Impact des entrées-sorties de l'indice CAC40

advertisement

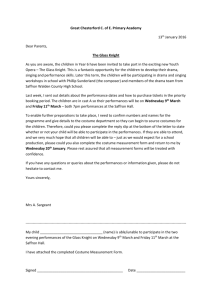

Market behavior around stock index revisions Meriam BOUSSEMA* Sandrine LARDIC** (corresponding author) Abstract: The purpose of this paper is to investigate the price and volume reactions around stock index revisions. This study uses CAC40 intraday data in the pre and post index revision periods comprised between 1992 and 2001. The impact of index additions or deletions can be interesting from a theoretical as well as from a practical viewpoint. Firstly, the Price Pressure Hypothesis (PPH) can be tested against the Liquidity Cost Hypothesis (LCH) and the Information Content Hypothesis (ICH). Finally, results of the study can help dealers to choose the best moment to buy/sell concerned securities. Key Words: purchasing-sale simulations, profiles of performance, MSCI Indices, CAC 40 index. JEL Classification: C1, G14. * Sinopia AM, mboussema@sinopia.fr ** Sinopia AM et MODEM, slardic@sinopia.fr, lardic@u-paris10.fr, Sinopia AM, 66 rue de la Chaussée d’Antin, 75009 Paris, France. Tel. : 01.53.32.51.03. 1 Market behavior around stock index revisions Introduction Analysis of the impact of index changes (additions or deletions), can be useful from a theoretical and practical point of view. From a theoretical viewpoint, this analysis allows us to know the impact of a particular event on the behavior of the prices and to identify the parameters generating changes in prices (arrival of information, unbalances between supply and demand for the securities,….). From a practical viewpoint, a better knowledge of the additions/deletions impact on returns can help operators, especially portfolio managers not only to choose the time of their intervention, but also to spot possible opportunities of purchases and sales of stocks. Most studies on the subject were carried out with this double perspective. Almost all these studies found that additions/deletions affect the prices and volumes of stocks concerned. However, the length and the causes of this effect were not clearly identified. Harris and Gurel (1986) suggested that index additions can exert a pressure on the prices, because of an increase in the demand or supply in these securities, and thus generate a temporary variation of the prices and volumes of transaction (price pressure hypothesis). If this effect fades out quickly, it means that additions/deletions induce an abnormally high demand/supply (from institutional investors, for example, wishing to replicate the index rather than acting on information they may have come by). Harris and Gurel consider that the existence of an abnormal return is neither due to the arrival of information, nor to a permanent change in the securities’ liquidity. They observed that any abnormal return of the SP500 is completely gone after two weeks. Chung and Kryzanowski (1996) reached the same conclusion for the Canadian index TSE300. 2 Amihud and Mendelson (1986) showed that an index revision is accompanied by a permanent modification of prices and liquidity of the securities concerned (liquidity hypothesis). The authors suggested that this phenomenon is due to the existence of a relation between returns and transaction costs. The liquidity hypothesis asserts that since direct transaction costs affect return of securities, a variation in the security liquidity is accompanied by a modification of the liquidity premium and the security equilibrium value. Within this framework, an index revision should be accompanied by a permanent variation of the level of the transaction costs and by a permanent change of the price level. Lastly, Jain (1987) and Dhillon-Johnson (1991) noted a permanent change in the security prices following its addition into / deletion from an index. They explained this phenomenon by the arrival of information which generates a readjustment of the fundamental value of the stock (information content hypothesis). Actually, this assumption can be accepted if the decision to include a security into / delete it from an index is made on the basis of information and not on criteria of size and liquidity (stock market capitalization or free float). The existence of a persistent abnormal return can be explained by other phenomena, such