2005 Exam - City University of Hong Kong

advertisement

CITY UNIVERSITY OF HONG KONG

Course code & title

:

MS6217

Statistical Modelling in Finance

Session

:

Semester B,

2004-2005

Time allowed

:

3 hours

This paper has 13 pages (including this page)

Instructions to candidates:

1.

2.

Answer ALL FOUR questions

Show sufficient work for each question

Materials, aids and instruments permitted during examination:

Approved calculator

1

Question 1 (25 marks)

Consider the following transfer function model,

Yt v( B) X t N t

(1.1)

where v( B) vo v1 B v 2 B 2 ....... , and B is the backward shift operator.

a)

An equivalent way of representing (1.1) is

Yt w( B) X t b / ( B) q ( B) Q ( B L )at / p ( B) P ( B L )

.

(1.2)

Explain the purposes of w(B), (B) and b in (1.2). Explain also why (1.2) is an

equivalent way of representing (1.1).

(5 marks)

b)

To examine the relationship between the monthly forward rates and spot rates of

the Australian dollar from May 1991 to April 1997, a transfer function model is

specified with { f t }, the first difference of the 90-day forward rate measured as

U.S. cents per Australian dollar, as the input series; and {st }, the first difference

of the spot rate, as the output series. Both { f t } and {st } are stationary.

i)

Describe step by step how you would “prewhiten” { f t } and {st } in the

transfer function model. Are the prewhitened series necessarily white

noise?

(5 marks)

ii)

Suppose that the sample cross-correlations between the prewhitened

{ f t } and prewhitened {st } are given by,

r fs (5) 0.001 ;

rfs(-4) = -0.102;

rfs(-3) = 0.004;

rfs(-2) = 0.000;

rfs(-1) = 0.024;

rfs(0) = -0.113;

r fs (1) 0.012 ;

rfs(2) = 0.130;

rfs(3) = 0.516;

rfs(4) = 0.202;

rfs(5) = 0.193;

rfs(6) = 0.101;

The standard deviation of r fs (i ) and rsf (i ) is approximately (n i) 1 / 2 ,

where n is the number of observations in the sample.

Discuss how you would identify a tentative transfer function model on the

basis of the above results.

(5 marks)

2

iii)

Suppose that the model identified in ii) is estimated and the Ljung-BoxPierce test for the significance of the residuals are:

Q * (6) 31.2

Q (12) 39.5

*

Q * (18) 42.4

with p-value = 0.0

with p-value = 0.0

with p-value = 0.0

So what do you conclude? Discuss how you would proceed to specify a

final transfer function model.

(3 marks)

iv)

In practice, what other diagnostic tests are necessary to examine the

validity of the model?

(5 marks)

v)

Discuss how you would test if there exists significant arbitraging

opportunities in the Australian foreign exchange market using the

estimated transfer function model.

(2 marks)

3

Question 2 (15 marks)

a)

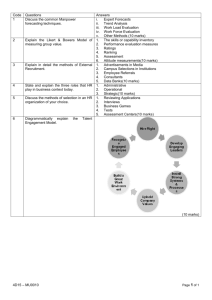

Briefly discuss the motivation behind log transformation of seasonal time series.

Figures 2a and b show, respectively, the earnings per share and log earnings per

share of a listed company in the NYSE from 1981Q1 to 2001Q4. Discuss if the

objectives of log transformations have been achieved.

(2 marks)

Fig.2a: Earnings per share

18

16

14

earnings

12

10

8

6

4

2

0

0

10

20

30

40

50

60

70

80

t

Fig 2b. Log earnings per share

3

2.5

2

log earnings

1.5

1

0.5

0

0

10

20

30

40

50

60

70

80

-0.5

-1

t

b)

Denote the log earnings by xt . Upon examining the ACF’s and PACF’s of xt

and its first regular and seasonal differences, the investigator estimates the

models:

i)

(1 B 4 )(1 B) xt (1 B)at ;

4

ii) (1 B 4 )(1 B) xt (1 B)(1 B 4 )at ;

where at ~ i.i.d .(0, 2 ) . Give expressions of these models in terms of the

notation ARIMA(p,d,q)(P,D,Q)L.

