UVA-F-1737

Rev. Nov. 4, 2015

Páginas de uso exclusivo promocional. Puede adquirir la versión completa en www.iesep.com

Selling Facebook

It was the evening of Monday, May 7, 2012, less than two weeks before the much-anticipated initial public

offering (IPO) of Facebook, Inc. Investment banker Michael Grimes listened attentively as David Ebersman,

chief financial officer of Facebook, explained that the social media company’s spectacular revenue growth

seemed to be slowing—just as the company was preparing to sell its shares to the public. The most recent data

showed that Facebook continued to add users at a rapid rate, but more and more of those users were accessing

the social media site via mobile devices—smartphones and tablets—rather than from personal computers.

Because Facebook did not yet offer advertising on its mobile site, that trend was adversely affecting revenue

growth. Facebook’s internal forecasts had estimated that revenue would reach $1.1 to $1.2 billion for the quarter

and $5 billion for the fiscal year. In mid-April, as part of the preparations for the company’s IPO, Ebersman

had shared those forecasts with a roomful of equity research analysts from Wall Street firms participating in the

IPO. For the analysts, the numbers formed the basis for their valuation models and the recommendations they

shared with clients who were interested in investing in the IPO. Now, with user growth outpacing growth in

advertising revenue, Ebersman was no longer confident of the financial projections he had shared with the

analysts.

Earlier in the day at a midtown Manhattan hotel in New York City, Grimes and Ebersman, along with

founder and CEO Mark Zuckerberg (age 27) and COO Sheryl Sandberg (age 42), had kicked off the company’s

IPO roadshow, pitching the Facebook IPO to more than 500 institutional investors at an invitation-only

luncheon event. The attendees were specially selected guests—investors who directed significant business to

the firms involved in the Facebook deal. Experienced and knowledgeable investors, they came prepared to hear

management’s sales pitch and ask questions about the company’s future prospects. Most, if not all, had received

verbal communications regarding Facebook’s IPO, including financial forecasts from one of the Wall Street

firms whose analysts had attended the April meeting. Some suspected that the forecasts were intentionally low

and expected that Facebook’s financial results would be higher than the estimates.

The luncheon event had not gone as smoothly as hoped. To the surprise of at least some Wall Street

investors in attendance, Zuckerberg had worn his usual attire—a hooded sweatshirt and sneakers—to greet his

potential shareholders. According to Wedbush Securities analyst Michael Pachter, “He’s actually showing

investors he doesn’t care that much…I think that’s a mark of immaturity…he has to realize he’s bringing

investors in as a new constituency right now…he’s got to show them the respect that they deserve because he’s

asking them for their money.”1 In addition, a number of potential investors in attendance had complained that

the 30-minute video shown at the beginning of the meeting reduced the time available for a question-and1

Damon Poeter, “Facebook IPO: Why Don’t We Do It

http://www.pcmag.com/article2/0,2817,2404202,00.asp (accessed Jul. 22, 2015).

in

the

Roadshow?,”

PC

Magazine,

May

9,

2012,

This case was prepared by Dorothy C. Kelly, CFA, under the supervision of Professor Robert Conroy, J. Harvie Wilkinson, Jr., Professor of Business

Administration, and Professor R. Edward Freeman, Elis and Signe Olsson Professor of Business Administration, Darden School of Business, University

of Virginia. It was adapted from CFA Institute training and other materials developed by the author from public documents. This case was written as a

basis for classroom discussion and is not an indication or representation of how a business situation should or should not be handled or addressed.

Copyright © 2015 by University of Virginia Darden Business Publishing, Charlottesville, Virginia. All rights reserved. To order copies, send an e-mail to

sales@dardenbusinesspublishing.com. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in any form or by

any means, electronic, mechanical, photocopying, recording, or other means without permission of the Darden School Foundation.

Distribuido por IESE Publishing. Si necesita más copias, contáctenos: www.iesep.com. Todos los derechos reservados.

Page 2

UVA-F-1737

Páginas de uso exclusivo promocional. Puede adquirir la versión completa en www.iesep.com

answer session with management. Grimes learned that attendees would have preferred to watch the video

online and have more time to quiz management about the business. Now, Facebook’s CFO was sharing

additional unwelcome news.

Ebersman (age 42) and Grimes (age 46) had been working closely together for months to complete what

would soon become the largest IPO by a technology company in U.S. history. Grimes’s employer, Morgan

Stanley, was the lead investment bank for the IPO, acting as representative for a syndicate of investmentbanking and financial-services firms that would complete the offering. As the senior investment banker on the

deal, Grimes was responsible for guiding the firm’s client through the IPO process, which included helping the

company navigate the regulatory and legal requirements; communicating with regulators, other underwriters,

analysts, potential investors, and the media; and managing and marketing the offering both before and after the

IPO. All this was to assure that Facebook and its selling shareholders received the highest possible price for

the IPO.