as a better follow-up by the analysts (in the case of the additions) involving a change in the company value. Moreover, Chung and Kryzanowski (1996) showed that the number of analysts following securities admitted in the index TSE300 increases significantly after the entry. Furthermore, no significant reduction in the number of analysts was noted when a security is dropped from the index. The information content hypothesis was tested by Thomas (1995) for CAC 40 index revisions. Analysing a period of 190 days around the index revision and calculating abnormal returns, this author showed that while additions into the index do not have any perceptible impact, the consequences of deletions from the CAC 40 are more significant even if they weaken progressively. Thomas examined the stability of this result by dividing its sample period in sub-periods and compared the averages of abnormal returns between these different sub-periods. She has concluded that the announcement of a revision produces a significant effect on security returns, the outgoing (entering) values being subject to an abnormal fall (rise) in prices between the announcement and the event. However, once the event is carried out, 3 returns of the admitted securities, like those of the deleted securities, find a level statistically similar to that of the period preceding the announcement. Therefore, the membership premium for being in the CAC 40 index should be limited to the admission premium. The aim of this article is twofold. Firstly, we will show new results confirming or invalidating the different hypotheses stated above. Secondly, we will offer a framework which would help portfolio managers to identify an optimal strategy of purchase/sale concerning the admitted/deleted from the index. For this purpose, we use a sample of three indices : the MSCI US, the MSCI Europe and the French blue chips index, the CAC 40. For the CAC 40 index, we use intra-day returns. Using intra-day data enables us to refine the analysis and to detect the very moment when the effect of the admission or the deletion is most marked. Moreover, using intra-day data makes it possible to have a large number of observations and consequently, more robust results from a statistical point of view, even if, because of the observation frequencies, the results should be also more disturbed. The remainder of this paper will be divided as follows. In the first section, we will present the database as well as the reprocessing carried out in order to make the data exploitable before detailing the calculation of abnormal returns. In the second section, we will analyze the securities’ purchase/sale strategy and determine the best periods to carry out these operations for the three indices selected. In the third section, we will analyze the stability of optimal strategies using all possible purchase/sale dates. In the fourth section, we will concentrate on intra-day data and examine the behavior of the French star index during a revision period. This last analysis permits us in particular to stress the importance of the choice of the times of interventions in the stock market during the day. 4 1. Database and abnormal returns 1.1 The sample Our sample contains three indices: the MSCI US, the MSCI Europe and the CAC 40. For the MSCI indices, we have used daily closing prices going from January 1997 to June 2001. We did not take into account the December 2001 index revisions as it occurred due to purely technical reason1 and it was well anticipated by the market operators long time before the event. For these MSCI indices, the revisions occur quarterly (whereas the CAC40 index can be revised at any time). These quarterly changes relate to a variable number of securities (between 0 and 40) and are carried out according to several criteria. As for the MSCI US index, after reprocessing, we retained 132 securities admitted into the index and 53 securities deleted from it over the period. For the MSCI Europe index, we retained 126 index additions and 125 index deletions. In the case of CAC40 index revisions, the securities added or deleted previous to 1992 were not included in the study as little information was available regarding them. Furthermore, stocks added or deleted after September 1999 were also disregarded as the market opening and closing hours were modified. All data being intra-day, each observation relates to a specific day, hour, minute or second of transaction. As some transactions occurred simultaneously, the data had to be reprocessed. When the prices were not identical, we calculated a volume weighted average price (in general the price of simultaneous transactions is identical). Then, the data were regularized every 10 minutes in order to be able to calculate returns on an homogeneous time basis. 