CHAPTER 15

advertisement

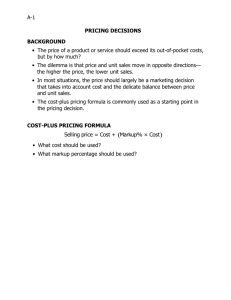

CHAPTER 15 Target Costing and Cost Analysis for Pricing Decisions EXERCISE 15-34 (25 MINUTES) (1) Cost-Plus Pricing Formula Variable manufacturing cost .................................................. $600 $1,200 = $600 + (100% $600)a Applied fixed manufacturing cost ......................................... 210 (2) Absorption manufacturing cost ............................................ $810 $1,200 = $810 + (48.15% $810)b Variable selling and administrative cost ............................... 90 Allocated fixed selling and administrative cost ............................................................... 150 (3) Total cost $1,050 $1,200 = $1,050 + (14.29% $1,050)c Variable manufacturing cost .................................................. $600 Variable selling and administrative cost ............................... 90 (4) Total variable cost .................................................................. $690 $1,200 = $690 + (73.91% $690)d Explanatory Notes: a($1,200 – $600) ÷ $600 = 100% b($1,200 – $810) ÷ $810 = 48.15% (rounded) c($1,200 – $1,050) ÷ $1,050 = 14.29% (rounded) d($1,200 – $690) ÷ $690 = 73.91% (rounded) EXERCISE 15-35 (30 MINUTES) Markup percentage applied to cost base in cost-plus pricing formula 1. Markup percentage profit required to achieve target ROI total annual costs not included in cost base = cost base per unit annual used in cost-plus volume pricing formula total variable selling and total annual $60,000 = administrative costs fixed costs 480 $400 $60,000 (480 $50) [480 ($250 $100)] = 480 $400 $60,000 $24,000 $168,000 = $192,000 + = 131.25% Thus, the Wave Darter’s price would be set equal to $925, where $925 = $400 + ($400 131.25%). EXERCISE 15-36 (15 MINUTES) 1. Material component of time and material pricing formula: material cost incurred on job 2. material handling material and storagecosts cost incurred annual cost of materials 1.05 used in Repair Department on job Material component of price, using formula developed in requirement (1): [$8,000 + ($8,000 .04)] 1.05 = $8,320 1.05 = $8,736 New price to be quoted on yacht refurbishment: Total price of job = time charges + material charges = $9,000* + $8,736** = $17,736 *From Exhibit 15-7. **From requirement (1). PROBLEM 15-39 (30 MINUTES) 1. (a) Time charges: annual overhead (excluding Hourly labor cost + material handling and storage) annual labor hours + hourly charge to cover profit magin = $25.00 + $220,000 + $5.00 20,000 = $41.00 per labor hour (b) Material charges: material cost material handling and storage costs incurred on job incurred on job annual cost of materials used Material cost = material cost $25,250 incurred on job incurred on job $252,500 Material cost 2. PRICE QUOTATION Time charges: Labor time .................................................................................................. 800 hours Rate ......................................................................................................... $ 41.00 per hour Total ............................................................................................................ $32,800 Material charges: Cost of materials for job ........................................................................... $150,000 + Charge for material handling and storage ............................................ 15,000* Total ............................................................................................................ $165,000 Total price of job: Time ............................................................................................................ $ 32,800 Material ....................................................................................................... 165,000 Total ............................................................................................................ $197,800 *Charge for material handling and storage): 10% = $25,250 ÷ $252,500; 10% $150,000 = $15,000 Price of job without markup on material costs (from requirement 2) .... $ 197,800 Markup on total material costs ($165,000 10%) ................................... Total price of job ........................................................................................ 16,500 $214,300 3. PROBLEM 15-42 (30 MINUTES) 1. Cost-plus pricing begins by computing an item’s cost and then adds an appropriate markup. The result is the item’s selling price. In contrast, target costing begins by determining an appropriate selling price. A target profit is next subtracted from that price to yield the cost (i.e., the “target cost”) that must be achieved. Target costing could be labeled price-led costing because it begins by determining a target selling price. In contrast, cost-plus pricing methods begin with the cost and culminate in determination of the selling price. 2. The current selling price is $6,750: Direct material……………………………....... Direct labor……………………………………. Manufacturing overhead…………………… Selling and administrative expenses……. Total cost…………………………………. Markup ($5,400 x 25%)……………………... Selling price………………………………...... 3. 4. $ 900 2,250 1,500 750 $5,400 1,350 $6,750 Lehigh’s markup is $1,350, which is 20% of the current $6,750 selling price ($1,350 ÷ $6,750). To achieve a 20% markup on a $5,500 selling price, the company must reduce its costs by $1,000. Selling price…………………………………. Less: 20% markup ($5,500 x 20%)………. Target cost…………………………………… $5,500 Current cost…………………………………. Less: Target cost………………………….. Required cost reduction…………………. $5,400 1,100 $4,400 4,400 $1,000 Yes. The company should focus its efforts on trimming non-value-added costs. These costs are associated with non-value-added activities (i.e., activities that are either (a) unnecessary and dispensable or (b) necessary, but inefficient and improvable). 5. If costs cannot be reduced below $5,400, Lehigh will have to reduce its markup to remain competitive. Assuming a desire to achieve the going market price of $5,500, the markup must equal $100 ($5,500 - $5,400), or 1.85% of cost ($100 ÷ $5,400). Given that the current markup on cost is 25%, a reduction of 23.15% is needed (25.00% - 1.85%). 6. The statement means that selling prices are a function of market conditions; however, the selling prices must cover a company’s costs in the long run. Also, in a number of industries, prices are based on costs. Yet, the prices are subject to the reaction of customers and competitors. 7. In the electronic version of the solutions manual, press the CTRL key and click on the following link: 10E - Build a Spreadsheet 15-42.xls