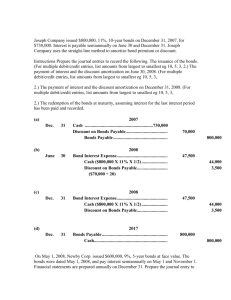

CHAPTER 10

advertisement