Capital Reduction: Benefits, Procedures & Regulations

advertisement

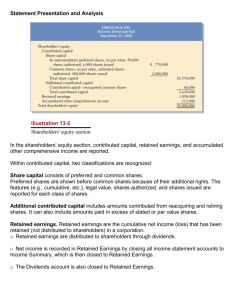

Issues for consideration The capital reduction of retained earnings and reserves set in accordance with the company’s statement of financial position carries tax payment duties for shareholders who receive it accordingly. The company must inform its creditors in writing about the upcoming capital reduction. Creditors have the right to object to the reduction within two months from the notification date. Capital Reduction Capital Reduction Capital Reduction Benefits of capital reduction Reducing a company’s capital is… Company A way to reduce its paid-up capital by either one of two methods, as follows: TIPS If creditors object to the capital reduction, the company may negotiate and repay them in order to proceed with the plan. “The company reduced capital by reducing the number of shares on August 3, 2010 in order to wipe out the deficit in retained earnings that was incurred during normal business undertakings. The company did not need capital reduction, but with the deficit in retained earnings, the company was not able to pay dividends despite the fact that the company hadnet profit earnings. Thus, reducing capital to offset the deficit in retained earnings was a proper option that did not affect the company’s financial status. It positively impacted shareholders by giving them the chance to receive dividends or even capital gains from share price movement”. Mr. Polpat Karnasuta, President, Nawarat Patanakarn Pcl., (NWR) To support future dividend payments if the company is experiencing accumulated loss. Capital reduction will compensate for a deficit in retained earnings allowing the firm to pay dividends without waiting for current operating results. 1) Reducing par value 2) Reducing the number of shares To support capital increases by new investors To encourage efficiency of capital usage, which consequently improves financial ratios (e.g., ROE, ROA, total asset turnover) and increases the company’s attractiveness among investors. Shareholders To have more opportunities to receive dividend payments if the company is experiencing a deficit in retained earnings. Relevant notifications - The Public Limited Company Act B.E.2535, Section 139-144 - Civil and Commercial Law, Section 1224-1228 www.set.or.th >> Regulation >> Regulation by Subject Capital reduction to support future dividend payments If a company has a deficit in retained earnings, laws prohibit it from paying dividends. The company may reduce its capital and use the funds obtained to offset the deficit in retained earnings. The company will consequently be able to pay dividends because (a) its retained earnings become positive and (b) the company’s statutory reserves are allocated and reserved in accordance with regulatory requirements. >> Disclosure joins with CIMB Securities (Thailand) Co., Ltd. 62 The Stock Exchange of Thailand Building, Ratchadapisek road, Klongtoey, Bangkok 10110 Listed Company Development Department, The Stock Exchange of Thailand Capital Reduction Capital Reduction Capital reduction procedures Reducing capital to support a capital increase by new investors A company may foresee a business opportunity that it is unable to take advantage of because it has been experiencing accumulated losses. If the firm wants to raise funds, it can reduce its capital so that its capital level truly reflects the past loss. Thus, new investors will be able to inject funds at a price that properly reflects the firm’s value. The board of directors resolves to reduce capital. At least 14 days Report to SET within the date on which the board resolves to reduce capital or within 9 a.m. of the next business day. Record date is set* Reducing capital to offset a deficit in retained earnings Within 2 months Reducing capital to encourage using capital more efficiently and thus improve financial ratios, e.g., ROE, ROA, or total asset turnover If the company has a large amount of excess cash and does not need to use aforementioned funds in the near future, the firm may reduce capital to return the excess funds to shareholders. Examples are as follows: Shareholders’ meeting resolves to reduce capital (voting > 75% of attending shareholders with voting rights) Within 14 days Cash 800 Liabilities Other assets 400 Paid-up capital Statement of financial position – After capital reduction of THB800 million 200 1,000 Retained earnings Cash 0 Other assets 400 Reduce paid-up capital only (Reducing capital to lower than ¼ of total capital is not permitted.) Paid-up capital 200 (1,000-800) 0 End of period for objections from creditors Reducing capital by reducing par value Reducing capital by reducing number of shares Within 14 days Shareholders’ equity 200 Board of directors resolves to set share register book closing date Liabilities and Liabilities and shareholders’ equity 1,200 200 Retained earnings 0 Shareholders’ equity 1,000 Total assets 1,200 Liabilities Total assets 400 shareholders’ equity (Capital can be reduced to lower than ¼ of total capital) Reducing capital to return excess funds to shareholders The company informs creditors of the meeting’s resolution in writing. Within 2 months Statement of financial position – Before capital reduction Capital reduction sequence is as follows: Other reserves >> Legal and Reserves >> premium on share capital >> Paid-up capital 400 Posting SP, XN signs Example: If net profit = THB20 million per annum, Return on Equity (ROE) and Debt/Equity (D/E) ratios can be shown as follows: Ratio Return on Equity Debt/Equity Before capital reduction After capital reduction 2.0% 10.0% 0.2 times 1.0 time Here, the company has THB800 million in cash and anticipates no need to use it. If it reduces capital, its ROE will be improved, while its D/E ratio will remain low. 3 business days Shares register book closing date for collecting shareholder names Registering changed registered capital with the Ministry of Commerce Within 3 business days Reporting to SET about registering capital reduction Commencing stock trading with the new registered capital Remark * The record date is when the company determines the list of shareholders eligible to receive particular rights. The share register book closing date must be the following business day. Listed Company Development Department The Stock Exchange of Thailand