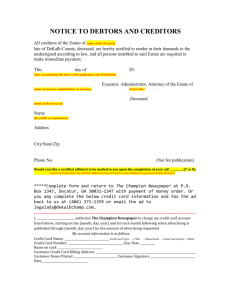

")

Managing the tax affairs of someone who has died

Page 1 of 13

Managing the tax affairs of someone who has died

Introduction

This guide will help you finalise the tax affairs of a deceased person. It tells you what tax returns you may need to lodge

and how the tax liability will be worked out.

General law

The law that applies to the assets and income of a deceased person depends on which state or territory of Australia the

deceased person lived in when they died.

If you have been appointed as an executor or administrator of the estate of a deceased person, you will be responsible for

managing the deceased estate's tax affairs, as well as:

z

z

carrying out (executing) the terms of the deceased person's will, or

complying with the relevant inheritance laws where there is no will.

You can find more information about the inheritance laws that apply in your state or territory by contacting the Public

Trustee Office.

Wherever the word ‘executor’ is used in this document, it applies equally to an executrix, trustee, administrator or legal

personal representative.

Taxation law

There are no death duties in Australia.

However, the Income Tax Assessment Act 1997 does tax certain income or capital transactions that occur as a

consequence of a person's death.

The tax consequences are different from the perspective of:

z

z

z

the deceased person

the executor, or

a beneficiary of the deceased estate.

What is a deceased estate?

The property and assets belonging to a person who has died is called their deceased estate. The deceased estate is held

in trust from the death of the person until the transfer of the property and assets to the beneficiaries. The deceased estate

is considered to be a trust during this period. Unlike a natural person or a company, a trust is not a legal entity in its own

right, but a relationship involving a trustee and the beneficiaries.

The executor of the estate is the person who holds the deceased estate in trust. That person is the trustee for the

deceased estate trust. The executor is responsible for administering the deceased estate in the best interest of the

beneficiaries.

Beneficiaries are those people who share in the deceased estate. They are usually named in the will, where one exists. If

no will exists, they are usually the deceased person’s next of kin.

What does an executor do?

An executor is appointed by the deceased person's will to administer their deceased estate in accordance with their will.

The Supreme Court can also appoint an administrator to deal with the deceased estate – for example, where there is no

valid will or the person nominated to be executor cannot discharge their duties.

The executor, in effect, steps into the shoes of the deceased person and winds up the deceased person's personal affairs.

Some other tasks usually performed by an executor include:

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

z

z

z

z

z

z

z

z

z

z

Page 2 of 13

locating the will

arranging the funeral

applying for probate

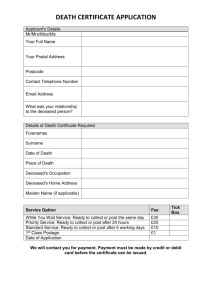

obtaining a death certificate

informing investment bodies of the death

informing Centrelink

locating and assessing the value of assets

paying debts, income tax and funeral expenses

transferring assets and paying stamp duty, and

distributing the surplus to beneficiaries.

Appendix A provides an illustration of the different stages of administration of a deceased estate.

What forms part of a deceased estate?

Assets owned by the deceased person form part of the deceased estate. For example, real estate, money in bank

accounts, shares, and personal chattels. Some types of income will also form part of the deceased estate.

Some assets will not be included in the deceased estate because the deceased person has made other arrangements to

distribute those assets.

Superannuation and life insurance payments

Superannuation and life insurance payments may or may not form part of the deceased estate. If there are stipulated

beneficiaries under the policies, the payments may go directly to the beneficiaries without going through the deceased

estate.

Jointly owned assets

Assets that are jointly owned may or may not form part of the deceased estate. This will depend on the type of coownership. There are two categories of co-ownership:

z

z

joint tenancy, and

tenancy-in-common.

When a joint tenant dies, their share in the asset is extinguished and they cannot pass the asset to their estate. The

surviving owner becomes the sole owner. The most common type of asset held in joint tenancy is the family home.

When a tenant-in-common dies, their share passes to their deceased estate. Hence, the executor can deal with that share

in the asset.

In the case of real estate, the title deed usually specifies the type of co-ownership. Under common law, joint tenancy of

real estate is presumed in the absence of contrary intention.

For other assets like bank accounts and shares, the type of ownership is often not stipulated. The contract or purchase

documentation may provide clues.

