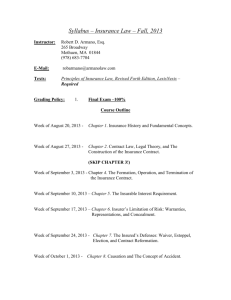

unfair trade practices act - National Association of Insurance

advertisement