SARBANES-OXLEY ACT OF 2002 - ucsc.edu) and Media Services

advertisement

and Media Services")

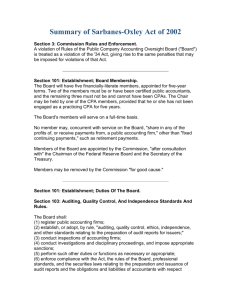

SARBANES-OXLEY ACT OF 2002 Purpose: In response to the Arthur Anderson, Enron and WorldCom debacle, the Sarbanes-Oxley Act seeks to restore the public confidence in both public accounting and publicly traded securities. Objectives: To assure ethical business practices through heightened levels of executive awareness and accountability. TITLE I – PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD Sec. 101 ESTABLISHMENT; ADMINISTRATIVE PROVISIONS The Public Company Accounting Oversight Board (the Board) will oversee audit of public companies The board will be a “body corporate” – it will be operated as if it were a non-profit entity Duties of the Board include (1) the registration of public accounting firms that prepare audits for the Issuer (issuer of publicly traded securities), (2) to establish and amend accounting standards, (3) to conduct inspections of registered public accounting firms (RPAF), and to (4) enforce compliance Composition of the board: 5 members, all appointees; only two members may be Certified Public Accountants; board membership is considered full-time, therefore members may not be otherwise employed or have other affiliations; the terms of service are 5 years per term with a maximum of two terms served Sec. 103 AUDITING, QUALITY CONTROL, AND INDEPENDENCE STANDARDS AND RULES RULE REQUIREMENTS o The Board will include in auditing standards it adopts the requirement that each RPAF will: Prepare and maintain audit reports and related workpapers for at least 7 years Conduct concurring or second partner reviews of audit reports Test an entity’s internal controls o The board will cooperate with professional groups of accountants (FASB, AICPA, etc.) It will recommend issues to be included in agendas of such groups It will take steps deemed appropriate to increase standard setting effectiveness i.e., the Board will have significant influence over existing standard-setters Sec. 104 INSPECTIONS OF REGISTERED PUBLIC ACCOUNTING FIRMS (RPAFs)* In order to assess degree of compliance Inspections occur yearly for each RPAF which audits more than 100 Issuers, every 3 years (at least) for each RPAF which audits 100 or less Issuers Inspections are conducted by selecting audit engagements for review (i.e., auditing an audit) * A REGISTERED PUBLIC ACCOUNTING FIRM MEANS A PUBLIC ACCOUNTING FIRM REGISTERED WIT THE BOARD IN ACCORDANCE WITH THIS ACT Sec. 105 INVESTIGATIONS AND DISCIPLINARY PROCEEDINGS The Board may conduct an investigation of any act or omission to act by an RPAF and/or any associate of an RPAF The Board may require testimony from any RPAF or its associates, and require the production of audit workpapers or relevant documentation; this also applies to any other person, including clients of the RPAF in question The Board may bring charges to the RPAF or associated person(s), who will be subject to a non-public hearing If said firm or associate is found in violation, penalties include: o Temporary suspension or permanent revocation or registration o Bar from future association with any other RPAF o o o o Limitations on activities any RPAF or individual may engage in Civil money penalties Censure Required further education Sec. 106 FOREIGN PUBLIC ACCOUNTING FIRMS In short, in certain situations certain foreign public accounting firms are subject to aforementioned regulations by the Board Sec. 107 COMMISSION (as in Securities and Exchange Commission) OVERSIGHT OF THE BOARD In the eyes of the Commission, the Board is a “registered securities association”; as such, the Commission shall have oversight and enforcement authority over the Board No rule of the Board shall become effective w/out Commission approval The Commission retains the right to amend any Board rule The Board’s sanctions of any RPAF and/or associate are filed with the Commission, which shall review any final disciplinary actions taken The Commission retains the modification authority, which allows it to enhance, modify, cancel, reduce, or require the remission of a sanction imposed by the Board upon an RPAF or associated person The Commission may censure or impose limitation upon the activities, functions, and operations of the Board in the case that the board has violated and provisions of the Sarbanes-Oxley Act (the Act), the rules of the board, or security laws; or fails to enforce compliance The Commission may remove from office or censure any member of the Board if said member violates any provisions of the Act, rules of the board or securities law, willfully abuses their authority, or fails to enforce compliance TITLE II – AUDITOR INDEPENDENCE Sec. 201 SERVICES OUTSIDE THE SCOPE OF PRACTICE OF AUDITORS Prohibited activities – It is unlawful for any RPAF that performs audits for any Issuer to perform any non-audit functions listed below: o Bookkeeping o Financial information systems design and implementation o Appraisal or valuation services o Actuarial services o Internal audit outsourcing services o Management functions or human resources o Broker or dealer, investment advisor, or investment banking services o Legal/expert services unrelated to the audit o Any other service the Board deems impermissible Any other non-audit service provided, including but not limited to tax, must per pre-approved by the board Sec. 202 PRE-APPROVAL REQUIREMENTS Any audit service provided by an RPAF to an issuer requires a pre-approval process Any non-audit function performed by the auditor for the issuer must be disclosed in financial statements Sec. 203 AUDIT PARTNER ROTATION Lead or coordinating partners of audits of issuers may not provide audit services for more than 5 consecutive years to one particular issuer Sec. 204 AUDITOR REPORTS TO AUDIT COMMITTEES RPAFs performing audits to issuers must report to said issuer’s audit committees: o “All critical accounting policies and practices to be used” o All alternative disclosure treatments of financial