FA Chapter 13 SM

advertisement

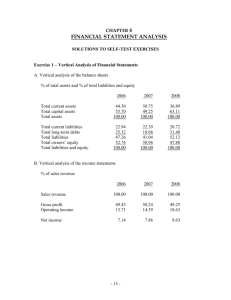

EXERCISES Exercise 13-1 (20 minutes) 2010 Sales........................................189 Cost of goods sold ................191 Accounts receivable ..............201 2009 181 182 192 2008 168 172 182 2007 156 159 169 2006 100 100 100 Analysis: The trend in sales is positive. While this is better than no growth, one cannot definitively say whether the sales trend is favorable without additional information about the economic conditions in which this trend occurred such as inflation rates and competitors’ performances. Given the trend in sales, the comparative trends in both cost of goods sold and accounts receivable are somewhat unfavorable. In particular, for the most recent year, both are increasing at slightly faster rates (indexes for cost of goods sold is 191 and accounts receivable is 201) compared to sales (index is 189). Exercise 13-2 (25 minutes) Answer: Net income decreased. Supporting calculations: When the sum of each year's common-size cost of goods sold and total expenses is subtracted from the common-size sales percent, the net income percent is as follows: 2007 net income percent: 100.0 - 59.1 - 15.1 = 25.8% of sales 2008 net income percent: 100.0 - 61.9 - 14.8 = 23.3% of sales 2009 net income percent: 100.0 - 63.4 - 15.3 = 21.3% of sales Next, notice that if 2007 sales are assumed to be $100, then sales for 2008 are $104.20 and the sales for 2009 are $105.40. If the net income percents for the three years are applied to these amounts, the net incomes are: 2007 net income: $100.00 x 25.8% = $25.80 2008 net income: $104.20 x 23.3% = $24.28 2009 net income: $105.40 x 21.3% = $22.45 This shows that net income decreased over the three-year period. ©McGraw-Hill Companies, 2008 Solutions Manual, Chapter 13 671 Exercise 13-3 (25 minutes) Sales.................................................... Cost of goods sold ............................ Gross profit ........................................ Operating expenses........................... Net income.......................................... 2008 100.0% 75.7 24.3 17.3 7.0% 2007 100.0% 46.5 53.5 35.0 18.5% Analysis: Overall, this company’s situation has worsened. This is evident from the substantial decline in net income as a percent of sales for 2008 (7.0%) relative to 2007 (18.5%). The main culprit is the increase in cost of goods sold as a percent of sales from 46.5% in 2007 to 75.7% in 2008. On a somewhat positive note, the company has not experienced any increase in operating expenses as a percent of sales; indeed, declining from 35.0% in 2007 to 17.3% in 2008. Even more positive is the company’s level of sales increase from $625,000 in 2007 to $740,000 in 2008. Exercise 13-4 (30 minutes) Parker has a greater amount of working capital. This by itself does not indicate whether the company is more capable of meeting its current obligations. However, support is provided by the current ratio and acid-test ratio, which show Parker is in a more liquid position than Morgan. This evidence does not mean that Morgan's liquidity is inadequate. Such a conclusion would require more information such as norms for the industry or its other competitors. Notably, Morgan's acid-test ratios approximate the traditional rule of thumb (1 to 1). This evidence also shows that Parker's working capital, current ratio, and acid-test ratio all increased dramatically over the three-year period. This trend toward greater liquidity may be positive, but it can also suggest that Parker holds an excess amount of highly liquid assets that typically earn low returns. The accounts receivable turnover and inventory turnover indicate that Morgan is more efficient in collecting its accounts receivable and in generating sales from available inventory. However, these statistics also may suggest that Morgan is too conservative in granting credit and investing in inventory. This could have a negative impact on sales and net income. Parker's ratios may be acceptable, but no definitive determination can be made without having information on industry (or other competitors’) standards. ©McGraw-Hill Companies, 2008 672 Financial Accounting, 4th Edition Exercise 13-5 (30 minutes) COMPARATIVE ANALYSIS REPORT Clay's profit margins are higher than Roak's. However, Roak has significantly higher total asset turnover ratios. As a result, Roak generates a substantially higher return on total assets. The trends of both companies include evidence of growth in sales, total asset turnover, and return on total assets. However, Clay's rates of improvement are better than Roak's. These differences may result from the fact that Clay is only three years old, while Roak is a somewhat more