P/E ratio - University of Connecticut

advertisement

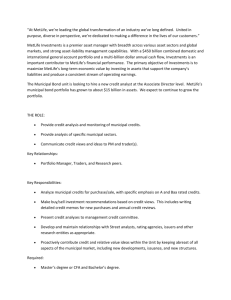

UNIVERSITY OF CONNECTICUT – STUDENT MANAGED FUND STOCK ANALYSIS REPORT Prepared by Zhiqun (Lily) Ding March 4, 2002 METLIFE INC (NYSE - MET) Industry: insurance (life) Sector: Financial services Valueline: Timeliness 2, Safety 2, Technical 2 Beta: 1.1 Large Cap: $ 20.1 billion StockScouter (CNBC): 8 (outperform the market) RECOMMENDATION Buy 150 shares @ $ 26.05 = $ 3,907.5 Stop loss order: $22.14 (-15%) Upside Review: $29. 96 (+15%) 1. BUSINESS SUMMARY MetLife, created by the demutualization of the Metropolitan Life Insurance Company on 4/7/00, is a leading provider of insurance and other financial services to a broad spectrum of individual and institutional customers. The origins of Metropolitan Life Insurance Company (MetLife) go back to 1863. The MetLife companies serve approximately ten million individual households in the U.S. and companies and institutions with approximately 33 million employees and members, including 88 of the FORTUNE 100 largest companies. MetLife is organized into six major business segments: Individual, Institutional, Reinsurance, Auto & Home, Asset Management and International. In November 2001, the Company acquired Seguros de Vida Santander and Soince Reinsurance Company, wholly owned subsidiaries of Santander Central Hispano in Chile. In June 2002, the Company acquired the former government-owned Aseguradora Hidalgo S.A., a life insurer in Mexico. The Company's unparalleled franchises and brand names uniquely position it to be the preeminent provider of protection and savings and investment products in the U.S. In addition, MetLife's international operations are focused on emerging markets where the demand for insurance and savings and investment products is expected to grow rapidly in the future. MetLife's well-recognized brand names, leading market positions, competitive and innovative product offerings and financial strength and expertise should help drive future growth and enhance shareholder value, building on a long history of tradition and integrity. Page 1 of 8 2. Financials /Benchmarking: Net income for 2002 was $1.61 billion, or $2.20 per diluted share. For 2001, net income was $473 million, or $0.62 per diluted share. For the FY ended 12/31/02, total revenues increased 6% to $34.06B. Net income from continuing operations before accounting change increased 92% to $1.74B. Revenues benefited from increased Auto & Home & Reinsurance segment premiums. Net income also benefited from lower interest credited to policyholder account balances. Auto & Home's combined ratio in 2002 was 99.4%, compared with 106% for the prior year. The improvement in the combined ratio was driven by increased average earned premium resulting from rate increases, fewer catastrophe and other weather-related losses, and better expense efficiencies. The value of international operations becomes more apparent in 2002. Operating earnings from International in the fourth quarter of 2002 were $38 million compared with an after-tax operating loss of $8 million in the year-ago period. The 2000-quarter included approximately $26 million of after-tax earnings from acquisitions in Mexico and Chile. Future potential: Valueline’s analyst raised 2003 EPS estimates to $2.8, which happens to be the same as Zacks’ projection. EPS in the following 12 months and earnings growth rates in the next 5 yrs are estimated by Zacks. EPS has strong growth trend; Earnings growth rates in the next 5 yrs. projected are higher than those of industry and S&P 500. Historical financial (Trailing 12 months) Growth rate Growth Rates % Company Industry S&P 500 4.70 0.20 0.10 Income (Qtr vs year ago qtr) 239.30 -0.60 13.70 EPS (Qtr vs year ago qtr) 254.80 0.00 18.10 Sales (Qtr vs year ago qtr) Page 2 of 8 Sales, income and EPS all beat industry and S&P 500; especially income and EPS have impressing growth. Financial health Financial Condition Company Industry S&P 500 Debt/Equity Ratio 0.20 0.31 1.17 Leverage Ratio 