Calculating Discounted Cash Flow

advertisement

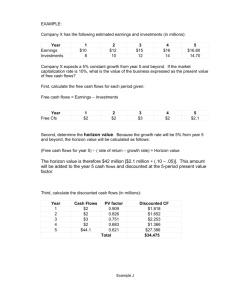

http://pages.stern.nyu.edu/~adamodar/New_Home_Page/lectures/basics.html DISCOUNTED CASHFLOW MODELS: WHAT THEY ARE AND HOW TO CHOOSE THE RIGHT ONE.. THE FUNDAMENTAL CHOICES FOR DCF VALUATION Cashflows to Discount o Dividends o Free Cash Flows to Equity o Free Cash Flows to Firm Expected Growth o Stable Growth o Two Stages of Growth: High Growth -> Stable Growth o Three Stages of Growth: High Growth -> Transition Period -> Stable Growth Discount Rate o Cost of Equity o Cost of Capital Base Year Numbers o Current Earnings / Cash Flows o Normalized Earnings / Cash Flows WHICH CASH FLOW TO DISCOUNT... The Discount Rate should be consistent with the cash flow being discounted o Cash Flow to Equity -> Cost of Equity o Cash Flow to Firm -> Cost of Capital Should you discount Cash Flow to Equity or Cash Flow to Firm? o Use Equity Valuation (a) for firms which have stable leverage, whether high or not, and (b) if equity (stock) is being valued o Use Firm Valuation (a) for firms which have high leverage, and expect to lower the leverage over time, because debt payments do not have to be factored in the discount rate (cost of capital) does not change dramatically over time. (b) for firms for which you have partial information on leverage (eg: interest expenses are missing..) (c) in all other cases, where you are more interested in valuing the firm than the equity. (Value Consulting?) Given that you discount cash flow to equity, should you discount dividends or Free Cash Flow to Equity? o Use the Dividend Discount Model (a) For firms which pay dividends (and repurchase stock) which are close to the Free Cash Flow to Equity (over a extended period) (b)For firms where FCFE are difficult to estimate (Example: Banks and Financial Service companies) o Use the FCFE Model (a) For firms which pay dividends which are significantly higher or lower than the Free Cash Flow to Equity. (What is significant? ... As a rule of thumb, if dividends are less than 75% of FCFE or dividends are greater than FCFE) (b) For firms where dividends are not available (Example: Private Companies, IPOs) WHAT IS THE RIGHT GROWTH PATTERN... The Choices THE PRESENT VALUE FORMULAE For Stable Firm: For two stage growth: For three stage growth: Definitions of Terms V0= Value of Equity (if cash flows to equity are discounted) or Firm (if cash flows to firm are discounted) CFt = Cash Flow in period t; Dividends or FCFE if valuing equity or FCFF if valuing firm. r = Cost of Equity (if discounting Dividends or FCFE) or Cost of Capital (if discounting FCFF) g = Expected growth rate in Cash Flow being discounted ga= Expected growth in Cash Flow being discounted in first stage of three stage growth model gn= Expected growth in Cash Flow being discounted in stable period n = Length of the high growth period in two-stage model n1 = Length of the first high growth period in three-stage model n2 - n1 = Transition period in three-stage model WHICH MODEL SHOULD I USE? Use the growth model only if cash flows are positive Use the stable growth model, if o the firm is growing at a rate which is below or close (within 1-2% ) to the growth rate of the economy Use the two-stage growth model if o the firm is growing at a moderate rate (... within 8% of the stable growth rate) Use the three-stage growth model if o the firm is growing at a high rate (... more than 8% higher than the stable growth rate) SUMMARIZING THE MODEL CHOICES Stable Growth Model Dividend Discount Model Growth rate in firmís earnings is stable. (g of firmeconomy+1%) Dividends are FCFE Model Growth rate in firmís earnings is stable. (gfirmeconomy+1% ) FCFF Model Growth rate in firmís earnings is stable. (gfirmeconomy+1% ) close to FCFE (or) FCFE is difficult to compute. Leverage is stable Two-Stage Model Three-Stage Model Growth rate in firmís earnings is moderate. Dividends are close to FCFE (or) FCFE is difficult to compute. Leverage is stable Growth rate in firmís earnings is high. Dividends are close to FCFE (or) FCFE is difficult to compute. Leverage is stable Dividends are very different from FCFE (or) Dividends not available (Private firm) Leverage is stable Growth rate in firmís earnings is moderate. Dividends are very different from FCFE (or) Dividends not available (Private firm) Leverage is stable Growth rate in firmís earnings is high. Dividends are very different from FCFE (or) Dividends not available (Private firm) Leverage is stable Leverage is high and expected to change over time (unstable). Growth rate in firmís earnings is moderate. Leverage is high and expected to change over time (unstable). Growth rate in firmís earnings is high. Leverage is high and expected to change over time (unstable). GROWTH AND FIRM CHARACTERISTICS Dividend Discount FCFE Discount Model FCFF Discount Model Model Pay no or low Have high Have high