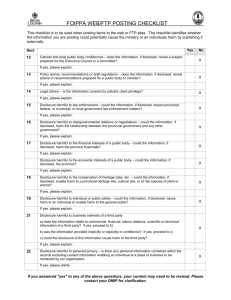

FINANCIAL DISCLOSURES CHECKLIST

advertisement