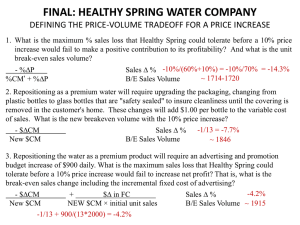

1 Hedging Diagrams 2 Spot

advertisement

UCLA Anderson – MGMT234A: International Financial Markets (Winter 2013)

Professor Andrea Eisfeldt

Week #8

March 4, 2013

Handout written by Shenje Hshieh†

Reminder: Read chapters 3.1, 3.2, 3.3, and 20.1 in Bekaert and Hodrick (2012). International

Equities Case due next week in class.

1

Hedging Diagrams

Please refer to the figures located on the last two pages of this handout for this section.

1.1

Protecting Against Future Value Loss of Assets

Suppose you have bought an asset (e.g. a bond, car, house, stock, etc.). This means you are long

that asset and can only make a profit if the value of that asset rises. However, you could potentially

lose money (i.e. net after purchase price) if the asset value drops. We can protect ourselves against

such events with derivatives, specifically with options and forwards (see the first three figures of the

last two pages of this handout). For the following graphs, the numbers assigned for each tick on

the x-axis are arbitrary; 0 represents the current price of the underlying asset. The dashed red line

represents the payoff after accounting for the cost of purchasing an option or the revenue gained

from selling an option.

1.2

Protecting Against Future Value Gain of Liabilities

Suppose now you have borrowed and sold an asset. This means you are short that asset and can

only make a profit if the value of that asset declines. However, you could potentially lose money

(i.e. net after sell price) if the asset value rises. We can limit our losses similarly with futures and

options (see the last three figures of this handout).

2

Spot-Forward/Futures Parity

From this point on, I will use forward price and futures price interchangeably.

Claim: The no-arbitrage condition implies that Ft = St er(T −t) .

Proof: Case 1: Suppose Ft > St er(T −t) . Then the following is an arbitrage opportunity:

1. At time t, borrow St (from a bank) at the continuously compounded rate of r

2. Buy 1 unit of the asset for St

3. Short forward (i.e. promise to sell underlying asset at price of Ft at time T )

4. At time T , deliver 1 unit of the asset to receive Ft and repay loan of St er(T −t)

†

Please email me at shenje.hshieh.2015@anderson.ucla.edu if there are any errors.

1

5. Receive positive profit of Ft − St er(T −t) > 0

Case 2: Suppose Ft < St er(T −t) . The following strategy yields an arbitrage profit:

1. Short 1 unit of the asset for St and invest at the continuously compounded rate of r

2. Long forward (i.e. promise to buy underlying asset at price of Ft at time T )

3. At time T , receive St er(T −t) and buy underlying asset for Ft

4. After closing out the short position on the asset, receive positive profit of St er(T −t) − Ft > 0

We have exhausted all cases; they all contradict the no-arbitrage premise. Therefore, we conclude

that Ft = St er(T −t) . Alternative proof: Consider longing a forward contract or buying a futures contract. At maturity

date T , the payoff is ST − Ft , where ST is the spot price of the underlying asset at maturity T and

Ft is the forward/future price set at time t. Suppose the underlying asset pays no dividends. The

amount you put up today to buy the futures contract (or enter a forward contract) is zero. This

means the present value of the futures/forward contract must also be zero:

PV(St − Ft ) = 0 ⇒ PV(ST ) = PV(Ft )

(1)

Since PV(ST ) = St and PV(Ft ) = Ft e−r(T −t) , we conclude that Ft = St er(T −t) . We can make a

similar argument for shorting a foward contract or selling a futures contract. 2.1

Cost of Carry

Intuitively, the forward/futures price should capture all the costs of holding the underlying asset (e.g.

storage cost), but none of the benefits of actual ownership of the underlying asset (e.g. dividends).

The cost of carry z summarizes the costs and benefits adjustments in the forward non-arbitrage

pricing formula:

Ft = St e(r−d+s−c)(T −t) = St ez(T −t)

(2)

Convenience Yield (c): This is a premium associated with owning the underlying asset. This reflects the market’s expectations concerning future availability of the underlying asset. For example,

if there are low inventories of an asset, there is a greater chance of shortage, which means a higher

convenience yield. The opposite is true when high inventories exist. Thus, c is subtracted from the

cost of carry.

