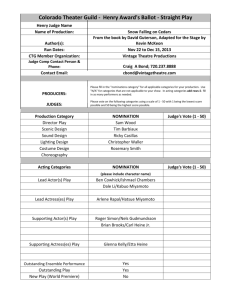

INSTRUCTIONS FOR COMPLETING THE JUDICIAL FINANCIAL

advertisement

REVISED FOR 2004 REPORTING YEAR INSTRUCTIONS FOR COMPLETING THE JUDICIAL FINANCIAL REPORTING STATEMENT APPLICABLE TO MUNICIPAL COURT JUDGES (Pursuant to Rule 1:18B) DEFINITIONS Judge or Self means any full-time or part-time municipal court judge. This includes Vicinage Presiding Judges, Chief Judges of municipal courts, judges of joint municipal courts and acting or temporary judges. Spouse means the spouse of a judge residing in the same domicile. Child means any unemancipated biological or adopted child or stepchild of the judge residing in the same domicile. Joint means jointly owned such as between a judge and spouse, judge and child, and/or judge’s spouse and child residing in the same domicile. GENERAL REPORTING INFORMATION • Each judge must file a Judicial Financial Reporting Statement annually, even if the judge has no information to report. However, a judge who was appointed to office during the current calendar year need not file a statement for the preceding calendar year provided he or she was not a judge during any portion of that year. • At the top of the first page of the Statement, in box 1, enter your name. In box 2, enter the courts to which you are assigned as a full or part-time, temporary or acting municipal court judge and the municipalities covered by each court to which you are assigned or cross-assigned. If you are cross-assigned to all courts within a county or vicinage, state that fact rather than listing each court. If you are assigned or cross-assigned to a joint municipal court, list all municipalities that are covered by that court. In all cases, indicate as to each court that you list whether you are assigned or cross-assigned as a temporary or acting judge. In box 3, list all vicinage(s) and counties to which you are assigned or cross-assigned. In box 4, list either your primary chambers address or your office address, depending on where you would like correspondence to be sent regarding your Statement. • If additional space is needed to provide any information or explanation use Section IV and, if necessary, attach additional pages indicating the applicable box or section being supplemented. • For each entry, check the box of the appropriate recipient/owner/investor (i.e., self, joint, spouse or child). If jointly owned between a spouse and a child, report the information under “spouse.” • Shaded boxes on the Statement indicate that no information is required to be provided in that box. • Do not list Social Security Numbers, telephone numbers, or home addresses for yourself or for your spouse or child. Also, do not list the name of your spouse or child. • Do not enter actual income amounts. SECTION I. EARNED INCOME IN EXCESS OF $1,000 Earned income means employee compensation and/or earnings from selfemployment. Such income may be for compensation/earnings for present employment/activities or for prior employment/activities. The seven categories of earned income are described below. A. Salary - fixed periodic compensation for personal services. Examples: salary or payment received for performing part-time or full-time judicial services (including compensation as a temporary or acting municipal court judge); regular employee wages, including salary received from a law firm as an associate, from a corporation or from a public entity for non-judicial services; a proprietor’s regular draw from a business; and distribution of partnership profits. B. Bonuses - premiums, extra or irregular remuneration in consideration for services performed. Examples: cash; gift certificates; company stock; reward for job performance, such as an all-expenses paid trip. C. Royalties - payment for the use of intangible personal property such as a patent or copyright. Examples: book royalties; payment for the right to export mineral rights; and patent royalties. D. Fees - fixed charges, usually for a professional service. Examples: legal, medical, or broker fees. 2 E. Commissions - fees paid to an agent or employee for transacting business or performing a service, usually a percentage of money received from the total amount paid to the agent or employee responsible for the business. Examples: original and renewal compensation to an insurance agent or a salesperson’s share of a sales transaction. F. Profit Sharing - a plan established and maintained by an employer to provide for participation in profits by employees and their beneficiaries. Example: an employee profit sharing plan. G. Pensions - income received from pension payments, other than federal pension or disability retirement payments (as to such federal payments, see the Unearned Income Instructions below). Examples: pension payments from a publicly held corporation; pension distribution received as a life beneficiary upon the pensioner’s death. General Instructions – Earned Income • Judges are required to report in this section earned income received by themselves, their spouses and unemancipated child. The source of earned income must be reported only if more than $1,000 is received from the source in the calendar year for which the Statement is being filed. Do not enter the actual income amount. You must specifically identify the source of the earned income but do not enter the city or state of the source of the earned income unless those public entities are the source. • The Statement should include all judicial service salaries that you received during the reporting year, from all courts to which you are assigned as a full or part-time, temporary or acting municipal court judge or from government agencies. Again, do not report the amount, only the source. If you are assigned or cross-assigned to a joint municipal court, list all municipalities that are covered by that court. In all cases, indicate as to each court that