2007 Exam - City University of Hong Kong

CITY UNIVERSITY OF HONG KONG

Course code & title :

Session :

Time allowed :

MS6217: Statistical Modelling in Finance

Semester B,

3 hours

This paper has 10 pages (including this page)

2006-2007

1.

2.

3.

Instructions to candidates:

Answer ALL FOUR questions

Show sufficient work for each question

This question paper is NOT to be taken away

Materials, aids and instruments permitted during examination:

Approved calculator

1

Question 1 (25 marks)

Equity Linked Investment (ELI) is now a popular investment product in Hong Kong. Suppose an

ELI is linked to the shares of Hutchison-Whampoa, one of the constituent stocks of the Hang

Seng Index. On the day of deposit, the spot price of Hutchison-Whampoa is $70 per share. The bank offers a strike price equal to 97% of the spot price. The deposit interest rate is 15.5% p.a., and the deposit term is 33 days. By investing in the ELI, the investor agrees to purchase shares of

Hutchison-Whampoa at the strike price with the principal and interest if the closing price of the stock is lower than the strike price on the date of maturity. Conversely, if the closing price is higher than strike price at maturity then the investor will receive the interest on the deposit. a) Compare the ELI with a stock option. Is the ELI equivalent to a call option or a put option?

Who is the buyer of the option and who is the writer? (3 marks) b) What is the strike price of the above ELI? (2 marks) c) Assuming that interest is compounded daily, work out the interest received for this investment as a percentage of the principal. (4 marks) d) If the deposit amount has to be no less than HK$100,000, what is the minimum amount required for this investment such that the number of shares settled at maturity (assuming that closing price < strike price) is a multiple of 100? (4 marks) e) Work out the profit/loss (in HK$) of this ELI if the closing price of Hutchison-Whampoa on the day of maturity is i) $75, ii) $71 and iii) $66 per share. (3 marks) f) At what closing price of the stock will this investment break even? (3 marks) g) How will the length of the ELI period affect the interest on the deposit? (2 marks) h) How will an increase in the strike price affect the interest on the deposit? (2 marks) i) From the viewpoint of an investor, do you consider the ELI a “bullish” or “bearish” strategy?

Carefully explain your answer. (2 marks)

2

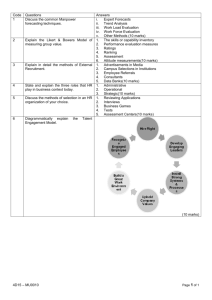

Question 2 (25 marks) a) Your financial advisor has suggested to you a protective put strategy on your investment: buy shares in a market stock fund and purchase put options on those shares with three month maturity and exercise price of $1040. The stock fund is currently at $1200. However, your professor at university has suggested instead that you buy a three-month call option on the index fund with exercise price of $1120 and buy three-month T-bills with face value of $1120. i) In a table and on a graph, illustrate the payoffs to each of these strategies as a function of the stock fund value in three months. (7 marks) ii) Which portfolio would you think must require a greater initial outlay to establish?

(3 marks) iii) Suppose the market prices of the securities are as follows:

Stock fund $1200

T-bill (face value $1120)

Call (exercise price $1120)

Put (exercise price $1040)

$1080

$160

$8

Make a table of profits realized for each portfolio for the following values of the stock price in 3 months: S

T

= 0, 1040, 1120, 1200 and 1280. Graph the profits to each portfolio as a function of S

T

on a single graph. iv) Which strategy is riskier?

(7 marks)

(2 marks) b) i) Use the Black-Scholes formula ( C

S e

T

(

d

1

)

Xe

rT

(

d

2

) ), where d

1

ln( S o

/ X ) ( r

T

2

/ 2) T

and d

2

1

European style call option on the following stock:

T to find the value of a

Stock price ( S o

= 100);

Annual interest rate (r = 0.10);

Time to expiry (T = 3 months);

Exercise price (X = 95);

Dividend yield ( = 0);

Standard deviation (

0.5

)

(4 marks) ii) Suppose that the standard deviation on the stock increases. Will the option be worth more or less with the higher volatility? Carefully explain your answer. (2 marks)

3

Question 3 (25 marks)

The earnings per share of a listed company in the NYSE from January 1987 to December 1998 are plotted in Figure 3.1(i). There are 144 observations, denoted by y

1

, y

2

, …, y

144

. Figure 3.1(ii) displays the plot of the values transformed by the natural logarithms: log e

(y

1

), log e

(y

2

),.. , log e

(y

144

).

