authorities (both the US and Europe)

As of the expiration of the tender offer, 92,1% of Sybase’s outstanding shares of common stock

were tendered

The acquisition was immediately completed via a short-form merger under Delaware law

Rationale for this strategic move

Accelerate the reach of SAP solutions across mobile platforms to help companies managing and

analyzing business information and processes on any device

Drive forward the realization of SAP’s in-memory computing vision

© SAP AG 2010. All rights reserved. / Page 5

Public

Agenda

1. Introduction

About SAP

Sybase tender offer

2. Financial Risks in M&A Transactions

Liquidity risk

Interest rate risk, counterparty risk, settlement risk, FX risk

3. Hedging of Financial Risks in M&A Transactions

Driving forces for M&A hedging decision process

Decision matrix: Hedging instruments

© SAP AG 2010. All rights reserved. / Page 6

Public

Financial Risks in M&A Transactions (1/2)

Liquidity risk Significant appreciation of USD against EUR will create additional liquidity

needs measured in EUR

Actions taken Loan facility was established before final decision from supervisory board was

made and merger agreement was signed. In addition to available cash this guaranteed

minimum requirement of strategic liquidity level

Example: Potential cash outflow for

USD 5.8bn acquisition

7.500

6.500

5.500

4.500

3.500

2.500

1.500

500

-500

-1.500

-2.500

SAP Group

Gross Liquidity in

€m

Gross Liquidity

Minimal Liquidity

Credit Line

Scenario I

EUR/USD 1,30

Scenario II

EUR/USD 1,15

Scenario III

EUR/USD 1,00

€4.5bn

€5.0bn

€5.8bn

€2.75bn

loan facility

€1.5bn minimum strategic liquidity

Approx. €500m Bilateral credit lines

€1.5bn Syndicated credit line

EUR/USD ECB Fixing on May 12th: 1.2686

© SAP AG 2010. All rights reserved. / Page 7

Public

Financial Risks in M&A Transactions (2/2)

Interest rate risk Value at Risk calculation showed no significant impact for changes in 2 year

EUR swap rate in the period between beginning and closing of tender offer. Given SAP’s strong

cash flow generation a repayment of the loan facility will be possible within 2 years

Acceptance ratio Financing Volume in €m Value at Risk in €m

50%

1.375

12,50

75%

2.063

18,76

100%

2.750

25,01

50 day 99% VaR

Tender Offer risk Acceptance ratio for tender offer might be too low

Foreign exchange risk No P+L risk, only translation risk. Higher EUR counter value of future

free cash flow from Sybase to SAP compensates for “higher” purchase price if USD increases.

However, FX risk leads to liquidity risk

Acceptance ratio

50%

75%

100%

Exposure in USDm

Value at Risk in €m

2.400

293

3.850

469

5.300

646

50 day 99% VaR

An increase of the acceptance ratio by 1% leads to additional VaR of € 7m

Settlement risk Settlement of USD FX deals with different counterparties and same day value

payment to the US is a huge challenge

© SAP AG 2010. All rights reserved. / Page 8

Public

Agenda

1. Introduction

About SAP

Sybase tender offer

2. Financial Risks in M&A Transactions

Liquidity risk

Interest rate risk, counterparty risk, settlement risk, FX risk

3. Hedging of Financial Risks in M&A Transactions

Driving forces for M&A hedging decision process

Decision matrix: Hedging instruments

© SAP AG 2010. All rights reserved. / Page 9

Public

Driving Forces for M&A Hedging Decision

Process

Intercompany structure /

Internal Financing

Uncertainty about

approval of antitrust

authorities

Uncertainty about

success of tender offer /

acceptance ratio

Volatility in Capital

Markets

Hedging decision

Avoidance of P+L

volatility created via

pre-hedge

Market squeeze when

(FX) hedging activities

are started

Deal contingent hedging /

Definition of “highly

probable”

IFRS Accounting of

hedging instruments

© SAP AG 2010. All rights reserved. / Page 10

Public

Some Thoughts on Choice of Hedging

Instruments

Example 1

•

Do nothing does not create P&L volatility as a higher purchase price increases goodwill

•

However, a further depreciation of the EUR bears significant liquidity risks

Example 2

•

Plain Vanilla Forward hedges liquidity risk if the tender offer is successful

•

However, significant P+L and cash effect possible if tender offer is not successful

Example 3

• Enter into an at-the-money Plain Vanilla Option to hedge against liquidity risk

•

However, significant premium has to be paid which does not qualify for Hedge

Accounting (time-value)

© SAP AG 2010. All rights reserved. / Page 11

Public

Some Thoughts on Choice of Hedging

Instruments

Example 4

•

Deal contingent forward hedges liquidity risk at considerable cost, regardless of success

of tender offer

•

However, there is no flexibility on the acceptance ratio of the tender offer (over-hedging

might happen)