What is a will?

A will is a legal document that sets out directions for the administration and disposal of your property after your death.

What is probate?

Where the deceased person leaves a will, the executor needs to obtain probate before they can distribute the assets of

the deceased estate to the beneficiaries. Probate is granted by the Supreme Court in the state or territory in which the will

is lodged. Probate is the Supreme Court's authority to the executor to administer the deceased estate.

People who believe they have an entitlement to part of the deceased estate or creditors of the deceased person (for

example, the Tax Office if there is an outstanding tax liability), can contest the will before probate.

What happens if the deceased person did not have a valid will?

If the deceased died without a valid will (intestate), letters of administration need to be obtained from the Supreme Court

appointing someone to administer the deceased estate.

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

Page 3 of 13

In such situations, the assets of the deceased person are distributed in accordance with the succession laws of the states

and territories of Australia. Generally, that means the estate passes to the deceased person’s next of kin.

What is a testamentary trust?

A testamentary trust is a trust established by a will. It does not come into effect until after the death of the person making

the will. At this point in time, specified deceased estate property is transferred to a trustee who holds the assets on trust

for the benefit of the beneficiaries. A testamentary trust is not the same trust as the deceased estate.

A testamentary trust may last for many years after the deceased estate has been fully administered. The information

provided in this document is not appropriate for testamentary trusts.

Tax obligations of executors

Role of executor

An executor has certain taxation responsibilities on behalf of the deceased person and the deceased estate.

Some of the responsibilities include:

z

z

z

z

z

z

z

notifying the Tax Office of the death, to stop the issue of any notices which may cause distress to partners or other

relatives

lodging prior year tax returns on behalf of the deceased person

lodging a 'date of death' (final) personal tax return on behalf of the deceased person

applying for a trust tax file number for the deceased estate if trust tax returns need to be lodged

preparing and lodging trust tax returns for the deceased estate, if necessary

making distributions to beneficiaries, and

paying tax on behalf of certain beneficiaries.

Any tax liability that may arise from your role as executor is separate from your own personal tax liability.

You do not include any of the income of the deceased person or deceased estate in your own personal tax return, except

for any trust income you received as a beneficiary.

Authority to deal with the tax affairs of the deceased person

For you to deal with the deceased person’s tax affairs, you will need proof that you have the authority to do so.

After you have been appointed executor, you should write to the Tax Office with details of the deceased person’s:

z

z

z

z

z

full name

date of birth

date of death

address for services of notices, and

tax file number, if known.

You will need to provide proof of identity for yourself and documents such as the death certificate and the will or evidence

of the grant of probate or letter of administration (when it is granted – this may be some time after you lodge the deceased

person's tax returns).

The tax file number of the deceased person cannot be disclosed to you until you have established your authority. Once

that is done, you can request the tax file number of the deceased person over the phone or have it sent to you.

Tax return for the deceased person

If the deceased person did not lodge prior year tax returns, you will need to determine whether they are necessary. If

required, you need to prepare and lodge them.

There may be a number of reasons why you may have to lodge a personal tax return for the deceased person.

For example:

z

tax has been withheld from the income earned by the deceased person

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

z

z

z

Page 4 of 13

the deceased person earned taxable income exceeding the tax-free threshold

tax has been withheld from interest or dividends because no tax file number was quoted to the investment body, or

the deceased had lodged returns in prior years.

To determine if a final tax return for the deceased person is required, read Do I need to lodge a tax return?

Final tax return not required for deceased person

If you have determined that a final tax return is not required, please complete the Non-lodgment advice 2006-07

(NAT 2586-6.2007) and send it into the Tax Office.

On the form, where it asks for the reason, please print ‘DECEASED’ followed by the date of death.

Final personal tax return required for deceased person

If the deceased person has been lodging tax returns prior to their death, you will need to submit a final tax return on behalf

of the deceased person.

This will be the final personal tax return of the deceased person with their personal tax file number. This tax return is

known as the ‘date of death return’.

That tax return should cover the period from the previous 1 July to the date of death. For example, if the date of death was

6 March 2007, the date of death tax return will cover the period 1 July 2006 to 6 March 2007.

The final tax return should include all assessable income derived by the deceased person and all the tax-deductible

expenses incurred up to the date of death. (Income derived after the date of death, and any deductible expenses incurred

after the date of death, are included in the deceased estate's trust return.)