Dividend Rate (d): Some assets emit cash that is not recieved by the forward. This cash can be

expressed as a rate and is also subtracted from the cost of carry.

Storage Cost Rate (s): Storage costs mostly applies to commodities such as gold and silver.

Thus, this cost is added into the cost of carry.

2

3

3.1

Mean-Variance Portfolio Analysis (No Riskless Asset)

Definitions

Assume the following variable assignments and definitions:

Expected k Asset Returns : Rk×1

Unit Vector : 1k×1

Portfolio Weights : Xk×1

Covariance Matrix of k Asset Returns : Vk×k

Expected Portfolio Return : µ

3.2

(3)

Minimize Risk Given µ

We want to find X∗ , given µ, that solves the following minimization problem:

X∗ = arg min X0 VX

X

subject to

X0 R = µ

X0 1 = 1

(4)

Step 1: Set up Lagrangian and take first order conditions with respect to X

L = X0 VX − λ1 (X0 R − µ) − λ2 (X0 1 − 1)

∂L

= 2VX − λ1 R − λ2 1 = 0

∂X

λ1

1 −1 ∗

R 1

X = V

λ2

2

(5)

Step 2: Solve for λ1 and λ2

0 0

λ1

1 R0

1 R0 V−1 R R0 V−1 1 λ1

1

µ

RX

R

λ

−1

R 1

=

=

=

= A 1

0

0 X =

0 V

0 −1

0 −1

1X

1

λ2

1

λ2

2 1

2 1 V R 1 V 1 λ2

2

(6)

Solving for λ1 and λ2 , we get:

λ1

−1 µ

= 2A

λ2

1

(7)

Step 3: Substitute λ1 and λ2 into X∗

∗

X =V

−1

−1 µ

R 1 A

1

3

(8)

4

4.1

Hedging with Futures

Definitions

Consider the following definitions:

Ft − Ft−1

St−1

St − St−1

Asset Return : RS,t =

St−1

Basis : Bt = Ft − St

Bt − Bt−1

Basis Return : RB,t =

St−1

Futures Pseudo Return : RF,t =

(9)

It follows that:

RF,t = RS,t +

Bt − Bt−1

= RS,t + RB,t

St−1

(10)

Note that there is no particular economic meaning for the futures pseudo return or the basis return.

4.2

Proof of the Minimum Variance Hedge Ratio Formula

Suppose we expect to sell N units of an asset at time t and choose to hedge at time t − 1 by shorting

futures contracts of M units of a similar asset. Denote the hedge ratio h by:

h=

M

N

(11)

The total amount realized for the asset when the profit or loss on the hedge is taken into account

Vt can be written as:

Vt = St N − (Ft − Ft−1 )M

Vt = St−1 N + (St − St−1 )N − (Ft − Ft−1 )M

(12)

where St−1 and St are the asset prices at times t − 1 and t, and Ft−1 and Ft are the futures prices at

time t − 1 and t, respectively. Substituting the hedge ratio into the equation above, the expression

for Vt can be written as:

Rh,t

Vt = St−1 N + N ((St − St−1 ) − h(Ft − Ft−1 ))

Vt

= N + N (RS,t − hRF,t )

≡

St−1

4

(13)

Because St−1 and N are known at time t − 1, the variance of Rh,t is minimized when the variance

of RS,t − hRF,t is minimized. Our minimization problem is thus:

arg min Var(RS,t − hRF,t ) = arg min Var(RS,t ) + h2 Var(RF,t ) − 2hCov(RS,t , RF,t )

h

h

(14)

Taking the first order condition, we arrive at:

h∗ =

Cov(RS,t , RF,t )

Var(RF,t )

(15)

as mentioned in the lecture notes. Substituting h∗ for h in Var(Rh,t ), we get:

Var(Rh,t ) = Var(RS,t ) + h2 Var(RF,t ) − 2hCov(RS,t , RF,t )

2

Cov(RS,t , RF,t )

