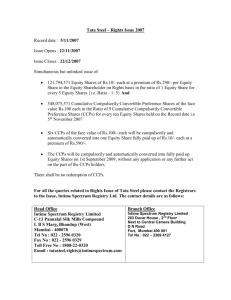

Equity Financing

advertisement