Chapter One The Accounting Equation and Double

advertisement

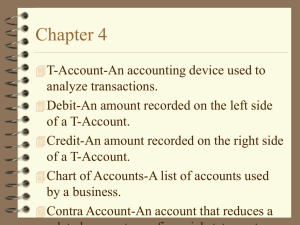

Chapter One The Accounting Equation and Double-entry Bookkeeping I. (1) (2) (3) (4) (5) (6) (7) Learning objectives After completing this session, students should be able to Define assets, liabilities, owner’s equity, revenue and expenses; Understand the functions of the fundamental accounting equation; Record business transactions and illustrate their effects on the fundamental accounting equation; Understand the accounts payable, accounts receivable, prepaid insurance, and drawing accounts; Understand the basic principle of double-entry bookkeeping and the use of Taccount form; Understand the rules of debits and credits; Prepare a trial balance. II. Lecture notes 1. Some important definitions as per the International Accounting Standards (IAS) (1) Assets: economic resources controlled by the business enterprise as a result of past events and from which future economic benefits are expected to flow to the enterprise. Need to emphasize three elements in this definition: control (as compared with ownership), past event, and future economic benefits. Recognition of the elements of financial statements: An item that meets the definition of asset should be recognized if: (a) it is possible that any future economic benefit associated with the item will flow to the enterprise; and (b) the item has a cost or value that can be measured with reliability. Example: Human resources are the most important assets of a company, but why can’t we find them on the financial statement? Some professional football club is an exception to these recognition criteria. (2) Liabilities: the existing obligations of the enterprise arising from past events, the settlement of which is expected to result in a sacrifice of economic benefits of the enterprise. Need to emphasize three elements in this definition: existing obligations, past events, and sacrifice of economic benefits (3) Owner’s equity: the residual interest in the assets of the enterprise after deducting 1-1 all its liabilities. 2. The fundamental accounting equation (1) One side is the reflection of the other side; (2) Provide a simple example to interpret the equation (starting a business, for example, a fruit stand on campus with RMB1,000.) 3. Functions of the fundamental accounting equation (1) shows the financial status and the results of operations of a business; (2) provides a theoretical basis for the preparation of financial statements. Assets = Liabilities + Owner’s equity + Revenue – Expense Balance sheet accounts income statement accounts 4. Recording business transactions (1) Explain transactions (a) – (e) Transaction (a): introducing the Business Entity Concept (separating personal accounts from business accounts) Transaction (c): explain accounts payable Compound entry: an entry involving more than two accounts Vs. Simple entry: an entry involving only two accounts. (2) Explain prepaid insurance (cf. prepaid rent): transaction (e) (3) Accounts: subdivisions under the three main headings. (4) Recording revenue and expenses A. definitions of revenue and expenses Revenue: Revenue is increase in economic benefits during the accounting period in the form of inflows or enhancement of assets or decreases of liabilities that result in increase in equity, other than those relating to contributions from equity participants. Expenses: are decreases in economic benefits during the accounting period in the form of outflows or reductions of asset or increases of liabilities that result in decreases in equity, other than those relating to distributions to equity participants. (cf. definition on textbook, p.21) 1-2 5. Double-entry bookkeeping (1) Each transaction must be recorded in the accounting records and will cause increase or decrease in the assets, liabilities or owner’s equity. But the total of one side of the fundamental equation should always equal the total of the other side. (2) Helpful for checking arithmetic errors. 6. The T-account form (1) What is a T-account form example: Cash + debit credit Accounts payable + debit credit Explain debits, credits, footing, debit balance, credit balance * Difference between footings (i.e., balance) always falls on the side with a bigger footing (usually on the plus “+”side) 7. Explain the complete accounting equation and the placement of T accounts Assets + - = Liabilities + + Owner’s equity + + Revenue - + - Expenses + - Drawing + - * The minus “-“side of revenue account and the minus “-“side of expense account will not be used. Explain transaction (k) * This is an internal transaction (not real transaction) and is a decrease in investment by the owner. * Withdrawals by the owner may take any form of assets, not just limited to cash. 8. Trial balance (1) What is a trial balance? (2) Importance of the trial balance – it is no use preparing financial statements if there are errors in records. 1-3 (3) Locating errors A. Procedures: start from the most recent transactions B. Some common errors Transposition: 169 196 Slide: 1.69 16.9 Recording the debit or credit side twice 9. Assignment for this chapter Problem 3 (p.33, to be done as an individual homework. Students need to follow the format on p.28) 1-4