(2 marks)

c)

Show that for model ii), the autocorrelation coefficient of the differenced series at

lag 3 is given by 3 / (1 2 )(1 2 ) , while for model i), 3 0.

(3 marks)

d)

Results on the estimation of the two models are given as follows. Compare the

performance of the models using the in-sample diagnostics.

(5 marks)

Estimation Results of Model i)

Maximum Likelihood Estimation

Parameter

Estimate

Standard

Error

Approx

t Value

Pr > |t|

Lag

MA1,1

0.76654

0.07655

10.01

<.0001

1

Variance Estimate

Std Error Estimate

AIC

SBC

Number of Residuals

0.008836

0.093999

-147.514

-145.145

79

Autocorrelation Check of Residuals

To

Lag

6

12

18

24

ChiSquare

10.80

19.14

22.02

24.79

DF

Pr >

ChiSq

--------------------Autocorrelations--------------------

5

11

17

23

0.0555

0.0587

0.1838

0.3614

0.169 0.148 -0.119 -0.251 -0.031 -0.014

0.254 0.050 -0.030 0.018 -0.135 0.076

-0.075 0.095 -0.060 -0.065 -0.001 -0.080

0.081 -0.008 0.050 -0.028 -0.119 -0.023

Estimation Results of Model ii)

Maximum Likelihood Estimation

Parameter

Estimate

Standard

Error

t Value

Approx

Pr > |t|

Lag

MA1,1

MA2,1

0.68089

0.31449

0.09049

0.11227

7.52

2.80

<.0001

0.0051

1

4

5

Variance Estimate

Std Error Estimate

AIC

SBC

Number of Residuals

0.008137

0.090203

-152.753

-148.014

79

Autocorrelation Check of Residuals

To

Lag

6

12

18

24

e)

ChiSquare

3.38

10.17

13.70

16.39

DF

Pr >

ChiSq

--------------------Autocorrelations--------------------

4

10

16

22

0.4960

0.4256

0.6212

0.7961

0.042 0.150 -0.114

0.187 0.070 -0.089

-0.105 0.114 -0.084

0.025 -0.008 0.070

0.007 -0.053

0.050 -0.121

-0.032 -0.000

0.004 -0.132

0.021

0.097

-0.057

0.027

Obtain forecast of earnings per share for period 85 (i.e., 2002Q1) using the

preferred model chosen in part d) and the following information:

Obs.

80

81

82

83

84

xt

2.3016

2.7850

2.6858

2.7738

2.4519

x̂t (predicted value of xt )

2.4816

2.7855

2.8240

2.7707

2.6465

xt xˆt

-0.18

-0.0005

-0.1382

0.0031

-0.1946

(3 marks)

6

Question 3 (37 marks)

a)

Your financial advisor has suggested to you a protective put strategy on your

investment: buy shares in a market stock fund and purchase put options on those

shares with three month maturity and exercise price of $1040. The stock fund is

currently at $1200. However, your professor at university has suggested instead

that you buy a three-month call option on the index fund with exercise price of

$1120 and buy three-month T-bills with face value of $1120.

i)

ii)

iii)

In a table and on a graph, illustrate the payoffs to each of these strategies as a

function of the stock fund value in three months.

(6 marks)

Which portfolio would you think must require a greater initial outlay to

establish?

(2 marks)

Suppose the market prices of the securities are as follows:

Stock fund

T-bill (face value $1120)

Call (exercise price $1120)

Put (exercise price $1040)

b)

$1200

$1080

$160

$8

iv)

Make a table of profits realized for each portfolio for the following values of

the stock price in 3 months:

ST = 0, 1040, 1120, 1200 and 1280. Graph

the profits to each portfolio as a function of ST on a single graph.

(9 marks)

Which strategy is riskier?

(2 marks)

i)

Use the Black-Scholes formula ( C So e T P( Z d1 ) Xe rT P ( Z d 2 ) ),

where d1

ln( So / X ) (r 2 / 2)T

T

and d2 d1 T to find the value

of a European style call option on the following stock:

Stock price ( S o = 100);

Annual interest rate (r = 0.10);

Time to expiry (T = 3 months);

ii)

c)

Exercise price (X = 95);

Dividend yield ( = 0);

Standard deviation ( 0.5 )

(4 marks)

Suppose that the standard deviation on the stock increases. Will the option be

worth more or less with the higher volatility?