Examples of assessable income include:

z

z

z

z

z

z

salary or wages

bank interest

dividends from share investments

trust distributions from managed investment funds

rent from investment properties, and

capital gains from the sale of assets.

Examples of tax-deductible expenses include:

z

z

z

z

z

work-related expenses like tools of trade, uniform or professional publications

tax related expenses incurred by the executor in relation to the income tax affairs of the deceased person

ongoing management fees paid to investment advisers

bank charges, and

rental expenses in relation to an investment property.

Gifts made under a will are not tax deductible unless the gift is made under the cultural bequest program. In such

instances, the deduction is allowable in the date of death tax return of the deceased person.

A claim for medical expenses tax offset may be made in relation to net medical expenses incurred by the deceased

person. This includes the amounts incurred by the deceased person but paid by you, as the executor of the deceased

estate.

Funeral expenses are not tax deductible nor are they eligible for the medical expense tax offset.

Losses

If the deceased person has accumulated losses at the date of death, those losses can be offset against income in the final

tax return (capital losses may be offset against capital gains), but cannot be carried forward into the deceased estate.

Ordinary losses as well as capital losses that cannot be offset in the final tax return for the deceased will lapse.

Completing the tax return

When preparing the final tax return for the deceased person, you need to:

z

print the words ‘DECEASED ESTATE’ on the top of page one of the tax return

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

z

z

Page 5 of 13

print ‘X’ in the ‘NO’ box at the question ‘Will you need to lodge an Australian tax return in the future?’

sign the tax return on behalf of the deceased person.

Note:

When completing the Medicare levy questions:

Question M1: If the deceased person (and any dependants) were fully exempt from the Medicare levy until their

death, the number of days that they are exempt from the Medicare levy (Label V) in this return is 365.

If the deceased person was half exempt from the Medicare levy until their death, the number of days that they are

half exempt from the Medicare levy (Label W) in this return is 365.

Question M2: If the deceased person (and any dependants) were covered by private hospital cover or were

exempt from the Medicare levy until their death, the number of days that they do not have to pay the Medicare levy

surcharge (Label A) in this return is 365.

Any refunds from this final tax return will be sent to you as the executor. Similarly, any tax liabilities of the deceased

person are to be paid by you out of the deceased estate. You need to withhold amounts from the assets or income of the

deceased estate to pay this liability.

Tax rates for final tax return of deceased person

The general individual tax rates, with the full tax-free threshold, apply to the final tax return of the deceased person, if an

Australian resident. The Medicare levy and Medicare levy surcharge may also be payable.

Higher Education Contribution Scheme (HECS) debt and Student Financial

Supplement Scheme (SFSS)

The trustee or executor of a deceased person is required to lodge all outstanding tax returns up to the date of death of the

person. If the deceased person had an accumulated HECS and/or SFSS debt at the time of their death, a compulsory

HECS/SFSS repayment will be calculated. Compulsory repayments will be raised in the income tax notice of assessment

when the minimum repayment thresholds are reached ($38,149 in 2007 for HECS debt and $38,149 in 2007 for SFSS

debts).

Any compulsory HECS and/or SFSS repayment included on an income tax notice of assessment which relates to the

period before death must be paid by the deceased estate. The remainder of the accumulated HECS and/or SFSS debt is

cancelled.

For more information on HECS/SFSS and how compulsory repayments are calculated, read

z

z

Repaying your HELP debt in 2006-07, and/or

Repaying your Financial Supplement loan 2006-07.

How to get a tax return

The individual tax return is part of TaxPack. Read TaxPack 2007 for information on how to obtain a copy.

Tax clearance

The Tax Office no longer issues letters of clearance, stating that income tax liabilities to the date of death have been

satisfied. The notice of assessment in respect of the date of death return will constitute the formal notification where:

z

z

all the liabilities on the notice have been satisfied, or

the notice states that no tax is payable.

Where the deceased person has not lodged a return for several years, the last notice of assessment will serve the same

purpose.

Taxation of the deceased estate

After the date of death, the deceased estate may receive income from various sources (see Assessable income). A trust

tax return will need to be lodged for the deceased estate if there is tax payable on the income or if tax has been withheld

from that income.

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

Page 6 of 13

A trust tax return will need to be lodged each income year until the deceased estate is fully administered (that is, all of its

assets and income are distributed to the beneficiaries) and no longer deriving income.

