Six Percent Growth Still Doable

advertisement

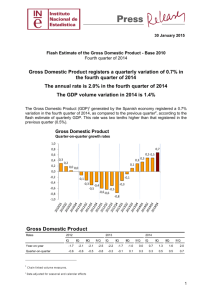

BERNARDO M. VILLEGAS September 16, 2011 Six Percent Growth Still Doable Understandably, there were many raised eyebrows when I told some colleagues of mine in the Makati Business Club that Philippine GDP can still rise by 8 percent in the second semester, making a 6 percent growth for the whole year of 2011 still within reach. I don't really mind being called a cock-eyed optimist or a prophet of boom. From where I stand, I can still see a close cooperation between the private sector and the government making a strong recovery from the 3.4 percent growth in the second quarter of this year possible. Let me give my reasons. First, let us take the low 3.4 percent growth in the second quarter in the right perspective. The second quarter of 2010 was an abnormally bullish period for the national economy because there were three extraordinary forces that converged then: the billions of pesos spent by the candidates for the May 2010 elections, the peaking of the pump priming that was a responsible response of the last Administration to the Great Recession, and a surge in exports that were the short-term results of a 7 percent growth in the U.S. GDP in the last quarter of 2009, a seeming recovery that was clearly a flash in the pan considering the double-dip recession that is staring the Americans in the face today. In short, the base on which the 3.4 percent growth was measured was abnormally high. The second semester of 2010 saw things returning to normal, with political spending reduced to zero, the beginning of belt tightening of the Aquino Administration, and the rapid deceleration in the growth of export. The only reliable source of growth of consumption expenditures was the continuous increase in the remittances from OFWs, albeit blunted by the appreciation of the peso. Thus, with a lower base from which 2 to grow, the possibility of an 8 percent growth in the second semester of 2011 is not an impossibility, if the following assumptions are considered realistic. I am convinced that the much larger budget deficit in July 2011 is already a harbinger of a significant increase in government expenditures, especially in infrastructures, for the rest of the year, even considering the uncertainties of the weather. After all, July was already in the thick of the typhoon season and we experienced a good number of serious weather disturbances during that month. I foresee a strong reversal of the 51.2 percent decrease in public construction recorded in the second quarter of 2011. I actually forecast an increase of 6 percent of the entire construction sector for the whole of 2011. I am confident of the organizational readiness of the critical departments--Budget, Public Works and Highways, Education, and Agriculture--to implement full steam ahead all the budgeted projects for the rest of the year, despite the few typhoons we may still encounter between now and December. I have this confidence because I have watched at close range the organizational reforms that were necessary in the DPWH before all the budgeted projects could be implemented with the minimum of corruption. When DPWH Secretary took over, he saw what had already been confirmed years ago by a study of the World Bank and the ADB: that the DPWH was one of the most corrupt departments with billions of pesos lost through below-standard works and actual pilferages. He had to spend a great deal of time reassigning regional directors and even firing some of them, attracting some legal suits on which he had to spend time. By June 2011, however, he felt he was ready for a more accelerated implementation of all the pending projects. He is even partnering with the Department of Education for the construction of school buildings. I am sure that these two departments will be contributing to a significant increase in public construction, to make my 6 percent increase in total construction possible. 3 I also have first-hand experience of what many credit rating agencies and banks don't see from their ivory towers. Through the Center for Research and Communication, I work closely with a team of economists, management specialists, urban planners and public administration professors in helping develop and implement economic programs for municipalities and provinces all over the Philippines. These LGUs are spread out as far as Mindanao, Leyte, Palawan, Oriental Mindoro, Aurora, Northern Luzon and Bicol. Everywhere I see numerous versions of PPP projects that do not attract the same attention as the big-ticket items (e.g. MRTs, LRTs, airports, power plants, etc) that are regularly monitored by the press. The LGU heads are keenly aware that they have a short window of opportunity to implement projects like farm-tomarket roads, irrigation systems, public markets, school buildings, mini-dams and innovative renewable energy projects, etc. They have started as early as July 2011 to implement these projects because they know that they only have some 18 months before January 2013 when it would be too late to show to their respective constituents that they deserve reelection because of concrete accomplishments. That is why I am of the belief that LGUs will contribute significantly to the increase in investments for the next 18 months. Therefore, I am bullish not only for the rest of the year but also for the whole of 2012 during which I see a 7 percent growth of GDP as attainable. Another reason for my optimism about investment is the extreme liquidity of the banking sector, with our savings rate exceeding 30 percent of GDP while our investment rate is still at the 15 to 17 percent level. Despite a temporary slowdown in consumer sales of most of the big businesses--compared to their star performances during the extraordinary year of 2010— domestic investors are heavily investing in energy, infrastructure, mining, residential construction, office buildings for BPOs, agribusiness, universities and hospitals, and tourism 4 facilities. Private and public investments will combine to make a 7 percent growth in Gross Domestic Capital Formation possible for the whole of 2011. Finally, Household Final Consumption Expenditure for the second semester will improve on its performance of 5.4 percent registered during the slow-growth second quarter of 2011. Given the already visible Christmas atmosphere in September 2011 and the always reliable increase in OFW remittances in the last quarter of the year, I see private consumption increasing by a record high of 7 percent for the second semester, led by food and non-alcoholic beverages; furnishings; household equipment and routine household maintenance (considering the boom in low-cost and medium-cost housing units); education; restaurants and hotels; and miscellaneous goods and services. Again, I don't mind being criticized as a super-optimist. At this stage of a significant improvement in the perception by outsiders about our positive investment climate (we just improved our ranking by ten positions in the World Economic Forum Global Competitiveness Index 2011-2012 and have moved up to just below investment grade in our credit rating), I am not about to relinquish my title of "Prophet of Boom." Have a Merry Christmas in September. For comments, my email address is bernardo.villegas@uap.asia. (Erratum: The secret document of Henry Kissinger was written to former President Richard Nixon (not Gerard Ford) and is entitled National Security Study Memorandum 200 [NSSM 200]). 5