established company. Clay's operations are considerably smaller than Roak's, but that will not persist many more years if both companies continue to grow at their current rates. To some extent, Roak's higher total asset turnover ratios may result from the fact that its assets may have been purchased years earlier. If the turnover calculations had been based on current values, the differences might be less striking. The relative ages of the assets also may explain some of the difference in profit margins. Assuming Clay's assets are newer, they may require smaller maintenance expenses. Finally, Roak successfully employed financial leverage in 2010. Its return on total assets is 9.0% compared to the 7% interest rate it paid to obtain financing from creditors. In contrast, Clay's return is only 5.9% as compared to the 7% interest rate paid to creditors. ©McGraw-Hill Companies, 2008 Solutions Manual, Chapter 13 673 Exercise 13-6 (20 minutes) Simeon Company Common-Size Comparative Balance Sheets December 31, 2007-2009 At December 31 2009 2008* 2007 Assets Cash ................................................................... 6.1% 8.0% 10.0% Accounts receivable, net .................................. 17.1 14.0 13.3 Merchandise inventory ..................................... 21.5 18.5 14.3 Prepaid expenses .............................................. 2.0 2.1 1.3 Plant assets, net ............................................... 53.3 57.3 61.1 100.0% 100.0% Total assets ....................................................... 100.0% Liabilities and Equity Accounts payable ............................................. Long-term notes payable secured by mortgages on plant assets .......................... 24.8% 16.9% 13.6% 18.8 22.9 22.1 Common stock, $10 par value ......................... 31.3 36.7 43.3 Retained earnings ............................................ 25.1 23.5 21.0 100.0% 100.0% Total liabilities and equity ................................ 100.0% * Column does not equal 100.0 due to rounding. Analysis: Several observations can be made. (1) Cash as a percent of assets has declined—this is favorable provided sufficient cash is available for operations. (2) Accounts receivable have increased as a percent of assets—this may be unfavorable in that assets are tied up in an unproductive manner and there would be additional assets exposed to the risk of uncollection; it could be favorable if increased sales outweigh these costs and risk. (3) Plant assets have declined as a percent of assets—this is favorable if the company is operating more efficiently; it could be unfavorable if the company is downsizing due to poor performance. (4) Accounts payable have markedly increased as a percent of assets—this could reveal liquidity constraints. ©McGraw-Hill Companies, 2008 674 Financial Accounting, 4th Edition Exercise 13-7 (25 minutes) 1. 2. Current ratio 2009: $31,800 + $89,500 + $112,500 + $10,700 $129,900 = 1.88 to 1 2008: $35,625 + $62,500 + $82,500 + $9,375 $75,250 = 2.52 to 1 2007: $37,800 + $50,200 + $54,000 + $5,000 $51,250 = 2.87 to 1 Acid-test ratio 2009: $31,800 + $89,500 $129,900 = 0.93 to 1 2008: $35,625 + $62,500 $75,250 = 1.30 to 1 2007: $37,800 + $50,200 $51,250 = 1.72 to 1 Analysis and Interpretation: Simeon's short-term liquidity position has deteriorated over this three-year period. Both the current and acid-test ratios show declining trends. Although we do not have information about the nature of the company's business, the acid-test ratio shifts from ‘1.72 to 1’ down to ‘0.93 to 1’ and the current ratio shifts from ‘2.87 to 1’ down to ‘1.88 to 1’—both suggest a potential liquidity problem. Still, we must recognize that industry standards could show that the 2007 ratios were too high (instead of 2009 ratios as being too low). ©McGraw-Hill Companies, 2008 Solutions Manual, Chapter 13 675 Exercise 13-8 (25 minutes) 1. 2. 3. 4. Days' sales uncollected 2009: $89,500 x 365 = 48.5 days $673,500 2008: $62,500 x 365 = 42.9 days $532,000 Accounts receivable turnover 2009: $673,500 ($89,500 + $62,500)/2 = 8.9 times 2008: $532,000 ($62,500 + $50,200)/2 = 9.4 times Inventory turnover 2009: $411,225 = 4.2 times ($112,500 + $82,500)/2 2008: $345,500 ($82,500 + $54,000)/2 = 5.1 times Days’ sales in inventory 2009: 2008: $112,500 $411,225 x 365 = 99.9 days $82,500 x 365 = 87.2 days $345,500 Analysis and Interpretation: The number of days' sales uncollected has increased and the accounts receivable turnover has declined. Also, the inventory turnover has decreased and days’ sales in inventory has increased. While none of these changes in ratios that occurred from 2008 to 2009 appear dramatic, it seems that Simeon is becoming less efficient in managing its inventory and