The net income of the deceased estate is taxed either in the hands of:

z

z

the beneficiaries who are presently entitled, or

the executor.

Assessable income

Any income derived after the date of death belongs to the deceased estate. Income derived after death may include:

z

z

z

z

z

z

z

z

salary and wages unpaid at the date of death

bank interest

eligible termination payments

dividends from share investments

trust distributions from managed investment funds

investment income from a friendly society funeral policy taken out after 31 December 2002 (for more information,

read Tax changes for friendly society funeral polices).

rent from investment properties, and

capital gains from the sale of assets.

Amounts for annual and long service leave paid to the deceased person’s beneficiaries or the executor are exempt from

tax.

Eligible termination payments (ETPs)

Sometimes, you may receive a payment called a death benefit eligible termination payment. This payment may be paid by

the deceased person’s employer, superannuation fund, approved deposit fund or from a retirement savings account.

z

This amount is tax-free when it is within the reasonable benefit limit (RBL), and

z

passed on to the deceased person’s dependants. In this context a dependant is someone who is financially

dependent, but it will always include the spouse of the deceased.

There are many special rules with for ETPs. For more help with such payments, phone 13 10 20.

If there are amounts of an ETP that are assessable, include them under ‘Other income’ in the trust tax return.

Tax-related expenses

Expenses incurred by the deceased estate in earning assessable income may be tax deductible. For example:

z

z

z

z

tax agent’s fees

ongoing management fees paid to investment advisers

bank charges, and

rental expenses for an investment property.

Gifts made pursuant to a will are not tax deductible unless the gift is made under the cultural bequest program (in which

case it must be included in the date of death return, not in the trust return).

Losses

If the deceased person has accumulated losses at the date of death, those losses cannot be carried forward into the

deceased estate. Ordinary losses as well as capital losses will lapse at the time of death.

Tax file number for the deceased estate

A tax file number is required to lodge a deceased estate’s tax return. You will need to complete an application form, Tax

file number application or enquiry for a deceased estate, for a trust tax file number and provide certain proof of identity

documents.

This trust tax file number may be quoted to investment bodies where investments are still held by the deceased estate. It

is not appropriate to quote your personal tax file number in the circumstances.

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

Page 7 of 13

Paying tax on the income of the deceased estate

There are many factors that will determine who pays the tax on the income derived by the deceased estate and the

applicable tax rate.

They include whether the beneficiaries are presently entitled, whether they are under a legal disability and whether the

deceased estate is fully administered. A summary of the different tax situations is provided in Appendix B.

While the deceased estate is under your administration, you will need to determine whether the beneficiaries are presently

entitled and under any legal disability at the end of each financial year (30 June). This will determine who is liable to pay

tax on the income of the deceased estate.

As executor, you cannot distribute the income or assets of a deceased estate until the debts of the deceased person,

including tax liabilities, are determined and probate has been granted.

You can distribute some of the income or assets to beneficiaries if you are certain that the remainder of the deceased

estate is sufficient to cover any outstanding liabilities.

Meaning of present entitlement

Beneficiaries are presently entitled to the income of a deceased estate if they have an indefeasible, absolutely vested

interest in the income. In other words, the beneficiaries have a claim or interest in the income that cannot be defeated by

another person. They must also be able to demand immediate payment of the income. This means that beneficiaries can

be presently entitled even though they may not have actually received an income distribution.

Generally, beneficiaries are not presently entitled to the income of a deceased estate during the administration of the

estate. This is because the debtors of the deceased person and any persons contesting the will may be able to defeat the

beneficiary's right to the income. This means that during this period, the income belongs to the deceased estate and not

the beneficiaries.

However, as administration progresses, it may become clear to you that part of the net income of the deceased estate will

not be required to either pay or provide for debts. You may exercise your discretion and pay some of the income to the

beneficiaries. The beneficiaries in this situation will be presently entitled to the income actually paid to them or actually

paid to someone else on their behalf.

Beneficiaries can be presently entitled if, under the terms of the will, money (income of the deceased estate) is applied for

their benefit and not paid directly to them. An example is the payment of the beneficiary’s rent.

No beneficiary is presently entitled to any income accrued by the deceased person at the date of death but only received

after death.

Meaning of legal disability

People are considered to be under a legal disability if they cannot give a valid discharge for money paid to them.