15.7 12.1 5.9 24.39 13.17 10.57 Company Industry S&P 500 Return On Equity 9.4 7.1 8.1 Return On Assets 0.6 0.6 1.4 Return On Capital 7.8 5.4 3.7 Book Value/Share High leverage ratio of 15.7 reflects healthy financial conditions. Management performance Investment Returns % Beautiful ROE, ROA, and ROC prove effective management. P/E ratio Price Ratios Current P/E Ratio Company Industry S&P 500 11.9 31.3 31.7 P/E ratio is pretty lower than industry average, and S&P 500, which implies Met’s price is undervalued relative to earnings. Cash Flow 2001 2000 Net Cash from Operating Activities 4799 1326 Net Cash from Investing Activities -3663 83 Net Cash from Financing Activities 2903 -764 Net Change in Cash & Cash Equivalents 4039 645 Free Cash Flow 4378 758 Met’s free cash flow shows the company's ability to repay debts, to reinvest and to pay dividends. 3. CHARTS Page 3 of 8 5--yr comparison MET has outperformed his competitor of Marsh & McLennan Companies, Inc. (MMC has the biggest Market Cap) and S&P 500 and Dow Jones average since its 2000 demutualization. Refer to Appendix II about competition. 4. RECENT NEWS Eileen McDonnell Appointed Senior Vice President, MetLife Individual Insurance Business Development February 27, 2003 11:45:00 AM ET NEW YORK--(BUSINESS WIRE)--Feb. 27, 2003--MetLife announced today that Eileen McDonnell has been appointed senior vice president, Individual Insurance Business Development. With 17 years of experience in the financial services industry, Eileen brings a successful track record of running individual markets as well as group pensions," said, Robert Henrikson, president, U.S. Insurance and Financial Services Businesses. "Her breadth and depth of experience make her a key addition to our leadership team." "MetLife and its retail distribution channels are committed to putting the customer at the heart of everything they do. That commitment, coupled with the company's desire for profitable growth and its strong brand and reputation, is what attracted me to MetLife," said Ms. McDonnell. "I am excited to lead the company's retail recruiting efforts while also concentrating on strategic planning and expense management." MetLife's Chairman And CEO To Speak at 28th Annual AIFA Conference February 27, 2003 4:02:00 PM ET Page 4 of 8 NEW YORK--(BUSINESS WIRE)--Feb. 27, 2003--MetLife, Inc.'s MET chairman and chief executive officer, Robert H. Benmosche, will be one of the life insurance panelists at the 28th Annual AIFA Conference on Monday, March 3, 2003, at 9:00 a.m. (CT). Mr. Benmosche will also be the conference's dinner speaker later that evening at 6:00 p.m. (CT). A.M. Best Assigns Indicative Debt Rating to MetLife, Inc.'s Debentures 2/25/2003 - 2:03:00 PM OLDWICK, N.J., Feb 25, 2003 (BUSINESS WIRE) --A.M. Best Co. has assigned an "a+" indicative senior unsecured debt rating to MetLife, Inc.'s (MetLife or the Company) (NYSE: MET) (New York) $1.00625 billion aggregate principal amount of its 3.911% debentures, due May 15, 2005. MetLife profit up, helped by investments February 10, 2003 5:55:00 PM ET In NEW YORK story "MetLife profit up, helped by investments," in headline please read ... "MetLife posts quarterly profit on investments". NEW YORK, Feb 10 (Reuters) - MetLife Inc. (MET), the No. 1 U.S. life insurer, on Monday said posted a quarterly profit rose, helped by investment gains. 5. MODELS Risk free rate (krf): km: Beta: 3.0% (10-year T-Note) 8.0% 1.1 DDM Model Capital Asset Pricing Model ks = krf + (km - krf) ks =3% + 1.1 * 5% = 8.5 % Discounted Cash Flow (DCF) PV- Dividends 01: 0.20 FV- Dividends 02: 0.21 gd = 5% PV- EPS1999: 1.21 FV- EPS2001: 2.56 Pmt =0, N = 3 gs = 28.38% Changes in ROE AND expected growth ROE01 = 6.5 ROE02 = 10.5 Page 5 of 8 Average dividend payout ratio = (0+ 0+12% + 14% +8%) / 5 = 7% Average Retention b: 1- 7%= 93% gr =b *ROE t+1 + ( ROE t+1 – ROE t)/ ROE t = 93% * 10.5 + (10.5 – 6.5)/6.5 = 71.3% Average g: (5+28.38+71.3)/3= 34.89% g>k It means this stock has experienced high growth rates, so new assumptions will have to be made (use