The following day, the nine-day roadshow would continue with a breakfast meeting at 7:15 in Boston,

followed by additional stops in other cities including Baltimore, Philadelphia, and Palo Alto, California. What,

if any, advice would Grimes offer his clients as they prepared for the next day’s meeting with potential investors?

What guidance should Grimes give Ebersman about disclosing the latest information regarding Facebook’s

business to the investors they would meet in the coming days—and those who had attended today’s event?

What actions would be in the best interest of his client, his firm, his firm’s clients, and the capital markets?

Morgan Stanley

Morgan Stanley was a global financial services firm that provided investment banking, securities,

investment management, and wealth management services. With roots tracing back to 1924, the firm provided

services to clients including corporations, governments, institutions, and individuals in 43 countries. As

illustrated in Table 1, Morgan Stanley was organized along three lines of business.

Table 1. Morgan Stanley business units.

Institutional Securities

Investment Banking

Capital raising

Corporate lending

Financial advisory services,

including advice on mergers and

acquisitions, restructurings, real

estate and project finance

Sales, Trading, Financing and

Market-Making Activities

Equity securities and related

products

Fixed-income securities and

related products, including foreign

exchange and commodities

Other Activities

Research

Prime Brokerage

Global Wealth Management

Clients

Individuals

Small- to medium-size businesses

and institutions

Asset Management

Global Asset Management Products and Services

Equity

Fixed Income

Alternatives

Products and Services

Brokerage and investment advisory

services

Financial and wealth planning

services

Annuity and insurance products

Credit and other lending products

Banking and cash management

Retirement plan services

Trust services

Three Principal Distribution Channels

A proprietary channel consisting of Morgan

Stanley’s representatives

A nonproprietary channel consisting of thirdparty broker-dealers, banks, financial planners,

and other intermediaries

An institutional channel that provides

advisory services and global portfolio

solutions to corporations, central banks,

sovereign wealth funds, endowments,

foundations, public pensions, insurance

general accounts, and financial institutions

Data source: “Organization Chart,” http://www.morganstanley.com/about-us-governance/orgchart.html (accessed Jul. 22, 2015).

Distribuido por IESE Publishing. Si necesita más copias, contáctenos: www.iesep.com. Todos los derechos reservados.

Páginas de uso exclusivo promocional. Puede adquirir la versión completa en www.iesep.com

Page 3

UVA-F-1737

As seen in Table 2, the Institutional Securities division was both the largest and most profitable of the

three business units. In 2011, the firm ranked #1 in global completed mergers and acquisitions and #2 in global

IPOs, earning $4.2 billion in net revenues from investment banking. Equity sales and trading and fixed-income

and commodities sales and trading contributed net revenues of $6.8 billion and $7.5 billion, respectively. The

Global Wealth Management group contributed net revenues of $13.4 billion and pretax income of $1.28 billion

in 2011. The group’s more than 17,000 global representatives managed client assets of $1.6 trillion. The much

smaller Asset Management division contributed net revenues of $1.9 billion and pretax income of $253 million

with $287 billion in assets under management as of December 31, 2011.2

Table 2. Business segment results (in millions of dollars).

FY2011

FY2010

Institutional Securities

Net Revenues* Pretax Income

$17,208

$4,585

$16,169

$4,372

Global Wealth Management

Asset Management

Net Revenues Pretax Income Net Revenues Pretax Income

$13,423

$1,276

$1,887

$253

$12,636

$1,156

$2,685

$718

*Net

revenues for FY2011, FY2010, include positive (negative) revenue from DVA (Debt Valuation Adjustment) of $3.7 billion and –$873

million, respectively.

Like many firms in the heavily regulated financial services industry, Morgan Stanley had a written code of

conduct that governed employee conduct. Excerpts of the code appear in Exhibit 3.

Grimes, a managing director and co-head of Global Technology Investment Banking, worked in the firm’s

San Francisco office. In his role as investment banker, Grimes helped corporate clients with mergers and

acquisitions, debt offerings, and IPOs. With degrees in electrical engineering and computer science from

University of California, Berkeley, he had carved a niche for himself in the technology sector, working on deals

for AMD, Avaya, EMC, HP, Seagate Technology, Microsoft, Netflix, Oracle, and Google. Forbes recognized

Grimes as the top-ranked investment banker in the technology sector in 2004, 2005, 2006, and 2010. In 2010,

Fortune named him one of the “50 Smartest People in Tech.” By 2012, he had worked on hundreds of deals

with a cumulative value exceeding $200 billion.