information within Generally Accepted Accounting Principles (GAAP) discussed with management and the ramifications of such, and which treatment is preferred by the RPAF o Any written material between the RPAF and management Sec. 206 CONFLICTS OF INTEREST An RPAF may not perform audit services for an issuer if a CEO, controller, CFO, chief accounting officer, or equivalent title of the issuer was employed by said RPAF and participated in any capacity in the audit of that issuer during the 1-year period preceding the date of the initiation of the (current) audit Sec. 207 STUDY OF MANDATORY ROTATION OF REGISTERED ACCOUNTING FIRMS The Comptroller General of the United States will investigate the possibility of mandatory rotations – a limit to the amount of time one particular RPAF may serve as auditor of a particular issuer TITLE III – CORPORATE RESPONSIBILITY Sec. 301 PUBLIC COMPANY AUDIT COMMITTEES Audit Committee (committee established by the board of directors of an issuer, composed of board members, for the purpose of overseeing the accounting and financial reporting processes of the issuer and audits of the financial statements of the issuer) Independence o This section establishes minimum independence standards for the audit committee o Requires the audit committee to appoint, compensate, oversee the work of the independent auditor (RPAF) o Sets guidelines for the audit committee to establish procedures for addressing complaints by the issuer regarding accounting, internal control, etc. This allows for installation of procedures for handling anonymous tip-offs, or whistleblowing Sec. 302 CORPORATE RESPONSIBILITY FOR FINANCIAL REPORTS The Commission requires for each company filing periodic financial reports, the principal executive and principal financial officer(s), to certify in each annual or quarterly report filed, that: o The signing officer has reviewed the report o The report does not contain any untrue statement of material fact or omit any material fact (to the best of the officer’s knowledge) o (to the best of the officer’s knowledge) the financial statements fairly represent the financial position of the issuer o The signing officers are responsible for establishing and maintaining internal controls, and have within the last 90 days of the report issuance evaluated the effectiveness of these controls o The signing officers have also disclosed to the RPAF and the audit committee any deficiencies in the design of the internal controls, any fraud, and whether or not there were any significant changes in the controls Sec. 304 FORFEITURE OF CERTAIN BONUSES AND PROFITS If an issuer is required to prepare an accounting restatement due to the material noncompliance of the issuer as a result of misconduct, the CEO and CFO must forfeit: o Any bonus or equity-based compensation received by that person from the issuer during the 12month period following the first public issuance or filing of the mis-stated document o Any profits realized from the sale of securities during the same 12-month period Sec. 307 RULES OF PROFESSIONAL RESPONSIBILITY FOR ATTORNEYS Any attorney appearing and practicing before the Commission in representation of an issuer must report evidence of material violation of securities to chief legal counsel or the CEO; if aforementioned parties do not respond, it is the attorney’s responsibility to report to the audit committee or board of directors TITLE IV – ENHANCED FINANCIAL DISCLOSURES Sec. 401 DISCLOSURES IN PERIODIC REPORTS Issuers must disclose off-balance sheet arrangements and known contractual obligations in each quarterly/annual financial report required to be filed with the Commission Any non-GAAP results must be reconciled to GAAP; also, disclosure of why non-GAAP result was preferential Sec. 402 ENHANCED CONFLICT OF INTEREST PROVISIONS Prohibits extension of credit, in the form of a personal loan, to or for any director or executive officer o Certain exceptions to this rule apply (e.g., open credit plans, charge cards) Sec. 404 MANAGEMENT ASSESSMENT OF INTERNAL CONTROLS Annual reports shall contain an internal control report, which shall: o State the responsibility of management for establishing and maintaining an adequate internal control structure and procedures for financial reporting o Contain an assessment of the effectiveness of the internal control structure Additionally, the registered public accounting firm which provides audit services for the issuer must attest to the internal control report made by the management of the issuer Sec. 406 CODE OF ETHICS FOR SENIOR FINANCIAL OFFICERS In periodic financial reports filed with the Commission, the issuer must disclose its code of ethics for senior financial officers, and if the issuer has not adopted such a code, must disclose why Sec. 407 DISCLOSURE OF AUDIT COMMITTEE FINANCIAL EXPERT Issuer must disclose in periodic reports whether or not the audit committee is comprised of at least one financial expert, and if not, why o A member is considered a financial expert if they have: An understanding of GAAP Experience preparing/auditing financial statements of comparable entities Experience with internal controls An understanding of audit committee functions Sec. 408 ENHANCED REVIEWS OF PERIODIC DISCLOSURES BY ISSUERS The Commission shall review disclosures made by issuers which have a class of securities listed on a national securities exchange or traded on an automated quotations system; reviews will be of an issuer’s financial statement o While issuers subject to review at any given time is based upon various criteria, all issuers will be subject to review at least once every 3 years Sec. 409 REAL TIME ISSUER DISCLOSURES Each issuer shall disclose to the public on a rapid and current basis such additional information concerning material changes in the financial condition or operations of the issuer in plain English TITLE V – ANALYST CONFLICTS OF INTEREST Sec. 501 TREATMENT OF SECURITIES ANALYSTS BY REGISTERED SECURITIES ASSOCIATIONS AND NATIONAL SECURITIES EXCHANGES