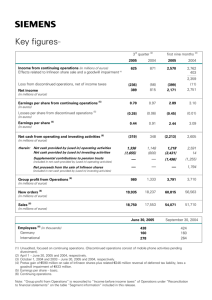

2014 Financial documents

advertisement