Beneficiaries are under a legal disability if they are either:

z

z

z

minors (that is, under 18 years of age as at 30 June)

bankrupt, or

declared legally incapable because of a mental condition.

When this group of persons become presently entitled to income of the deceased estate, you as executor will be assessed

on their behalf.

The income year in which the deceased estate is fully administered

The net income of the deceased estate (and whether any beneficiary is presently entitled) is determined on the last day of

each income year (30 June). This means that, on the last day of the income year, a beneficiary who is presently entitled

will be assessed on their share of the net income for the whole of the income year.

However, in the income year in which the deceased estate is fully administered, the Tax Office will accept an

apportionment of the net income received. Where the executors and beneficiaries are able to demonstrate, through proper

accounts at the completion of administration, the actual amounts of income derived in the periods before and after the day

on which the estate was fully administered, an apportionment may be made as follows:

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

Page 8 of 13

Income derived in the period between . . .

is assessed . . .

the beginning of the income year and the day administration

was complete

in your hands as the executor.

the day administration was complete and the end of the income to the beneficiaries who are presently

year

entitled.

Where beneficiaries are under a legal

disability, you as executor will be

assessed on their behalf.

For such an apportionment to take place:

z

z

there must be evidence of the income derived during these periods, and

you (as the executor), or the beneficiaries, must request it.

The Tax Office does not accept an apportionment into the two periods merely on a time basis.

One exception is when you (as executor) pay part of the income of the deceased estate to a beneficiary before the estate

is fully administered. In such an instance, the beneficiary would be assessed on the basis that they were presently entitled

to that income.

Lodging the deceased estate’s trust tax return

After you have determined whether the beneficiaries are presently entitled and whether they are under any legal disability

at the end of the financial year, you are then required to lodge a trust tax return for the deceased estate (if you are liable to

pay tax for the deceased estate).

If the deceased estate is paying tax on franked dividends, the imputation credits need to be claimed back through this trust

tax return.

You will need a copy of a Trust tax return 2007 and the accompanying Partnership and trust tax returns instructions 2007.

Special instructions for executors of deceased estates are contained in the guide.

If you need assistance with completing the trust tax return for the deceased estate, phone us on 13 28 61.

Tax rates for the deceased estate

Tax rates – beneficiary not presently entitled

To the extent beneficiaries are not presently entitled to the net income of the deceased estate, the tax liability will rest with

the deceased estate.

First three income years

For the first three tax returns, the deceased estate income to which no beneficiary is presently entitled is taxed at the

general individual rates, with the benefit of the full tax-free threshold. No Medicare levy is payable.

Read Individual income tax rates.

Example

The deceased passed away on 5 April 2005.

The first tax year for the deceased estate will cover the period 6 April 2005 to 30 June 2005.

The second tax year will be from 1 July 2005 to 30 June 2006.

The third tax year will be from 1 July 2006 to 30 June 2007.

If the deceased estate earned taxable income of $6,000 or less during those first three tax returns, there is no tax

payable.

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

Page 9 of 13

This concessional period of three tax years at the general individual rates, with the benefit of the full tax-free threshold,

cannot be extended.

If the administration of the deceased estate is completed in the same income year as the date of death, you do not need

to lodge a trust tax return for the deceased estate if:

z

no beneficiary is presently entitled to any of the income of the deceased estate (they may receive assets only),

and

z

the taxable income of the estate is below the tax-free threshold of $6,000 (for the 2007 income year).

Fourth income year and later

For deceased estates with prolonged administration that extend beyond the concessionally taxed period, there are special

progressive trust tax rates that will apply.

Example

The deceased passed away on 5 April 2004.

The first tax year for the deceased estate will cover the period 6 April 2004 to 30 June 2004.

The second tax year will be from 1 July 2004 to 30 June 2005.

The third tax year will be from 1 July 2005 to 30 June 2006.

The fourth tax year will be from 1 July 2006 to 30 June 2007.

It is from the fourth tax year that the special progressive tax rates will apply.

For the 2007 income year, the special progressive tax rates are:

Deceased estate taxable income

(no present entitlement)

Tax rates

$0 - $416

Nil

$417 - $594

50% of the excess over $416

$595 - $25,000

$89 plus

15% of the excess over $594

$25,001 - $75,000

$3,750 plus

30% of the excess over $25,000

$75,001 - $150,000

$18,750 plus

40% of the excess over $75,000

$150,001 and over

$48,750 plus

45% of the excess over $150,000

No Medicare levy is payable.