in collecting its receivables. ©McGraw-Hill Companies, 2008 676 Financial Accounting, 4th Edition Exercise 13-9 (25 minutes) 1. Debt and equity ratios 2009 2008 Total liabilities and debt ratio $129,900 + $98,500 ....................... $228,400 43.7% $75,250 + $101,500 ....................... $176,750 39.7% Total equity and equity ratio $163,500 + $131,100 .....................294,600 56.3 $163,500 + $104,750 ..................... _______ _____ Total liabilities and equity ............... $523,000 100.0% 268,250 60.3 $445,000 100.0% 2. Debt-to-equity ratio 2009: $228,400 / $294,600 = 0.78 to 1 2008: $176,750 / $268,250 = 0.66 to 1 3. Times interest earned 2009: ($31,100 + $9,525 + $12,100) / $12,100 = 4.4 times 2009: ($29,375 + $8,845 + $13,300) / $13,300 = 3.9 times Analysis and Interpretation: Simeon added debt to its capital structure during 2009, with the result that the debt ratio increased from 39.7% to 43.7%. In addition, the debt-to-equity ratio also increased from 0.66 to 1 to 0.78 to 1. We should note that the debt increase is mostly in current liabilities, which places a greater stress on short-term liquidity. ©McGraw-Hill Companies, 2008 Solutions Manual, Chapter 13 677 Exercise 13-10 (30 minutes) 1. Profit margin 2009: $31,100 / $673,500 = 4.6% 2008: $29,375 / $532,000 = 5.5% 2. 3. Total asset turnover 2009: $673,500 = 1.4 times ($523,000 + $445,000)/2 2008: $532,000 = 1.3 times ($445,000 + $377,500)/2 Return on total assets 2009: $31,100 ($523,000 + $445,000)/2 = 6.4% 2008: $29,375 ($445,000 + $377,500)/2 = 7.1% Analysis and Interpretation: Simeon's operating efficiency appears to be declining because the return on total assets decreased from 7.1% to 6.4%. While the total asset turnover favorably increased slightly from 2008 to 2009, the profit margin unfavorably decreased from 5.5% to 4.6%. The decline in profit margin indicates that Simeon's ability to generate net income from sales has declined. ©McGraw-Hill Companies, 2008 678 Financial Accounting, 4th Edition Exercise 13-11 (20 minutes) 1. 2. Return on common stockholders' equity 2009: $31,100 ($294,600 + $268,250)/2 = 11.1% 2008: $29,375 ($268,250 + $242,750)/2 = 11.5% Price-earnings ratio, December 31 2009: $30 / $1.90 = 15.8 2008: $28 / $1.80 = 15.6 3. Dividend yield 2009: $0.29 / $30 = 0.1% 2008: $0.24 / $28 = 0.9% Analysis and interpretation The company’s return on common stockholders’ equity is good, but not great. An 11% return makes it an acceptable investment provided its risk is not too high. The company’s price-earnings ratio is around 16. This suggests that the market does view this company to have some growth potential. The dividend yield is on the low side. Thus, this stock would likely be classified as a “growth” stock, and the price-earnings ratio suggests that the market does perceive a high likelihood of some growth. Exercise 13-12A (10 minutes) 1. 2. 3. 4. 5. 6. 7. 8 A C A A A B B A Income (loss) from continuing operations Extraordinary gain (loss) Income (loss) from continuing operations Income (loss) from continuing operations Income (loss) from continuing operations Gain (loss) from disposing of a discontinued segment Income (loss) from operating a discontinued segment Income (loss) from continuing operations ©McGraw-Hill Companies, 2008 Solutions Manual, Chapter 13 679 Exercise 13-13 (15 minutes) RANDA MERCHANDISING, INC. Income Statement For Year Ended December 31, 2008 Net sales .......................................................................... Expenses Cost of goods sold ......................................................$1,480,000 Salaries expense ......................................................... 640,000 Depreciation expense ................................................. 232,500 Total expenses ............................................................ Income from continuing operations before taxes ....... $2,900,000 Income taxes expense ................................................... Income from continuing operations ............................. Discontinued segment Loss from operating wholesale business segment (net of tax) ................................................. (444,000) Gain on sale of wholesale business segment (net of tax) ................................................. 775,000 Income before extraordinary gain ................................ 217,000 330,500 2,352,500 547,500 331,000 661,500 Extraordinary gain on condemnation of company property (net of tax).................................... 230,000 Net income ...................................................................... $ 891,500 ©McGraw-Hill Companies, 2008 680 Financial Accounting, 4th Edition ©McGraw-Hill Companies, 2008 Solutions Manual, Chapter 13 681