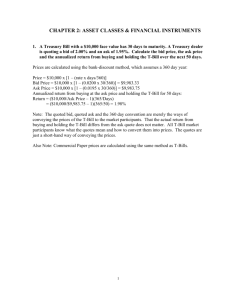

Chapter 7 Practice Problems 1. Below is a plot of the U.S. Treasury

advertisement

Chapter 7 Practice Problems 1. Below is a plot of the U.S. Treasury yield curve for Tuesday, January 17th. a. Based upon the extreme arbitrage theory (expectations hypothesis), what are predicted future interest rates (based upon “yesterday’s” yield curve)? b. Based upon the segmented markets theory, what are predicted future interest rates (based upon “yesterday’s” yield curve)? c. Based upon the preferred habitat theory (liquidity premium theory), what are predicted future interest rates (based upon “yesterday’s” yield curve)? d. Using either theory, what is the market predicting for future interest rates compared to one year ago? 2. Risk premiums on corporate bounds are usually countercyclical (they decrease during business cycle expansions and increase during contractions). Why is this so? 3. Assuming that the expectations theory is the correct theory of the term structure, calculate the interest rates in the term structure for maturities of one to five years, and plot the resulting yield curves for the following paths of one-year expected interest rates over the next five years: a. 5%, 6%, 7%, 6%, 5% b. 5%, 7%, 7%, 7%, 7%. c. How would your yield curves change if people preferred shorter-term bonds to longer-term bonds? 4. What effect would reducing income tax rates have on the interest rates of municipal bonds? Would interest rates of Treasury securities be affected? If so, how? 5. Suppose your marginal federal income tax rate is 36 percent. What is your after-tax return from holding a one-year corporate bond with a yield of 9 percent? What is your after-tax return from holding a one-year municipal bond with a yield of 5 percent? How would you decide which bond to hold? 6. Imagine that the typical bond purchaser has a utility function of the form U = $2/3. This bond purchaser is considering a one year corporate bond which is a discount bond with face value of $1000. 95% of the time this corporation fulfills its commitment and pays this face value. There is a 5% chance that the corporation fails and pays nothing to bond holders. a. What is the highest price a typical bond purchaser would pay for the corporate bond? What is its associated interest rate? b. All of a sudden, the economy enters a recession and as a result, the market believes there is a 6% chance of corporate bond default. What happens to the price the typical purchaser would be willing to pay for this bond? What happens to its interest rate? Compare this to part a and comment.