Study Guide

advertisement

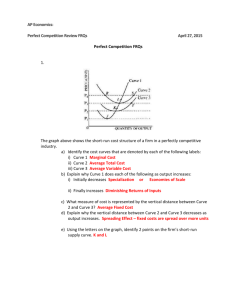

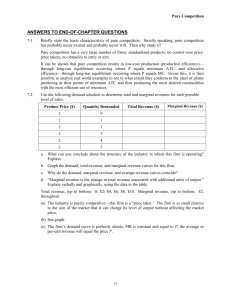

AP MICROECONOMICS-2015 Name: ________________________ Study Guide Unit #2: Chapter 13 +14 Mandatory for all students DUE: Block Period February 25th or 26th 1) The graph above displays 3 curves: Marginal Product. Total Product & Average Product of Labor (workers). a. Label the appropriate curves as: MP, TP and AP 2) Define Marginal Product: _______________________________ 3) Explain the reasons for the shape of the marginal product of labor curve (in terms of initially rising & then falling) _______________________________________________________________________________________________ _______________________________________________________________________________________________ 4) Whenever MP is increasing you are in the area of _____________________________ and therefore the marginal cost of a firm must be ________________________. 5) Label all 4 cost curves below: 6) Define Marginal Cost (MC) ______________________________________________________________________________________________________ 7) Explain why curve D starts very high on the Y axis and approaches the X axis but never touches it? ______________________________________________________________________________________________________ 8) At what point does curve A cross curve B and cross curve C? a. explain why this is true. ______________________________________________________________________________________________________ 9) Explain how the ATC (average total cost) is used to determine economic profit a. Write formula & provide example with numbers! ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ 10) List the five market characteristics of Perfect Competition: (also called a competitive market) a. Categories: # of firms, type of product, ease of entry/exit, information, price control ↓ ↓ ↓ ↓ ↓ ______________________________________________________________________________________________________ Entire Industry Individual Firm Price S1 ------------- $10 -------------- E1 Q1 Price $10 D1 D1 Q1 Qty T-Shirts Qty T-Shirts 11) Clearly explain why an individual firm in a competitive market has or “sees” a horizontal demand curve? a. What does this imply about the relationship of Price, Average Revenue & Marginal Revenue? ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ 12) Explain why an individual firm in a competitive market increases production until MR a. Hint: think of the profit on the very last unit produced using this formula! ≥ MC to maximize profit? ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ 13) The entire Market for Blue Jeans is in equilibrium at a price of $60. The cost curve table below is for an individual firm in a competitive market for Blue Jeans. (as is the demand curve table) Please fill in the following table and find the profit maximizing level of production for this individual competitive firm. a. Fixed costs are ________ What quantities display economies of scale: _____________ b. This firm should produce: _________ units. (in short run) c. The profit for this firm = ________________________ (P – ATC) * Qty d. Why should this firm still operate with an economic loss? ___________________________ e. Can this be a long run equilibrium? _______________________________________ |------------------- COST CURVES--------------------------------| |-------------------DEMAND CURVE------------| Quantity Produced Total Cost MC 0 1 2 3 4 5 6 100 150 202 257 317 385 465 -50 ATC AVC -- -- 85.66 79.25 51.00 52.33 54.25 77.5 60.83 Quantity Demanded Price 0 1 2 3 4 5 6 60 60 60 60 60 60 60 Total Revenue Marginal Revenue -60 -60 Marginal Cost Table: QTY= 30 40 50 60 MC = $8 $10 $12 $14 ATC = $8 $8.5 $10 $11 14) The graph above is for an individual firm in a competitive market. Based on the graph & Marginal Cost Table above at a market price of $10: (remember they are a price taker!) a. b. c. d. e. How many units would be produced: __________ Label graph: Add a marginal revenue curve and label actual Price, Quantity & E1 Draw in profit or loss box. What is the economic profit for this firm? __________ Is their Accounting profit above or below this? If market demand rose causing price to rise to $14 dollars (modify graph and label all points) i. How many units would be produced: ______________ ii. Calculate the economic profit of this firm (show calculations…) ============================================================================================= (a) Initial Condition Market Firm Price Price MC Short-run supply, S1 A P1 Long-run supply ATC P1 Demand, D1 0 Q1 Quantity (market) 0 Quantity (firm) 15) Based on the graphs above list 3 requirements for a competitive market to be in long run equilibrium - ________________________ ________________________ - ________________________ 16) Analyze the difference between the short run supply curve and the long run supply curve for an 1- INDIVIDUAL FIRM. a. Hint: think ATC & AVC Make sure you mention the terms SHUTDOWN & EXIT in your analysis ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ 17) Discuss the difference between the short run MARKET supply curve vs. long run MARKET supply curve for an entire industry. (left hand graph above…) a. Hint: Why is there a difference? ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ (a) Initial Condition Market Firm Price Price MC Short-run supply, S1 A Long-run supply P1 ATC P1 Demand, D1 0 Q1 Quantity (market) 0 Quantity (firm) 18) Modify the graphs above for the impact of a short run decrease in demand a. Find a new market equilibrium b. Label equilibrium point either E1 & E2 or A & B & Quantity , shade profit/loss box) c. Explain why this new equilibrium will not last in the long run in a competitive market d. Explain what would likely occur in the long run to secure a new long run equilibrium ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ ______________________________________________________________________________________________________ TOTAL SCORE Excellent Work ____ Very Good Work ____ Good Work ____ Poor Work ____ ________/30 PTS