1.2 Calculation of abnormal returns To analyze the price behavior before and after stock index revisions, we calculated abnormal returns of securities concerned by the revision. A simple way of doing so is to estimate the market model over a 1 MSCI has changed its methodology, to increase the target market representation target of the MSCI Standard Equity Indices from 60% of total market capitalization to 85% of free float-adjusted market capitalization within each industry group and within each country. 5 "normal" period of time2 and to extract the residuals of the previous regression. For MSCI indexes, the window chosen to estimate the market model covers a period of two years, ending 29 days prior to the event. This length of the period ensures a good stability of the estimators. For the CAC 40 index, as returns being calculated every 10 minutes, we have retained a shorter period of time (two months) finishing 20 days before the event. The observation of the individual data enables us to draw some conclusions specific to the securities under scrutiny and to detect some anomalies in the data3. However, a more synthetic study was undertaken because of the discrepancy between abnormal returns. Consequently, in this work, we consider only average behaviors of the admitted or deleted securities for each index. We place ourselves from the viewpoint of an investor who would seek to profit from an operation of purchase/sale stocks concerned by the index revision. The question is at which moments should she buy or sell its securities in order to maximize its performance? 2. Simulations of optimal purchase/sale strategies The goal here is to find the best time for an investor to buy (resp. to sell) then to sell (resp. to buy) a security admitted (resp. deleted) into (from) an index. First, we suppose that the investor buys at a specific date a stock for 100$. Then, we calculate how much will he/she earn when selling at successive dates. For each purchase date, we determine the corresponding optimal sale date. The sale date is considered optimal when the profit is maximum. Thus, for an (arbitrary) given date of purchase, we have two pieces of information : the optimal date to sell and the profit associated with this date. We then move to the following date and renew the procedure. And so on … We finally obtain a series of maximum values, for each possible purchase date of the sample. Let us take a concrete example. 2 3 A period before the event (addition or deletion). To keep space, these results are not presented in the text. They are however available upon request. 6 The National Bank of Paris (BNP) entered into the CAC 40 index the 11/17/93. Its admission was announced the 11/12/93( five days before the entry). Date 0 corresponds to the date of admission (see figure 1). On the abscissa axis, the value "-15_36" corresponds to 15 trading days before the admission date of the security in the index and to the 36th interval of time. In 1993, the opening of the stock exchange was at 10H00, the interval 36 thus relates to the 10 minutes interval going from 16H00 to 16H10. The curve shows for each date (couple day_ interval) the maximum abnormal profit that the investor will be able to obtain buying, at this date, for 100 dollars the security BNP. 106 announce 105 entry 104 103 102 101 100 99 98 97 96 DATE -14_27 -12_12 -11_30 -9_9 -8_29 -6_6 -5_25 -3_8 -2_33 0_14 1_32 3_30 5_10 6_28 8_4 9_22 10_40 12_16 13_34 15_11 16_30 18_7 19_29 Figure 1. BNP performances around its entry into the CAC 40 index Figure 1 shows that it was optimal for an investor to buy BNP stocks for 100 $ before its admission in the index, i.e. before the date 0. Suppose he/she decides to buy these stocks after this date, whatever the sale date, he/she