Figure 3.1. Earnings per share of a listed company in the NYSE

3000

2500

2000

1500

1000

1

(i) Original values y t

14 28 42 56 70

Time

84 98 112 126 140

8.00

7.75

7.50

7.25

7.00

6.75

6.50

1 14 28 42 56 70

Time

84 98 112 126 140

(ii) Transformed values log e

(y t

)

(a) Discuss why the log transformation is needed and whether the objective is achieved.

(2 marks)

4

After taking first-order seasonal differencing, the investigator finds the series stationary. Figure 3.2 presents the SAS results of estimation and diagnostic checking for the series z t

, where z t y t

y t

12

and y t

e y t

.

(b) Find the missing values (1), (2), (3) and (4) in Figure 3.2, where (4) refers to the constant term δ . (5 marks)

(c) Give an expression of the fitted model of z t

in terms of the backshift notation.

(5 marks)

(d) Is the model adequate? Why or why not? with y t

alone on the left-hand side).

(3 marks)

(e) Express the model in terms of the original time series y t

for the purpose of forecasting (that is,

(5 marks)

(f) Obtain the forecast of y

145

using the values of the series log e

(y t

) given in Figure 3.3. (5 marks)

Figure 3.2. SAS output of estimation and diagnostic checking results

ARIMA Procedure

Maximum Likelihood Estimation

Standard Approx

Parameter Estimate Error t Value Pr > |t| Lag

MU (1) 0.01541 4.36 <.0001 0

AR1,1 0.60223 0.07215 8.35 <.0001 1

AR1,2 (2) 0.07335 3.30 0.0010 3

AR2,1 (3) 0.08716 -3.23 0.0013 12

Constant Estimate (4)

Variance Estimate 0.001369

Std Error Estimate 0.037003

AIC -489.893

SBC -478.362

Number of Residuals 132

Autocorrelation Check of Residuals

To Chi- Pr >

Lag Square DF ChiSq --------------------Autocorrelations--------------------

6 3.03 3 0.3865 0.028 -0.023 0.012 -0.133 -0.016 0.051

12 5.69 9 0.7700 0.008 0.020 0.105 0.034 0.069 -0.030

18 13.00 15 0.6026 -0.165 -0.097 -0.038 0.023 0.076 -0.064

24 20.11 21 0.5143 -0.007 0.059 0.076 -0.013 0.133 -0.129

5

Autocorrelation Plot of Residuals

Lag Covariance Correlation -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1 Std Error