Usage of this instrument may lead to discussion with auditor on definition of “highly

probable”, which might not allow hedge accounting treatment

•

Example 5

•

Deal contingent option hedges liquidity risk regardless of success of tender offer

•

However, Hedge Accounting might not be applicable (“highly probable”) and increased

premium has to be paid in case of successful transaction

Example 6

•

Define a critical level at which liquidity risk is still acceptable

•

In case the critical level is triggered: Enter into an at-the-money Plain Vanilla Option

© SAP AG 2010. All rights reserved. / Page 12

Public

Decision matrix: Hedging Instruments

Do nothing

Plain Vanilla

Forward*

Plain Vanilla

Option atm*

Deal Contingent Deal Contingent Wait and hedge

Forward**

Option**

worst-case

Tender offer successful

Liquidity risk

Unexpected

P&L Volatility

Costs (Premium)

Tender offer not successful

Liquidity risk

Unexpected

P&L Volatility

Costs (Premium)

Summary

* Assumption: Hedge Accounting is obtained as transaction is highly probable

** Assumption: Hedge Accounting is not obtained as transaction is not highly probable

© SAP AG 2010. All rights reserved. / Page 13

Public

Thank you!

© SAP AG 2010. All rights reserved. / Page 14

Public

Q&A

© SAP AG 2010. All rights reserved. / Page 15

Public

© Copyright 2010 SAP AG

All Rights Reserved

No part of this publication may be reproduced or transmitted in any form or for any purpose without the express permission of SAP AG. The information contained herein

may be changed without prior notice.

Some software products marketed by SAP AG and its distributors contain proprietary software components of other software vendors.

Microsoft, Windows, Excel, Outlook, and PowerPoint are registered trademarks of Microsoft Corporation.

IBM, DB2, DB2 Universal Database, System i, System i5, System p, System p5, System x, System z, System z10, System z9, z10, z9, iSeries, pSeries, xSeries, zSeries,

eServer, z/VM, z/OS, i5/OS, S/390, OS/390, OS/400, AS/400, S/390 Parallel Enterprise Server, PowerVM, Power Architecture, POWER6+, POWER6, POWER5+,

POWER5, POWER, OpenPower, PowerPC, BatchPipes, BladeCenter, System Storage, GPFS, HACMP, RETAIN, DB2 Connect, RACF, Redbooks, OS/2, Parallel Sysplex,

MVS/ESA, AIX, Intelligent Miner, WebSphere, Netfinity, Tivoli and Informix are trademarks or registered trademarks of IBM Corporation.

Linux is the registered trademark of Linus Torvalds in the U.S. and other countries.

Adobe, the Adobe logo, Acrobat, PostScript, and Reader are either trademarks or registered trademarks of Adobe Systems Incorporated in the United States and/or other

countries.

Oracle is a registered trademark of Oracle Corporation.

UNIX, X/Open, OSF/1, and Motif are registered trademarks of the Open Group.

Citrix, ICA, Program Neighborhood, MetaFrame, WinFrame, VideoFrame, and MultiWin are trademarks or registered trademarks of Citrix Systems, Inc.

HTML, XML, XHTML and W3C are trademarks or registered trademarks of W3C®, World Wide Web Consortium, Massachusetts Institute of Technology.

Java is a registered trademark of Sun Microsystems, Inc.

JavaScript is a registered trademark of Sun Microsystems, Inc., used under license for technology invented and implemented by Netscape.

SAP, R/3, SAP NetWeaver, Duet, PartnerEdge, ByDesign, SAP Business ByDesign, and other SAP products and services mentioned herein as well as their respective

logos are trademarks or registered trademarks of SAP AG in Germany and other countries.

Business Objects and the Business Objects logo, BusinessObjects, Crystal Reports, Crystal Decisions, Web Intelligence, Xcelsius, and other Business Objects products and

services mentioned herein as well as their respective logos are trademarks or registered trademarks of Business Objects S.A. in the United States and in other countries.

Business Objects is an SAP company.

All other product and service names mentioned are the trademarks of their respective companies. Data contained in this document serves informational purposes only.

National product specifications may vary.

These materials are subject to change without notice. These materials are provided by SAP AG and its affiliated companies ("SAP Group") for informational purposes only,

without representation or warranty of any kind, and SAP Group shall not be liable for errors or omissions with respect to the materials. The only warranties for SAP Group

products and services are those that are set forth in the express warranty statements accompanying such products and services, if any. Nothing herein should be construed

as constituting an additional warrant.

© SAP AG 2010. All rights reserved. / Page 16

Public