will clearly not be able to make a substantial profit (the curve remains close to the value 100$). In addition, the maximum gain he/she can obtain corresponds to a purchase carried out 4 days before the admission (interval 37, value: 105.13). The curve of the figure 1 actually corresponds to the superior envelope of gains for an investor intervening in the market between -15 days and +15 days around the BNP admission into the index. The optimal sale date was not reported in this figure. Consequently, we added this information in figure 2. The missing information on this figure is the date of the corresponding sale in order to obtain these maximum gains. Also, we added one second curve 7 (datemax) on the figure of the performances (cf figure 2), indicating the date of sale for each date of purchase. It is optimal for the investor to sell the security at the date of entry (0_5) if he bought it 4 days before the entry in the index4. Figure 2. BNP performances around its addition into the CAC 40 index It appears in figure 2 that whatever the purchase date between 14 days before the admission and the admission day, the curve corresponding to the maximum price is horizontal. The optimal date to sell the stocks under scrutiny is the admission date. Note also that the optimal period of detention is very short beyond the date of admission into the index, except rare cases. Let us now return to the more general study of the index revisions. As previously, we consider an investor interested by opportunities of gains related to securities admission (deletion) into (from) the MSCI US index. Figures 3 and 4 show performances calculated as before. 4 The sale dates are also read on the abscissa axis. 8 104 102 100 98 96 94 30 28 26 24 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 -29 -26 -23 -20 -17 -14 -11 -8 -5 -2 1 4 7 10 13 16 19 22 25 28 buying date 102 MINDATE MIN 100 98 performance 106 buying date DATEMAX MAX performance sale date 35 30 25 20 15 10 5 0 -5 -10 -15 -20 -25 -30 -35 96 94 92 90 88 -29 -26 -23 -20 -17 -14 -11 -8 -5 -2 1 4 7 10 13 16 19 22 25 28 sale date Figure 3. Performances around admission into the MSCI US index Figure 4. Performances around deletion from the MSCI US index Figure 3 which corresponds to the basket of stocks entering into the MSCI US index is very easy to interpret. It is interesting to buy stocks admitted into the index as soon as possible and to sell them one day before the admission (date -1). After the admission, it is clearly not interesting to adopt a purchase/sale strategy for the stocks concerned by the admission (the curve MAX has a typical stair profile). On the other hand, figure 4 which is about securities deleted from MSCI US index is also interpretable although the stair profile is less clear. This figure shows that it is profitable to sell stocks concerned by deletion as soon as possible and to repurchase them the day before the deletion. Moreover, from the announcement, the gain resulting from such a strategy decreases very quickly. As in the case of the entries, the investor gains are null on average if he adopts a strategy of sale/purchase as soon as the stock comes out of the index. In order to examine the spatial stability of these results, the study is extended to the MSCI Europe index revisions. Results appear on figures 5 and 6. 110 MAX 25 DATEMAX 25 102 10 100 5 98 96 94 92 90 5 0 -5 94 -5 Figure 5 – Stock performances around entry into the MSCI Europe index 98 10 96 7 10 13 16 19 22 25 28 100 MIN 15 0 -29 -26 -23 -20 -17 -14 -11 -8 -5 -2 1 4 buying date 102 MINDATE 20 buying date 104 15 performance 106 20 sale date 30 108 88 86 84 -29 -26 -23 -20 -17 -14 -11 -8 -5 -2 1 4 sale date 7 10 13 16 19 22 25 28 Figure 6 – Stock performances around deletion from the MSCI Europe index The result is identical to that obtained for the American index revisions and appears even stronger in the case of the deleted securities, as the typical “stair” form clearly appears for the European stock 9 performance 30 index (see the curve Max), indicating the absence of possibilities of gains resulting from a purchase/sale strategy beyond the date of deletion. Figure 6 also shows that starting from the date of announcement (9 trading days before the event), the gain derived from the