(2 marks)

In order to better understand the dependence of a security on volatility, an

investigator estimates a GARCH(1,1) model for the monthly excess returns of the

S&P 500 index ( y t ) from January 1926 to December 1991. Results of estimation

using SAS are given as follows:

GARCH Estimates

7

SSE

MSE

Log Likelihood

SBC

Normality Test

2.70454693

0.00341

1269.46195

-2512.2257

95.0061

Observations

Uncond Var

Total R-Square

AIC

Pr > ChiSq

Variable

DF

Estimate

Standard

Error

Intercept

ARCH0

ARCH1

GARCH1

1

1

1

0.007453

0.0000818

0.1203

0.8545

0.001547

0.0000238

0.0197

0.0189

1

792

???

.

-2530.9239

<.0001

t Value

4.82

3.44

6.12

45.15

Approx

Pr > |t|

<.0001

0.0006

<.0001

<.0001

i)

Write down the estimated GARCH process. What assumptions on the

parameters are necessary in order for the process to be valid?

(5 marks)

ii)

Obtain the unconditional variance of the process.

iii)

What other diagnostic tests would you use to examine the adequacy of the

model?

(3 marks)

8

(4 marks)

Question 4 (23 marks)

To examine the international transmission of bond market movements, an investigator

considers 960 daily close-of-trade observations from April 1986 to December 1989 on

the yields of government bonds with less than five years to maturity for the bond markets

of the U.K. and U.S.

a)

Using the Augmented Dickey Fuller (ADF) test in conjunction with the Dolado’s

sequential testing procedure discussed in class, test for the unit root hypothesis for

each of the bond yield series at the 10% level of significance. Some of the

following information may be useful:

Test Statistic

U

U

UK

-1.14

-1.01

US

-1.21

-1.73

4.01

6.17

3.92

2.22

where is the test statistic for testing H o : 0 vs. H1 : 0 in models without

a linear trend;

U is the test statistic for testing H o : 0 vs. H1 : 0 in models with a linear

trend;

is the test statistic for testing H o : 0 vs. H1 : 0, 0 in models

without a linear trend;

U is the test statistic for testing H o : 0 vs. H1 : 0, 0 in models

with a linear trend; and

the regression used for testing is:

p

xt t xt 1

i xt i t

(8 marks)

i 1

b)

Discuss (without having to perform the testing) how the investigator could test if

the bond “returns” (as opposed to bond yields) are stationary?

(2 marks)

c)

Suppose that each of the bond yield series is I(1). The investigator then tests if

there is a long run relationship between the series using the bivariate

Cointegrating Regression Augmented Dickey Fuller (CRADF) test. The results

are summarized as follows:

CRADF

UK/US

US/UK

p = augmentation

level

0

0

-4.27

-3.98

9

Conduct the test at the 10% level of significance. What do you conclude?

(2 marks)

d)

The investigator then constructs and estimates the following Error Correction

model:

UKt 01 1 zt 1

USt 02 2 zt*1

q

m

i UKt i j USt j 1t

i 1

j 1

m*

q*

i*UKt i *j USt j 2t

i 1

i)

ii)

iii)

e)

(5.1)

(5.2)

j 1

What is the purpose of including the error correction terms in (5.1) and

(5.2)?

(2 marks)

What are the expected signs of the coefficients 1 and 2 ? Carefully

explain your answers.

(2 marks)

Suggest how the investigator could determine the appropriate number of

lagged terms in the Error Correction model.

(2 marks)

One interesting hypothesis to examine is whether movements in one bond market

have a tendency to “Granger cause” movements in the other. Discuss how the test

of Ganger causality may be conducted. Suppose the test statistic for testing

UKt USt is 9.563 and q q* m m* 6 . Conduct the test at the 5%

level of significance.

(3 marks)

f)

Given your answers to parts c) and e), discuss if USt is expected to “Granger

cause” UK t .

(2 marks)

10