dividends capital capital High growth firms Earn high expenditures expenditures generally returns on relative to relative to projects depreciation. depreciation. (ROA) Earn high Earn high Have low leverage (D/E) Have high risk (high betas) Stable growth firms generally Pay large dividends relative to earnings (high payout) Earn moderate returns on projects (ROA is closer to market or industry average) Have higher leverage Have average risk (betas are closer to one.) returns on projects Have low leverage Have high risk narrow the difference between cap ex and depreciation. (Sometimes they offset each other) Earn moderate returns on projects (ROA is closer to market or industry average) Have higher leverage Have average risk (betas are closer to one.) returns on projects Have low leverage Have high risk narrow the difference between cap ex and depreciation. (Sometimes they offset each other) Earn moderate returns on projects (ROA is closer to market or industry average) Have higher leverage Have average risk (betas are closer to one.) SHOULD I NORMALIZE EARNINGS? Why normalize earnings? o The firm may have had an exceptionally good or bad year (which is not expected to be sustainable) o The firm is in financial trouble, and its current earnings are below normal or negative. What types of firms can I normalize earnings for? o The firms used to be financially healthy, and the current problems are viewed as temporary. o The firm is a small upstart firm in an established industry, where the average firm is profitable. HOW DO I NORMALIZE EARNINGS? If the firm is in trouble because of a recession, and its size has not changed significantly over time, Use average earnings over an extended time period for the firm Normalized Earnings = Average Earnings from past period (5 or 10 years) If the firm is in trouble because of a recession, and its size has changed significantly over time, Use average Return on Equity over an extended time period for the firm Normalized Earnings = Current Book Value of Equity * Average Return on Equity (Firm) If the firm is in trouble because of firm-specific factors, and the rest of the industry is healthy, Use average Return on Equity for comparable firms Normalized Earnings = Current Book Value of Equity * Average Return on Equity (Comparables) Source unknown: Calculating Discounted Cash Flow The three key questions in company valuation can all be answered using discounted cash flow methods. Take a Closer Look New Tech's Valuation Process. The discounted cash flow valuation used by New Tech was conducted by its financial advisor. Value: How much is a company worth today, based on what it will earn in the future? The company's predicted cash flows (or earnings) are discounted to give a present value. Rate of return: What is an investor's expected rate of return, given the amount invested and the company's financial projections? Investors will calculate their rate of return by: discounting the cash flow and the value they will take out of the company; and comparing this amount to what they invested at the beginning. Equity share: How much equity will the investor receive for the investment? Dividing the investment by the value of the company will give the percentage of ownership shares the investor will get. But first you need to know the value. 1. How Much is This Company Worth Today? Let's say investors are considering an investment in your company and plan to take their money out in five years. To them, your company is worth today what it can earn during the five years, plus their share of the value of the company at the end of the five years. This is like saying, the value of a five-year 10% Canada savings bond is the interest it will earn each year plus the principal amount paid back at the end of the term. The interest is equivalent to cash flows, and the principal is equivalent to the value of the company at the end of the year. The big difference is that the cash flows and the value at the end of the term are known for certain with a savings bond, but for investments in active businesses, these are unknowns. The discounted cash flow method applies adjustments or "discounts" to account for those unknowns. Using this method, the value is the total of the cash flows, adjusted or discounted, plus the value remaining (or residual value), also discounted. discounted cash flow value = discounted cash flows + discounted residual value A Simplified Example A company is projected to have fluctuating cash flows (e.g. losses of $200,000 in the first two years, a gain of $300,000 in the third, etc.) that total $1 million over five years. How much is it worth today? a) Discount the cash flows. The cash flows are discounted at a rate acceptable to the investor - say 20% (see chart). This leaves a present value of $0.4 million. In other words, the calculation indicates that getting $1 million in five years is the same as having $0.4 million today, using a discount rate of 20%. (This rate is used to calculate a discount factor for each year; the first year's cash flows are only discounted for one year, by about 80%; but the fifth year's cash flow must be discounted for five years, so it's discounted by much more, about 40%.) Year 1 Year 2 Year 3 Year 4 Year 5 Projected cash flows (000s) -$100 -$100 $300 $400 $500 $1,000 Discounted cash flows (@ 20%) -$83 -$69 $174 $192 $200 $414 Total b) Find the residual value of the company and discount it. The company's value at the end of the five years is calculated as being $10 million. This "residual value" is then adjusted by a discount factor (based on the 20% rate the investor finds acceptable), leaving a value of $4 million. You can think of the "residual" as an estimate of how much someone would pay to buy the whole company at the end of the investment period. c) Add the discounted cash flow and the discounted residual value. The cash flow value and the residual value are then added together. The estimated value of the firm using the discounted cash flow model is $0.4 million + $4 million or $4.4 million. Projected Cash flows $1 million Residual value $10 million Discounted cash flow value Discounted to Notes: present value $0.4 million Discounted at 20% over five years. $4.0 million Capitalized and discounted based on 20% discount rate over five years. $4.4 million Estimated fair market value today. This example is very simplified. For a more detailed explanation, see Calculating New Tech's Discounted Cash Flow Value, based on our case example company. Further discussion can be found in the Valuation Methods tool. 2. Investors' Rate of Return Investors want to calculate their rate of return. To do that they must compare the amount of the investment to the amount they will earn at the end of the investment period. But how can they know what they will earn in the future? Again, they must use the discounted cash flow projections to estimate the future value of their investment. A Simplified Example If investors had invested $500,000 and received 35% of the company's shares, how much will their return be at the end of the investment? a) Take estimated cash flow for the final year. The cash flow in the final year is used as a basis to decide the value of the company. Imagine that the company is projecting earnings of $500,000 in the final year. b) Estimate the value or sale price of the company based on the cash flow. How much will someone pay for this company in five years? Perhaps companies will be selling for 5 times or 10 times their earnings. Investors must decide what they think the market will be like and choose a multiple to multiply the cash flow by to convert it to a value for the company. Let's say the investors choose 8 times earnings. Then the value of the company when the investors will exit should be 8 times $500,000 or $4 million. c) The value of the investors' share is calculated. If the investors have purchased 35% of the shares of the company, they can expect to take away $1.4 million when the business is sold. d) The investors determine their rate of return. The investors' original investment of $500,000 is then compared to the return of $1.4 million. The return is the equivalent of a return of 23% compound interest for five years (see the table below). Projected final year's cash flow $500,000 Multiplied by 8 to find estimated selling price of the company $4 million Divided by 35% to represent the investor's share $1.4 million Calculated as a rate of return on original investment of $500,000 (compounding the interest) 23% 3. How Much of the Company do the Investors Get? The valuation information you get from discounted cash flow also allows you to consider the percentage of shares the investors receive in return for their investment. In the example above, the investors' share was assumed to be 35%. At that proportion, and given a value of $4 million at the end of the investment period, the investors would make $1.4 million, or 23% on the initial $500,000 investment. If the investors feel that isn't an adequate return, then one way to increase the return is to give them a greater equity share for the same investment. So, for example, if their $500,000 investment bought them 45% of the company, instead of 35%, they would get 45% percent of the $4 million exit value — or $1.8 million. And that is equivalent to a 29% return on their investment. Investors' share 35% share 45% share Exit value of company $4 million $4 million Divided by investors % share $1.4 million $1.8 million 23% 29% Calculated as a rate of return on original investment of $500,000 (compounding the interest) Value, Return and Exit Strategy The way the values and rates of return are calculated depend on the specific exit strategy used. In the next section, the implications of different exit strategies on exit values are discussed.