Tax rates – beneficiary presently entitled and not under a legal disability

If the beneficiary is presently entitled and not under a legal disability, they are liable for tax.

For example, if you make an income distribution to an adult resident beneficiary, it is the responsibility of that person to

declare the amount in their personal tax return and pay income tax on it at their marginal tax rate.

Tax rates - beneficiary presently entitled but under a legal disability

If the beneficiary is presently entitled, but under a legal disability, you will be liable to pay tax on their behalf. You will be

assessed separately for each beneficiary in this category.

The general individual tax rates apply. These rates are set out in Individual income tax rates.

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

Page 10 of 13

Normally, unearned income of minors is subject to tax at higher rates and a lower tax-free threshold. However, for

distributions from a deceased estate, the ordinary tax rates apply.

Medicare levy

Medicare levy and Medicare levy surcharge are also payable in the same way as if the income was assessed to the

beneficiary. For more information, read What is the Medicare levy?

Tax offsets

You are also entitled to tax offsets to which the beneficiary would be entitled – for example, the dependent spouse,

medical expenses and 30% private health insurance tax offsets. The low income tax offset is automatically calculated if

the income is below the relevant threshold.

You will need to include a statement with the tax return showing the type and amounts of tax offsets claimed.

Tax rates – non-resident beneficiary

If the beneficiary is a non-resident of Australia for taxation purposes, you are liable to pay tax on the beneficiary’s share of

the trust income distributed.

The non-resident tax rates apply. These are set out in Individual income tax rates.

No Medicare levy is payable.

Interest and dividends are not included in the non-resident beneficiary's trust income. Instead, these are taxed by having a

non-resident withholding tax withheld and paid to the Tax Office. The withholding tax rate varies for different countries and

between interest and dividends. Fully franked dividends are not subject to withholding tax. To find the appropriate

withholding rate, phone us on 13 28 61.

Information for beneficiary

Beneficiaries who are presently entitled may need to lodge personal tax returns and disclose their trust distributions.

Accordingly, they need to know certain information about their entitlement.

All beneficiaries who are presently entitled should be provided with the following information:

z

z

z

z

their share of trust income that they were presently entitled to

the amount of their entitlement that was applied for their benefit

the amount that is assessable to them, and

their share of imputation credits associated with any dividends that may be in the trust distribution.

Beneficiaries presently entitled but under a legal disability also need to know the amount of tax you have paid on their

behalf. They are entitled to receive a tax credit for this tax so that the same amount will not be taxed twice.

Non-resident beneficiaries will also need to know:

z

z

z

z

the amount of interest in their distribution and the withholding tax paid

the amount of unfranked dividends in their distribution and the withholding tax paid

the amount of franked dividends in their distribution, and

the amount of tax you have paid on their behalf.

Tax obligations of beneficiaries

A beneficiary is a person who receives all or part of the deceased estate. If a will exists, it usually sets out how the

deceased estate and income should be dealt with.

There may be some tax obligations for beneficiaries, depending on the nature of any distribution they may receive. As the

executor, you should provide details of trust distributions to the beneficiaries.

Corpus distribution

If the trust distribution represents corpus of the deceased estate, no tax is payable by the deceased estate or the

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

Page 11 of 13

beneficiary.

Corpus is the capital amount or income that has already been subject to tax to the deceased estate – for example, the

capital sums in a bank account.

If the distribution takes the form of a transfer of asset, there may be capital gains tax consequences to the beneficiary.

Income distribution

If the trust distribution consists of income of the deceased estate, the tax implications to the beneficiaries depend on

whether they are presently entitled to the income.

If the estate income is applied on behalf of the beneficiaries, they are considered to be presently entitled to the amount,

even though they did not receive any money in their hands. An example is the payment of the beneficiary’s rent.

Presently entitled and under no legal disability

Australian resident beneficiaries who are presently entitled and not under any legal disability, will be personally liable to

pay tax on the income distribution.

They will need to disclose that income distribution from the deceased estate in their personal tax return and pay tax at the

general individual tax rates.

The income will be assessable in the year the present entitlement arose, not in the year the amount is received.

For example, if a beneficiary was presently entitled to the deceased estate income on 30 June 2007, they are personally

assessable on that amount in the year ended 30 June 2007, even though the amount may be received after that date in

the following tax year.