purchase-sale of securities decreases quickly. The “datemax” and “datemin” curves show clearly that the investor must reverse its position the day before the index revision to maximize its performance. Let us now observe the average behavior of the securities of the CAC 40 index. Figures 7 and 8 describe the evolution of performances. sale date 16 14 12 10 8 6 4 106 104 102 100 98 2 0 -15.2 -13.3 -10.2 -7.2 -5.32 -2.17 1.2 3.32 6.17 9.2 11.32 14.17 17.2 19.32 buying date Figure 7. Stock performances around the entry into the CAC40 index 96 buying date 18 108 DATEMAX MAX performance 20 22 20 MINDATE 18 MIN 16 14 12 10 8 6 4 2 0 -2 -4 -15.2 -13.32-10.17 -7.2 -5.32 -2.17 1.2 3.32 6.17 9.2 11.32 14.17 17.2 19.32 sale date Figure 8. Stock performances around the CAC40 index deletions The data used here are more subjected to noises than MSCI data, as they are intra-day. Furthermore, the dates of admission and/or deletions are relatively dispersed. Although the figures 7 and 8 are more difficult to interpret, we find a profile similar to that observed for the other indices, namely a “stair” (for the “Datemax” and “Datemin” curves) and an optimum gain for a strategy of selling/purchasing before the date of the event. 3. Generalization Up to now, we observed only the optimal gains profiles of the investor. However, it is also crucial to obtain information on the stability of these profiles. We saw that it is optimal for an investor in MSCI US index to buy as soon as possible the stock entering into the index and to sell it 1 or 2 days before the admission. Suppose a second investor who would sell his stocks 3 days before the admission or 1 or 2 days after the admission: should s(he) expect a weak profit or even a loss or 10 101 100 99 98 97 96 95 94 93 92 91 performance 22 could s(he) expect a gain profile almost identical to that of the first investor? To answer this question, one should study the stability of performances. In order to study the stability of the performances, we determined the gains carried out by an investor for a date of purchase (respectively of sale) unspecified between -29 and 29 days around the admission (respectively the deletion) and selling (respectively repurchasing) the security at all dates after. Figure 9 gives the result. In this figure as in all that follow, the third axis, namely the performance axis shows the evolution of a portfolio bought 100 $. 120 100-120 100 80-100 60-80 80 40-60 20-40 Performance 60 0-20 40 20 -29 -22 A y -28 0 -15 y -20 -8 y -12 -1 y -4 6 y4 Sale Buy ing 13 y 12 20 y 20 y 28 27 Figure 9. Stock performances around their addition into the MSCI US (all possible dates of purchase and sale) We chose to draw figure 9 in three dimensions in order to have in the same graph the profiles of gains for all the possible dates of purchase and sale. By assumption, this profile is null for a sale preceding the purchase (area labeled A in the figure). This is why performances fall abruptly. The periods of purchase/sale during which it is possible to carry out a gain appear very clearly on this figure: they correspond to the peaks on the surface (inside the circle). It is therefore necessary to buy the security before the index revision and to sell it around the date of admission (- 2 days up to +2/3 days). Outside these periods, the investor is almost assured to carry out a loss. 11 In order to more precisely locate the period during which it is more appropriate to intervene, we have enlarged the highest zone by considering (arbitrary of course) a date of purchase between -29 and -6 days and a date of sale between -6 days and +29 days. Figure 10 reproduces the result. It confirms the previous results, namely it is necessary to buy the admitted stock before the entry and sell around the date of admission. Note a peak in performances 1 day before the event. Note also an asymmetry around this peak: the investor can sell her(is) security 2 or 3 days after the admission and still carry out an important gain, but if s(he) decides to sell it 2 or 3 days before the entry, it has all the chances to carry out only a very weak or even a null gain. Finally, note that the edge corresponding to the peak with the maximum gains is the curve we represented on figure 3 for a date of purchase ranging between -29 and -6 days before the admission into the index. 