Cov(RS,t , RF,t )

Var(RF,t ) − 2

Cov(RS,t , RF,t )

= Var(RS,t ) +

Var(RF,t )

Var(RF,t )

Cov(RS,t , RS,t + RB,t )2

= Var(RS,t ) −

Var(RF,t )

(16)

Var(RS,t )Var(RF,t ) − Cov(RS,t , RS,t + RB,t )2

=

Var(RF,t )

Var(RS,t )Var(RB,t ) − Cov(RS,t , RB,t )2

=

Var(RF,t )

Var(RS,t )Var(RB,t )(1 − ρ2SB )

=

Var(RF,t )

Note that the hedge is “perfect” only if Var(Rh,t ) = 0. There are two scenarios in which this can be

true: (1) the basis has zero volatility (Var(RB,t ) = 0) or (2) the basis is perfectly correlated with

the spot price (ρSB = 1).

5

Mean-Variance Optimal Hedging with Foreign Exchange

Futures

Let hi for i ∈ {1, ..., m} be the hedge ratio to be chosen for each m currency in our expanded

minimization problem. Our new minimization problem is now the following:

0

X∗

X

= arg min X H V(k+m)×(k+m)

H∗

H

X,H

subject to

0

X H R(k+m)×1 = µ

0 1k×1

X H

=1

0m×1

5

(17)

where H is a m × 1 vector of hedge ratios hi . We use the same method as in section 3 above to solve

our optimal portfolio weights and hedge ratios. Note that the asset returns vector R is expanded

to include the m currency futures in addition to the k assets (priced in local currency).

6

6.1

Misc. Questions Asked During the TA Session

Should Forward and Future Prices Equal?

They should when interest rates are constant. See the appendix of chapter 3 of Fundamentals of

Futures and Options Markets by John C. Hull for proof.

6

Unhedged Payoff

10

Payoff

5

5

g(S) + f (S)

0

0

−5

−5

−5

0

5

10

Unhedged Payoff

10

−10

−10

10

5

Payoff

5

0

−5

Hedged Payoff

10

f (S) = F − S

g(S) = S

−10

−10

−5

0

5

10

Spot Price at Maturity (S)

Long Put Option Payoff

−10

−10

5

0

0

0

5

10

5

10

5

10

Hedged Payoff

10

5

−5

g(S) = S

0

f (S) =

−5 max{K − S, 0}

−5

−10

−10

−5

0

5

10

Unhedged Payoff

10

−10

−10

10

5

Payoff

Short Forward Payoff

10

−5

0

5

10

Spot Price at Maturity (S)

Short Call Option Payoff

−5

g(S) + f (S)

−10

−10

5

0

0

0

Hedged Payoff

10

5

−5

g(S) + f (S)

g(S) = S

0

f (S) =

−5 max{S − K, 0}

−5

−10

−10

−5

0

5

10

−10

−10

−5

0

5

10

Spot Price at Maturity (S)

7

−5

−10

−10

−5

0

Unhedged Payoff

10

Payoff

5

0

5

−10

−10

−5

0

5

10

Unhedged Payoff

10

Payoff

g(S) = −S

−10

−10

−5

0

5

10

Unhedged Payoff

10

Payoff

0

−5

−5

−10

−10

−5

0

5

10

Spot Price at Maturity (S)

Long Call Option Payoff

0

0

−10

−10

−5

−10

−10

−5

0

5

10

−5

0

5

10

Spot Price at Maturity (S)

Short Put Option Payoff

f (S) =

max{K − S, 0}

−5

0

−5

−5

−10

−10

−5

0

5

10

Spot Price at Maturity (S)

8

5

10

−5

0

5

10

5

10

Hedged Payoff

10

0

0

g(S) + f (S)

−10

−10

5

−5

Hedged Payoff

10

5

5

g(S) = −S

−10

−10

5

10

5

g(S) + f (S)

0

f (S) =

−5 max{S − K, 0}

−5

0

5

10

5

Hedged Payoff

10

f (S) = S − F

g(S) = −S

−5

0

Long Forward Payoff

10

g(S) + f (S)

−10

−10

−5

0