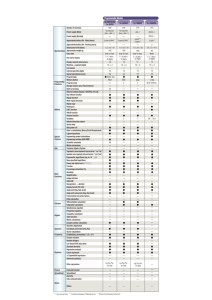

Market risk is the potential economic loss that may result - Snap-on

advertisement