1b. GAAP Exercise

advertisement

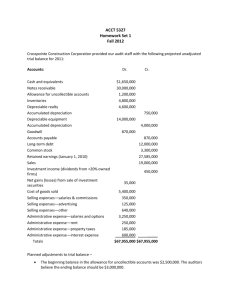

GAAP EXERCISE 1. Review: What does G.A.A.P. stand for? 2. Research: When this course is offered 5 years from now – why may GAAP not be part of the curriculum? 3. Match the GAAP with its description and a case in which the GAAP had been violated. Copy and paste the matching description and case into the chart Accounting Concepts and GAAPs 1. Business Entity Concept 2. Going Concern Concept 3. Time Period Concept 4. Monetary Unit Assumption 5. Principle of Conservatism 6. Objectivity Principle 7. Revenue Recognition Convention 8. Expense Recognition Convention 9. Matching Principle 10. Cost Principle 11. Consistency Principle 12. Materiality Principle 13. Full Disclosure Principle Description Case GAAP Descriptions a) The accounting for a business or organization is kept separate from the personal affairs of its owner, other business or organization. b) Each expense related to revenue earned must be recorded in the same accounting period as the revenue it helps to earn. c) Accounting for purchases must be recorded and remain at their cost price. d) Accountants should apply the same methods and procedures from period to period. When changes are made, they must be explained clearly on the financial statements. e) Any and all information that affects the full understanding of a company’s financial statements must be included with the financial statements. f) Revenue should be taken into account at the time the transaction is completed. g) Expenses are recorded when benefit is used up to generate revenue h) Assumes that a business will continue to operate unless it is known otherwise. i) Accounting takes place over specific time periods known as fiscal periods. The fiscal periods should be of equal legth when used to measure the financial progress of the business. j) The accounting will be recorded on objective evidence. Different people looking at the evidence will arrive at the same value for the transaction. k) Accountants are required to use GAAPs except when to do so would be expensive or difficult and where it makes no real difference to the decisions of users of the financial statements. l) Accounting measures and reports the results of economic activities in terms of a stable monetary unit. m) The accounting for a business should be fair and reasonable. The results should not overstate nor understate the affairs of the business. CASES OF VIOLATION i) A company always recorded purchases in the Cost of Goods Sold account (expense) whether or not the merchandise had been sold. ii) A company has produced financial statements for years without any date or fiscal period identified on them. iii) R. Brueht owns a construction company and believes because he is the owner, no accounting entries are needed when he removes lumber from the job-site to add a deck to his house. iv) A company changed their method of amortizing every two years. v) A used appliance store works on the cash and barter business. The bookkeeper is confused about how to record an entry, where a customer received a stove and in return owes the store 15 hours of plumbing labour. vi) A company debited $15 to Office Equipment for the purchase of a new pencil sharpener which will be used by the business for the next 5 years. vii) A company prepared an unclassified set of financial statements. viii) M. Elliot, after three business failures, has opened a new restaurant. When calculating the life expectancy of her new equipment, it never entered her mind how long the equipment could be used for, but only how long she felt the business would last. ix) A company recorded the purchase of land at cost price and then realized the value was greatly underestimated. They wanted to change the price based on the current market value of the property. x) A company wrote the value of their equipment down to its estimated disposal value in order to lower net income for the year. xi) A company selling franchises charges a franchise fee lasting 20 years. They wanted to show the entire fee as revenue in the year they sold the franchise. xii) A company recorded the payment for a one year insurance policy by debiting Insurance Expense. xiii) A company, after considering the resale value to properties close to theirs, tripled the value of land on their general ledger and recorded a Gain on value of Land (a revenue account).