American wind Energy Association

advertisement

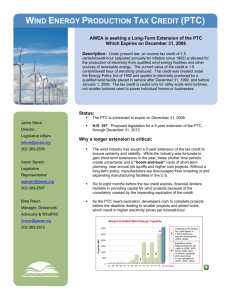

Wind: Powering a Cleaner, Stronger America American Wind Energy Association, 2008 The American Wind Energy Association ● www.awea.org Trade Association Overview The American Wind Energy Association ● www.awea.org The National Trade Association representing the Wind Industry in the U.S. Over 1300 Business Members, including: – Turbine Manufacturers – Component Suppliers – Project Developers – Electric Utilities – Lawyers, Consultants, Investors, etc. The American Wind Energy Association ● www.awea.org Trade Associations Facilitate Business for Members by: • Using Policy as Leverage on the Market • Providing Liaison to the Press and key audiences such as: – Policy Makers (Congress and other Federal agencies) – Electric utilities/the Customer – Financial Community • Networking Events – Organizing Annual Conference and Exhibition – Various Workshops throughout the year • Providing Information and Education through – Publications – Web site www.awea.org • Developing Technical Standards (Proposed “Grid Code”) The American Wind Energy Association ● www.awea.org AWEA MEMBER BENEFITS • Committees and Working Groups – Legislative – Transmission – Education • Education Resources and Networking Events – WINDPOWER 2008 – Annual Conference & Exhibition – Workshops: finance, transmission, siting, etc. • Member Services – – – – – Members only site Careers in Wind Job Board Online Store Wind Projects Database News Room: Media Outreach, Wind Energy Weekly, WindLetter The American Wind Energy Association ● www.awea.org Wind Power Market Overview The American Wind Energy Association ● www.awea.org Wind Growing Worldwide 100000 90000 1. Germany: 22,247 MW 80000 2. U.S.: 16,818 MW 70000 3. Spain: 15,145 MW 60000 4. India: 8,000 MW 50000 5. China: 6,050 MW 40000 30000 20000 10000 0 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Source: GWEC Global Market Report As of December 31, 2007 The American Wind Energy Association ● www.awea.org Rest of World Europe United States Wind Power Taking Off in U.S. 25000 20000 15000 Annual Cumulative 10000 5000 0 1995 1996 1997 1998 1999 2000 2001 2002 Source: AWEA Market Report As of December 31, 2007 The American Wind Energy Association ● www.awea.org 2003 2004 2005 2006 2007 2008 (proj.) Installed Utility-Scale Wind Power as of December 31, 2007 Washington 1163 Total 16,818 MW at 12/31/07 Montana 146 Oregon 885 Idaho 75 Wyoming 288 Utah 1 North Dakota 345 South Dakota 98 Nebraska Nebraska 20 73 Colorado 1067 California 2439 New Mexico 496 ME 42 Minnesota 1299 Kansas 364 Oklahoma 689 VT 6 NH 1 Wisconsin 53 Michigan 3 Iowa 1273 Illinois 699 New York 425 Pennsylvania 294 Ohio 7 WV 66 MA 5 Rhode Island 1 New Jersey 8 Missouri 57 Tennessee 29 > 1,000 MW 100 MW-1,000 MW Texas 4356 Alaska 2 Hawaii 63 The American Wind Energy Association ● www.awea.org < 100 MW Driving Forces Behind Wind’s Growth • Wind’s steadily improving economics – Federal production tax credit – Bigger turbines – More productive turbines • Benefits to utilities from wind in mix – No fuel cost – No environmental costs/degradation – Popular with customers • Fossil fuel prices increasing/volatile • Federal and state policy initiatives The American Wind Energy Association ● www.awea.org Federal and State Policies to Promote Wind Power The American Wind Energy Association ● www.awea.org Federal Production Tax Credit (PTC) • Eligibility period now extended through end of 2008. Provides 2¢ per kWh for 10 years of operation to wind plant owners • Lowers price of electricity to customers • Industry needs long-term extension to encourage investment The American Wind Energy Association ● www.awea.org Historic Impact of PTC Expiration on Annual Installation of Wind Capacity The American Wind Energy Association ● www.awea.org Renewable Portfolio Standard (RPS) • Requirement that utilities supply a portion of their electricity from renewable resources by a certain date • Would create stable market for wind, which would drive down cost of energy • Texas good example of how RPS can drive development • Creates incentive to solve implementation issues • 26 states and D.C. have RPS policies The American Wind Energy Association ● www.awea.org Transmission Grid Operating Rules • Nondiscriminatory interconnection of new generation facilities • Real-time balancing markets instead of schedule deviation penalties • Elimination of rate “pancaking” and allocation of transmission facilities’ costs to end-use customers rather than generators • Equitable allocation of congested capacity among competing users The American Wind Energy Association ● www.awea.org Clean Energy Superhighways New transmission lines built to take advantage of the nation’s wind resources could access tens of thousands of megawatts of new wind capacity The American Wind Energy Association ● www.awea.org Climate Policy • AWEA is involved in clean air and global warming policy to make sure that wind power projects are recognized for their zero-emissions energy generation and allocated emission allowances • Wind energy can be included by allocating allowances based on generation output, which creates an incentive for efficient and clean energy sources • Wind power is readily available to deliver zeroemissions electricity on a large scale The American Wind Energy Association ● www.awea.org Green Power Market • Green Pricing – No competition, utility offers customers choice of supporting wind power construction • Green Marketing – In competitive market, customers empowered to choose service providers that contract to purchase renewables • Green Tags – Environmental attributes purchased separately from electricity The American Wind Energy Association ● www.awea.org Small Turbine Incentives • Investment tax credit • Buy-down programs • Sales tax exemptions • Model zoning ordinances • Reasonable interconnection standards • Net metering The American Wind Energy Association ● www.awea.org Future of Wind Energy in U.S. The American Wind Energy Association ● www.awea.org 20% Vision: Cumulative Capacity Installed Preliminary: fromEnergy forthcoming report The American Wind Association ● www.awea.org 20% Vision: Market Growth Potential Onshore Offshore Total MW 239,500 53,900 Total Number of Turbines 79,130 17,975 Preliminary: fromEnergy forthcoming report The American Wind Association ● www.awea.org 20% Vision: Policy & Market Challenges • Establishing Stable Policy • Addressing Value Chain Challenges • Building Transmission • Addressing Challenges associated with Wind’s Variability • Meeting Siting Challenges • Improve Wind’s Ability to Compete on Cost The American Wind Energy Association ● www.awea.org