Presently entitled and under legal disability

For those beneficiaries who are presently entitled but under a legal disability (for example, under 18 years old), you as

executor of the deceased estate should have paid tax on their behalf in respect of the income distribution.

If that income distribution from the deceased estate is their only source of income for the year, they do not need to lodge a

personal tax return.

If the beneficiaries have other income, they need to lodge a personal tax return that includes the income distribution from

the deceased estate. However, they will be entitled to a credit for the tax paid or payable by you on their behalf.

Overseas deceased estate

For Australian resident beneficiaries, the rules are the same, regardless of whether the deceased estate is in Australia or

overseas. Where the income distribution from an overseas deceased estate has been subject to foreign tax, they may be

entitled to a foreign tax credit. (Read How to claim a foreign tax credit 2006-07 (NAT 2338-6.2007).)

Franked dividends

If some of the income distribution from the deceased estate consists of franked dividends (that is, the company paying the

dividends has paid income tax in respect of the amount), resident beneficiaries are also entitled to the associated franking

credit when the income distribution is disclosed in their personal tax returns.

That is why you need to inform them of their share of any franking credits associated with the franked dividends.

To find more information about the dividend imputation system, read Refunding franking credits – individuals.

Capital gains tax

When you transfer or sell assets of the deceased estate, there may be capital gains tax consequences. There are special

capital gains tax rules regarding such assets.

For more information, read Deceased estate and capital gains tax.

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

Page 12 of 13

Checklist

To fully meet the taxation obligations, you may need the following from the Tax Office:

z

z

z

z

z

z

z

z

z

tax file number of the deceased person

Non-lodgment advice 2006-07 (NAT 2586-6.2007)

TaxPack 2007 (including the personal tax returns)

Tax file number application or enquiry for a deceased estate

Trust tax return 2007

Partnership and trust tax returns instructions 2007

Guide to capital gains tax 2006-07 (NAT 4151-6.2007)

Guide to capital gains tax concessions for small business

Taxation Ruling IT 2622: Present entitlement during the stages of administration of deceased estates

Do you need to know more?

For more information about deceased estates, you can:

z

z

phone us on 13 28 61, or

seek advice from a professional adviser.

Appendix A - stages of administration of a deceased estate

The period of administration begins at the date of death and ends when the administration of the estate is complete.

Date of death

Stages of administration

Period of administration

1.

2.

3.

4.

Burial of deceased person

Executor appointed by will or administrator appointed by Court

Probate applied for and granted by Court

Assets vested in executor who administers estate

{ date of death and trust tax return lodged

{ initial stage – net income of estate is applied to reduce debts

(including tax liabilities) etc

{ intermediate stage – part of the net income of estate that is not

required to pay debts etc may be paid to beneficiaries

{ final stage – debts etc are paid or provided for in full and net

income and assets of the estate are distributed to beneficiaries.

Administration of estate is complete

Appendix B - a summary of how deceased estate income is taxed in

relation to Australian resident beneficiaries

If the income is an

amount to which . . .

then . . .

a beneficiary is presently

entitled

determine whether or not

the beneficiary is under a

legal liability

the income is

assessed . . .

the tax rates which

apply . .

if the beneficiary is under a to the executor on

legal liability

behalf of the

beneficiary

general income tax rates

apply

if the beneficiary is not

under a legal liability

to the beneficiary on

their personal income

tax return

the beneficiary’s marginal

tax rates will apply

the executor is

assessed on the

income

concessional tax rates

apply for the first three tax

returns of the deceased

estate.

no beneficiary is presently

entitled

Last Modified: Wednesday, 6 June 2007

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

Managing the tax affairs of someone who has died

Page 13 of 13

Copyright

© Commonwealth of Australia

This work is copyright. You may download, display, print and reproduce this material in unaltered form only (retaining this

notice) for your personal, non-commercial use or use within your organisation. Apart from any use as permitted under the

Copyright Act 1968, all other rights are reserved.

Requests for further authorisation should be directed to the Commonwealth Copyright Administration, Copyright Law

Branch, Attorney-General’s Department, Robert Garran Offices, National Circuit, BARTON ACT 2600 or posted at

http://www.ag.gov.au/cca.

http://www.ato.gov.au/print.asp?doc=/content/31669.htm

08/04/2008

")