0 0.0013692 1.00000 | |********************| 0

1 0.00003871 0.02827 | . |* . | 0.087039

2 -0.0000321 -.02346 | . | . | 0.087108

3 0.00001663 0.01215 | . | . | 0.087156

4 -0.0001816 -.13261 | ***| . | 0.087169

5 -0.0000213 -.01556 | . | . | 0.088684

6 0.00006996 0.05110 | . |* . | 0.088705

7 0.00001100 0.00804 | . | . | 0.088928

8 0.00002677 0.01955 | . | . | 0.088933

9 0.00014432 0.10540 | . |** . | 0.088966

10 0.00004696 0.03430 | . |* . | 0.089907

11 0.00009423 0.06882 | . |* . | 0.090006

12 -0.0000417 -.03049 | . *| . | 0.090404

13 -0.0002264 -.16535 | .***| . | 0.090482

14 -0.0001328 -.09701 | . **| . | 0.092742

15 -0.0000526 -.03840 | . *| . | 0.093508

16 0.00003132 0.02288 | . | . | 0.093627

17 0.00010376 0.07578 | . |** . | 0.093670

18 -0.0000880 -.06425 | . *| . | 0.094133

19 -9.2396E-6 -.00675 | . | . | 0.094465

20 0.00008133 0.05940 | . |* . | 0.094468

21 0.00010345 0.07556 | . |** . | 0.094751

"." marks two standard errors

Partial Autocorrelations

Lag Correlation -1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

1 0.02827 | . |* . |

2 -0.02428 | . | . |

3 0.01353 | . | . |

4 -0.13414 | ***| . |

5 -0.00704 | . | . |

6 0.04561 | . |* . |

7 0.00864 | . | . |

8 0.00409 | . | . |

9 0.10269 | . |**. |

10 0.04244 | . |* . |

11 0.07679 | . |**. |

12 -0.03557 | . *| . |

13 -0.14018 | ***| . |

14 -0.08907 | .**| . |

15 -0.03542 | . *| . |

16 0.01154 | . | . |

17 0.03157 | . |* . |

18 -0.10176 | .**| . |

19 -0.00409 | . | . |

20 0.06372 | . |* . |

21 0.11210 | . |**. |

22 -0.00234 | . | . |

23 0.17374 | . |*** |

24 -0.09389 | .**| . |

6

Figure 3.3. Values of series log e

(y t

) for previous periods

t log e

(y t

)

115 7.53102

116 7.61530

117 7.39572

118 7.30519

119 7.40914

120 7.91899

121 7.23850

122 7.23562

123 7.42833

124 7.49165

125 7.52833

126 7.62657

127 7.56216

128 7.62462

129 7.42118

130 7.37526

131 7.46049

132 8.00303

133 7.28482

134 7.30317

135 7.52186

136 7.55956

137 7.62217

138 7.71021

139 7.64060

140 7.66996

141 7.48381

142 7.42536

143 7.47534

144 7.99934

7

Question 4 (25 marks) a) The relationship between a dependent variable Y t the following transfer function-noise model:

Y t

2 Y t

1

Y t

2

( X t

1

and an independent variable

2 X t

2

X t

3

)

0.2

t

1

X t

is given by

0.1

t

2 where t i i d

2

)

(4.1) i) Explain the relationship between Y t

and X t

using (4.1) (4 marks) ii) Obtain the impulse response weights of the transfer function for lags 0 - 3. (8 marks) iii) Graphically depict the behaviour of the impulse response function. (2 marks) b) A stock analyst believes that the closing price of the HSBC holdings in New York on a given day is useful in predicting the stock’s opening price in Hong Kong on the following day. To verify this claim, she collects n = 300 observations of the stock’s daily closing prices in New

York and the opening prices in Hong Kong. A pure random walk without drift model has been found to be the best ARIMA model for the New York prices. The analyst then fits a transfer function model based on the estimated cross-correlations between the pre-whitened

New York closing prices (

t

) and the Hong Kong opening prices (

t

) as shown in Table 4.1.

The residuals’ ACF and PACF are given in Table 4.2. i) Write down the appropriate equations corresponding to the pre-whitened input and output series. (3 marks) ii) Do you agree that the closing price of the HSBC holdings in New York on a given day is a useful leading indicator of the stock’s opening price in Hong Kong on the following day?

Carefully explain your answer. (4 marks) iii) Specify a transfer function-noise model based on the results from Tables 4.1 and 4.2.

(3 marks) iv) In practice, what other statistical diagnostics are necessary to confirm the theoretical validity of the model? (1 mark)

8

Table 4.1: Cross Correlations

r

( )

between t

and k Cross Correlatons

-11 0.0155

-10 -0.0231

-9 -0.0903

-8 0.0243

-7 0.0001

-6 0.0021

-5 -0.0534

-4 -0.0321

-3 -0.0943

-2 -0.0932

-1 -0.1000

0 0.1001

Note:

( )

1/ n k Cross Correlations

1 0.1966

2 -0.0435

3 -0.0053

4 0.0021

5 0.0013

6 0.0231

7 -0.0521

8 -0.0087

9 -0.0043

10 -0.0011

11 -0.0000

Table 4.2: ACF and PACF for the residuals k ACF

1 0.0873

2 0.0621

3 0.1001

4 -0.0201

5 -0.0213

6 0.0089

7 0.0004 k PACF

1 0.0873

2 -0.0091

3 0.0082

4 0.0172

5 0.0534

6 0.0001

7 0.0423

8 0.0114

9 -0.0632

Note:

( )

( )

1/

8 0.0231

9 0.0004 n

9

10