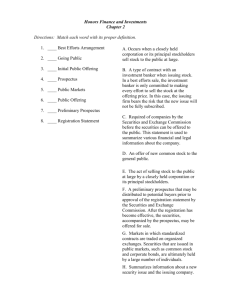

Going Public: IPOs in the United States

U.S. securities offerings were regulated by the U.S. Securities and Exchange Commission (SEC). The

Securities Act of 1933, sometimes referred to as the “truth in securities” law, prohibited deceit,

misrepresentations, and fraud in the sale of securities and required disclosure of financial and other significant

information relating to securities offered for public sale. Companies made the required disclosures in the

prospectus, or offering document, provided to potential investors. Offering documents did not include

projected financial statements or forecasts.

Prior to a securities offering, the issuing company drafted a preliminary prospectus, which it filed with the

SEC as part of the required securities registration statement—Form S-1 for companies seeking a public

offering.3 The preliminary prospectus included material facts about the company, the offering, selling

shareholders, historical financial statements, and risk factors, enabling investors to make informed decisions

prior to purchasing securities. Certain details about the offering, such as the price and exact number of shares

offered, were omitted from the preliminary prospectus and included only in the final registration statement.

2

Morgan Stanley, “Morgan Stanley Reports Full Year and Fourth Quarter 2011,” https://www.morganstanley.com/about-usir/shareholder/4q2011.html#intro (accessed Jul. 22, 2015).

3 Certain offerings were exempt from the registration requirement. These included private offerings to a limited number of individuals or entities,

offerings of limited size, and offerings of municipal, state, and federal government securities.

Distribuido por IESE Publishing. Si necesita más copias, contáctenos: www.iesep.com. Todos los derechos reservados.

Page 4

UVA-F-1737

The preliminary prospectus included a prominent disclaimer in red ink stating:

Páginas de uso exclusivo promocional. Puede adquirir la versión completa en www.iesep.com

The information in this prospectus is not complete and may be changed. Neither we nor the selling

stockholders may sell securities until the registration statement filed with the Securities and Exchange

Commission is effective. This prospectus is not an offer to sell these securities and neither we nor the

selling stockholders are soliciting offers to buy these securities in any state where the offer or sale is

not permitted.

Because it was incomplete and included the prominent red ink, the preliminary prospectus was sometimes

referred to as the “red herring” prospectus.4

Once submitted, the SEC’s Division of Corporate Finance reviewed the registration statement for

thoroughness and clarity to ensure that potential investors would be adequately informed. The SEC would then

provide comments, which the company would often address via an amendment to the S-1, known as an S-1/A.

Potential investors could review the registration statement and indicate interest in participating in the offering,

but could not place orders based on the preliminary prospectus. According to securities regulations, investment

banks could only solicit and accept orders to purchase shares in the offering after the SEC had approved the

registration and the final prospectus with the offering price and other details of the offering had been delivered

to the investor.

As part of its mandate to protect investors, the SEC sought to ensure that communications and offering

documents regarding securities offerings contained appropriate disclosures. The SEC interpreted the term

“offer” broadly. It had cautioned firms that publicity prior to a proposed offering could be considered an effort

to create interest for the purpose of marketing and selling the securities to be offered and thus subject to the

regulators’ disclosure requirements and oversight.

The SEC limited what information a company and related parties could release to the public during the

time period between the company’s initial filing and when SEC staff declared the registration statement

effective. This period was known as the “waiting period.” Because of the limitations on releasing information,

some referred to the period as the “quiet period.” The intent of such regulations was to protect investors from

aggressive promotion of securities offerings.

While not a legal requirement, privately held companies in the United States often hired investment banks

to assist in the IPO process. Investment banks provided valuable experience in marketing and distributing the

offering to investors and navigating the regulatory requirements in accordance with U.S. securities regulations.

As part of marketing and distributing the offering to investors, investment bankers provided advice on the

timing and pricing of IPOs. Investment banks could also underwrite the securities offering, buying the securities

from the issuing company at a discount and then offering the securities to the public at the offering price. The

offering company received its capital in advance from the investment bank, which was responsible for selling

the securities to investors. An investment bank with a strong distribution channel of brokers and financial

advisers was able to market and sell the securities directly to its institutional and/or retail investors, reducing

the risk of underwriting the offering. For large offerings, the investment bank would organize and lead a

syndicate, or group of financial firms that would participate in the deal to market and distribute the new offering.

With a syndicate, each firm underwrote a portion of the offering and was then responsible for marketing and

distributing the shares it purchased.

4

The term “red herring” is often used to refer to something that misleads or distracts from the relevant or important issue.

Distribuido por IESE Publishing. Si necesita más copias, contáctenos: www.iesep.com. Todos los derechos reservados.