multistage growth model). Multistage Growth Model Assumptions: 5 years of supernormal growth, where g=35% after that, g=6% Intrinsic value V0 = $ 28.92 Vo > P ($26.05) Buy decision. (The company pays small dividends to reinvest.) No Growth Model Price = E0/k = 1.92/0.085= $22.59 P/E Model (5-yr horizon) Estimated EPS: $3.5 (VL) Average P/E Ratio = (14.4+21.9+11)/3 = 15.77 Projected high price = $3.5 *15.77= $ 55.20 Lowest Price in last 3 years = $14.3 Present Price = $26.05 Upside potential = 29.15 Downside potential = 11.75 Upside/downside potential = 2.5 Buy decision 6. Analyst Ratings Recommendations Current 1 Month Ago 2 Months Ago 3 Months Ago Strong Buy 10 10 9 8 Moderate Buy 6 6 7 7 Hold 4 4 4 4 Moderate Sell 1 1 1 1 Strong Sell 0 0 0 0 Mean Rec. 1.79 1.79 1.83 1.88 Page 6 of 8 7. RISK FACTORS Changes in general economic conditions, including the performance of financial markets and interest rates; unanticipated changes in industry trends Heightened competition, including with respect to pricing, entry of new competitors and the development of new products by new and existing competitors; MetLife, Inc.'s primary reliance, as a holding company, on dividends from its subsidiaries to meet debt payment obligations and the applicable regulatory restrictions on the ability of the subsidiaries to pay such dividends; Regulatory, accounting or tax changes that may affect the cost of, or demand for, the Company's products or services Discrepancies between actual claims experience and assumptions used in setting prices for the Company's products and establishing the liabilities for the Company's obligations for future policy benefits and claims; The effects of business disruption or economic contraction due to terrorism or other hostilities Appendix I Key Ratios & Statistics Price & Volume Recent Price $ 52 Week High $ 52 Week Low $ Avg Daily Vol (Mil) Beta Share Related Items Mkt. Cap. (Mil) $ Shares Out (Mil) Float (Mil) Dividend Information Yield % Annual Dividend Payout Ratio (TTM) % Financial Strength 26.17 34.85 20.60 2.48 0.47 18,326.33 700.28 287.40 0.80 0.21 0.00 Quick Ratio (MRQ) Current Ratio (MRQ) LT Debt/Equity (MRQ) Total Debt/Equity (MRQ) NM 0.20 0.25 Valuation Ratios Price/Earnings (TTM) Price/Sales (TTM) Price/Book (MRQ) Price/Cash Flow (TTM) Per Share Data Earnings (TTM) $ Sales (TTM) $ Book Value (MRQ) $ Cash Flow (TTM) $ Cash (MRQ) $ Mgmt Effectiveness Return on Equity (TTM) Return on Assets (TTM) Return on Investment (TTM) Profitability 12.28* 0.57* 1.07 27.52 2.13* 45.86* 24.39 0.95 5.21 9.60* 0.59 7.90* Gross Margin (TTM) % Operating Margin (TTM) % Profit Margin (TTM) % 3.18 4.64* Mil = Millions MRQ = Most Recent Quarter TTM = Trailing Twelve Months Asterisks (*) Indicates numbers are derived from Earnings Announcements Pricing and volume data as of 02/28/2003 Source: www.multinvestor.com Name Appendix II MetLife Insurance Company Marsh & McLennan Companies, Inc. Page 7 of 8 Industry Insurance Brokers Insurance Brokers 8 8 Current $26.05 $40.29 FY End $33.28 $45.26 27.74% 12.35% $36.70 $51.82 40.88% 28.63% 33.42 Bil 10.44 Bil 1.61 Bil 1.37 Bil StockScouter rating Whose share price is estimated to gain the most? % Change Next Fiscal Yr % Change Who sold and earned the most over past 12 months? Total Sales Total Income Who grew sales and income the most over the past 12 months? Sales Growth Income Growth 4.70% 5.00% 239.30% 40.10% Whose shares are priced cheapest relative to earnings? Price/Earnings Ratio 11.80 16.40 Net Profit Margin 4.80% 13.10% Debt/Equity Ratio 0.20 0.58 -2.2% -15.6% 3.2% -12.6% -19.2% -25.9% 3-Mo Price Change -10.80% -10.80% 6-Mo Price Change -8.60% -8.60% 12-Mo Price Change -22.20% -22.20% Company relative to all stocks 3-Mo Relative Strength 55 27 6-Mo Relative Strength 66 35 12-Mo Relative Strength 50 43 Whose financial health is strongest? Whose share price has performed best in the last year? Company Price Performance 3-Mo Price Change 6-Mo Price Change 12-Mo Price Change Industry Price Performance Source: www.moneycentral.com Page 8 of 8