105-110 100-105 95-100 90-95 85-90 80-85 Performance -29 -24 -19 Buying -14 -9 Sale Figure 10. Stock performances around their addition into the MSCI US index (buying between –29 and –6 days, selling at all possible dates ) Concerning the securities deleted from the MSCI US index (see figures 11 and 12), the interpretation is more difficult, since the profiles of performances appear more unstable (as we already noted concerning figure 4). Remind that on these areas, we seek the lowest values since we adopt a strategy of sale followed by a repurchase of the outgoing security. 12 104 102-104 100-102 98-100 102 96-98 94-96 92-94 100 90-92 88-90 98 96 Performance 94 y -29 92 y -21 y -13 90 y -5 Buy ing y3 88 y 11 y 19 y 27 Sale Figure 11. Stock performances around their deletion from the MSCI US index (all dates of purchase and sale) Figure 11 shows that to have a gain, the investor should sell the security as soon as possible. Concerning the date of repurchase, figure 12 allows us to visualize it better. According to it, it is optimal to repurchase the security at the date of its deletion from the index (or approximately 20 days after the deletion). 99-100 98-99 97-98 96-97 95-96 94-95 93-94 92-93 91-92 90-91 Performance -9 -14 -19 Sale -24 -29 Buying Figure 12. MSCI USD index deletions (sale between –29 et –6 days and repurchasing at all dates) 13 We carried out a similar analysis for the additions/deletions about the MSCI Europe index. To keep space, results similar to those commented here appear only in the appendix. In fine, our analysis shows that in all the cases it is necessary to buy (resp. to sell) as soon as possible and to sell (resp. to buy) the day before the addition (resp. deletion) or the very same day. Performances seem stable around the optimal gain profiles. This stability is however more visible for additions into the index than for deletions from the index. On the other hand, an investor who would liquidate his position 2 or 3 days before the realization of the event would carry out only a very weak or even a null gain. Let turn now to the analysis of performances’ stability inside trading days. If it is now clear that an investor may gain by buying a security admitted into an index as soon as possible and to sell it the day before the admission or 1 to 2 days after, the question is: do performances vary according to the time of investor’s interventions during the day? In other words, has an investor choosing to intervene only at the closing hour for instance has more chance to gain than an investor who systematically intervene at the opening ? To deepen this question, the daily MSCI indexes data we use are closing prices. Concerning the CAC40 index, as underlined before, abnormal returns are calculated on data recorded every ten minutes. Since performances also exhibit a stair profile, we interpret this as a sign of stability inside every trading day. 4. More on intraday data In this section, we use a different perspective. Contrary to previous sections where the analysis is conducted using successive intervals of a day (every 10 minutes of one day in the case of the CAC 40 index), we refer here to identical intervals of successive days (opening prices, closing prices, …). We therefore use daily data observed at fixed times of trading days. Figures 13A to 13D give the results. They refer to an investor who will invest 100 $ during the first ten minutes of a trading day 14 and sell her(is) securities only at opening prices of following days. We suppose here that her(is) interventions occur only at opening prices. More precisely, each figure corresponds to a 10 minutes interval. Thus, the interval " 2 " of the figure 13A corresponds to the series in the range 10H1010H20. We suppose the investor buy/sell securities only during these ten minutes between –15 days and + 20 days around the date of admission (date 0). 21 101.2 18 15 DATEMAX 101 MAX 100.8 100.6 12 100.4 9 100.2 6 100 99.8 3 99.6 0 99.4 -3 -6 99.2 -15.2 -10.2 -5.2 0.2 5.2 10.2 15.2 25 99 100.4 DATEMAX 20 100.3 MAX 15 10 5 0 -10 -15.4 -10.4 -5.4 0.4 5.4 10.4 15.4 100 99.8 99.6 99.4 -10.3 -5.3 0.3 5.3 10.3 15.3 100.4 18 MAX 100.3 100.2 100.1 12 10 99.9 8 99.8 6 99.6 100.2 DATEMAX 14 99.7 100.4 20 100.1 -20 100.6 22 16 -15 100.8 DATEMAX MAX -15.3 100.2 100 -5 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 100 99.9 4 99.8 2 0 99.7 -15.5 -10.5 -5.5 0.5 5.5 10.5 15.5 Figure 13A to 13D. Stock performances around their addition into the CAC40 index using opening prices. NB: X-axis : buying date, left y-axis: sale date, right y-axis: performance The analysis of performances over the first minutes of quotations does not show that a single purchase/sale strategy dominates others (see figures 13A and 13B). Conversely, figures 14A to 14F, corresponding to the last minutes of transactions (starting from interval 40), makes it possible to highlight the fact that an optimal strategy consists in buying the security entering into the index as soon as possible and selling it the day before the entry, or the day of the entry. Beyond this date, the figures show clearly that any strategy of purchase-sale will get only weak profits if not losses. 15 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 -6 100.4 100.3 100.2 100.1 100 99.9 99.8 DATEMAX MAX 99.7 99.6 -15_38 -10_38 -5_38 0_38 5_38 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 10_38 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 -6 -8 -10 -12 15_38 -15_39 100.8 DATEMAX MAX 100.6 100.4 100.5 DATEMAX MAX 100.4 100.3 100.2 100.1 100 99.9 99.8 99.7 99.6 -10_39 -5_39 0_39 5_39 10_39 15_39 22 102 20 101.5 18 16 DATEMAX 14 100.2 12 100 10 100.5 8 99.8 99.6 99.4 -15_40 -10_40 -5_40 0_40 5_40 10_40 15_40 22 18 100.6 16 100.4 14 100.2 12 10 100 8 99.8 6 4 99.6 2 0 99.4 -15_42 -10_42 -5_42 0_42 5_42 10_42 100 6 4 99.5 2 0 99 -15_41 100.8 DATEMAX MAX 20 15_42 101 MAX -10_41 -5_41 0_41 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 -15_43 5_41 10_41 15_41 101 DATEMAX MAX 100.8 100.6 100.4 100.2 100 99.8 99.6 99.4 99.2 -10_43 -5_43 0_43 5_43 10_43 15_43 Figure 14A to 14F. Stock performances around their addition into the CAC 40 index using closing prices. NB: X-axis : buying date, left y-axis: sale date, right y-axis: performance As another example, figure 15 gives stock performances around their addition into the CAC 40 when we suppose that the representative investor intervene only in the midday. The result is not very different from the one obtained with opening or closing prices even if the “stair” profile is attenuated: even if it is possible to carry out significant performances well beyond the entry, the investor is almost sure to carry out losses if he chooses to buy the stocks between the date of admission into the index and six days afterwards. 16 DATEMAX MAX 101.5 101 100.5 100 performance sale date 102 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 99.5 99 98.5 -15.7 -12.11 -9.15 -6.19 -3.23 0.27 3.31 6.35 buying date 10.7 13.11 16.15 19.19 Figures 15. Stock performances around their addition into the CAC 40 index using midday prices. From the viewpoint of the securities deleted from the CAC 40 index, the analysis of performances "by range" makes it possible to obtain relatively strong conclusions. The first ranges do not seem truly profitable if a purchase/sale strategy is based on them (see figure 16). 20.6 100 99.5 buying date 20.2 99 20 98.5 19.8 98 19.6 97.5 19.4 97 19.2 96.5 19 -15_2 performance 20.4 100.5 MINDATE MIN 96 -11_2 -7_2 -3_2 1_2 5_2 sale date 9_2 13_2 17_2 Figure 16. Stock performances around their deletion from the CAC 40 index using ranges 1 to 6. Note however that if we have a close look at performances over last minutes of quotations, we observe a very marked and symmetrical dynamic with the cases of addition into the index. Thus, a strategy consisting to maximize investor’s gains is to sell as soon as possible securities which will be deleted from the index and to repurchase them between -2 days and the day of the event. Such a strategy is very marked starting from the fortieth range as the figures 17 testify (intervals 40 to 44). 17 25 20 100.3 MINDATE MIN 20 100.2 19.5 15 100.1 19 10 100 5 99.9 18 0 99.8 17.5 -5 99.7 17 -10 99.6 16.5 99.5 16 -15 -15_39 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 -15_41 -10_39 -5_39 0_39 5_39 10_39 -15_40 100.5 100 99.5 99 98.5 98 97.5 97 96.5 -10_41 -5_41 0_41 5_41 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 -6 -15_43 10_41 15_41 100 99.5 18.5 15_39 MINDATE MIN 100.5 MINDATE MIN 99 98.5 98 97.5 -10_40 22 20 18 16 14 12 10 8 6 4 2 0 -2 -4 -15_42 -5_40 0_40 5_40 10_40 15_40 100.6 100.4 MINDATE MIN 100.2 100 99.8 99.6 99.4 99.2 99 98.8 98.6 98.4 -10_42 -5_42 0_42 5_42 10_42 15_42 101 MINDATE MIN 100.5 100 99.5 99 98.5 98 97.5 97 -10_43 -5_43 0_43 5_43 10_43 15_43 96.5 Figures 17A to 17E. Stock performances around their deletion from the index using closing prices NB: X-axis : sale date, left y-axis: buying date, right y-axis: performance In addition, a strategy consisting to intervene either at the opening or at the closing leads to the same profile of performances (see figure 18). Figure 18. Stock performances around their deletion from the CAC 40 index using ranges 1 to 6 and 40 to 43. Contrary to the index additions, for the deletions the «stair» does not arise over the period excluding the first and last minutes of transactions of the day (see figure 19). 18 Figure 19. Stock performances around deletion from the CAC 40 index using ranges 7 to 39. Conclusion In terms of purchase-sale strategies, strong results come out from our study since we obtain similar conclusions on the one hand for indices MSCI USD, MSCI Europe and for the CAC40 index and on the other hand for the entries and the exits of the indices. Our study shows that in all the cases it is necessary to buy (resp. to sell) as soon as possible and to sell (resp. to buy) the day before the event or the very same day. In addition, the interventions must preferably take place during the last minutes of transactions. Beyond the date of the event, such a strategy of purchase-sale is not remunerative. References Amihud Y. and H. Mendelson (1986), “Asset pricing and the bid-ask spread”, Journal of Financial Economics, 17, 223-249. Bancel F. and C. Vai (1994), “Impact sur les prix et les volumes des titres introduits ou sortant du panier de l’indice CAC40”, Analyse Financière, n°101, 78-88. Brown S. and J. Warner (1980), "Measuring Security Price Performance", Journal of Financial Economics, 8, 205-258. Brown S. and J. Warner (1985), "Using Daily Stock Returns: The Case of Event Studies", Journal of Financial Economics, 14, 3-31. Campbell J., A. Lo and A. MacKinlay (1997), The Econometrics of Financial Markets, Princeton University Press, New Jersey. Chung R. and L. Kryzanowski (1996), “ Trade activity and volatility changes around TSE300 index revisions”. Actes du colloque “Organisation et qualité des marchés boursiers”, 19-20 Décembre. Cochran W.G. and G.M. Cox (1950), Experimental Designs, New-York: John Wiley & Sons, Inc. Colas F.X. (2001), “ Impact des rebalancements de l’indice MSCI Europe sur les rendements et les volumes”, stage report, SINOPIA Asset Management. 19 Dhillon U. and H. Johnson (1991), “Changes in the Standard and Poor’s list”, Journal of Business 64, 75-85. Harris L. and E. Gurel (1986), “Price and volume effects associated with changes in the S&P 500 list : new evidence for the existence of price pressures”, Journal of Finance, 41, 815-829. Hasbrouck J. (1991), “Measuring the information content of stock trades”, Journal of Finance 46, 179-208. Jain P. (1987), “The effect on stock price of inclusion or exclusion from the S&P 500”, Financial Analysts Journal 43, 58-65. Satterthwaite F.W. (1946), "An Approximate Distribution of Estimates of Variance Components", Biometrics Bulletin, 2, 110-114 Thomas S. (1995), “Appartenance à un indice boursier : impact sur les rentabilités des titres concernés”. Document de travail, ParisBourse SA. 20 Appendix 105-110 100-105 95-100 90-95 85-90 80-85 -29 Performance -23 -17 -11 -5 1 7 Buy ing 13 19 25 Sale Stock performances around addition into the MSCI Europe index (all dates) 105-110 100-105 95-100 90-95 85-90 Performance -29 -25 -21 Buy ing -17 -13 -9 Sale Stock performances during addition into the MSCI Europe index (purchasing between –6 and –29 days and sale at all dates) 21 100-105 95-100 90-95 85-90 80-85 Performance 27 20 13 6 -1 Sale -8 -15 -22 -29 Buy ing Stock performances during deletion from the MSCI Europe index (all dates) 98-100 96-98 94-96 92-94 90-92 88-90 Performance 86-88 84-86 -9 -13 -17 Sale -21 -25 -29 Buying Stock performances during deletion from the MSCI Europe index (sale between –6 and –29 days and repurchasing at all dates) 22