you list whether you are regularly assigned or crossassigned. Municipal court judges also should report sources of all other earned income, including pension payments (Category G). • For income received as sole proprietor or partner (e.g., a solo practitioner in a law firm), report the name and nature of the sole proprietorship or partnership (e.g., Jones and Jones, Esquires). If the name of the law firm from which a judge is receiving buyout payments has changed since the judge’s appointment, enter the current name of the law firm. 3 • Individual client fees, customer receipts, or commissions on transactions received through an employer or business do not have to be reported separately as sources of earned income. Do not identify individual clients by name, unless the client is a public entity employing you to perform non-judicial services. • Where a judge’s spouse receives an all-expenses paid trip as a reward for job performance and the judge accompanies the spouse on the trip without cost to the judge, report the trip under bonuses (IB) as to the spouse. The trip is not considered a gift as to the judge. • If you are affiliated with a law firm as “of counsel”, report referral fees received from the law firm. The source of such payments is the law firm. Whether such payments constitute salary, bonuses or fees depends upon the exact nature of the judge’s contractual relationship with the law firm. • If there is a need for explanation of the nature or source of income earned, use section IV for that purpose. SECTION II. UNEARNED INCOME IN EXCESS OF $1,000 Unearned income means income derived from the sale, rental, growth, or conversion of capital, or receipt of a gift as defined herein. Financial institution means a bank, saving and loan, credit union, or similar institution. The five categories of unearned income are described below. A. Investment Income - income received from the investment of capital such as dividends, capital gains or interest, except income from securities issued by the federal government and accounts held at financial institutions. Examples of required reporting: stock or mutual fund dividends, capital gains received from the sale of real estate or a business; interest income (other than interest earned on savings or checking accounts or on certificates of deposit at a financial institution); gains from the sale of stocks, bonds or other obligations. B. Rents - payments received for the use of real or tangible personal property. Examples: rental income from leasing an apartment, business, plane, or automobile. C. Trusts – distributions from a trust. D. Estates – distributions from an inheritance. 4 E. Gifts - any money or item valued in excess of $1,000 and for which a consideration of equal or greater value is not received; this does not include any loan made in the ordinary course of business, or any devise, bequest, investment estate distribution or principal distribution of a trust or gift received from a member of a judge’s household or from a relative within the third degree of consanguinity of the judge or the judge’s spouse, or from the spouse of that relative. See Commentary, Section 3.C.(3) of the Code of Judicial Conduct for definition of third degree of consanguinity. Section 5.D.4 of the Code of Judicial Conduct restricts the acceptance of gifts by judges. (See also Guideline VI.B.3) General Instructions – Unearned Income • Judges are required to report in this section unearned income received by themselves, their spouses and unemancipated children. • Passive investment income from a limited liability company should be reported under Investment Income II.A. • Unearned income includes income from stocks, bonds and mutual funds held in retirement and educational accounts. However, distributions from such accounts need not be reported. • The following need not be reported: the receipt of Social Security or other federal pension or disability retirement benefits (example: U.S. Army disability retirement benefits); interest earned on a savings or checking account or on a certificate of deposit in a financial institution; the balance in an account in the State Deferred Compensation Plan; interest on a zero coupon bond in an IRA account until the income from the bond is actually received, upon the bond’s maturity date; or dividends on life insurance policies that may be used either to reduce premiums or to provide paid up additions to the value of the policy. • The source of unearned income must be reported only if more than $1,000 is received from the source in any calendar year. Income means gross income received and not necessarily profit. Consequently, as an example, a beachfront property rental income of $10,000 should be reported as a source of income even if expenses for the property (mortgage, taxes and maintenance) were $12,000. • Enter only the name of the source of unearned income in excess of $1,000 per year. Do not enter the amount of unearned income. You must specifically identify the source of the unearned income, but do not enter the address of the source, except as indicated below regarding capital gains from the sale of property and rents. 5 • Income received from the buyout of a judge’s interest in a building owned by the judge’s former law firm should be reported under Investment Income II.A. as a capital gain, assuming that the amount paid by the judge’s former law firm for the judge’s interest in the building exceeded the amount that the judge paid for that interest by $1,000 or more. • For income from investments, trusts and estates, list the names of the paying companies or individuals. For each entry check the box of the appropriate recipient. For example, the source would have to be reported only for stock dividends with a value totaling more than $1,000 in a given year. Any individual sale of stock that resulted in a capital gain in excess of $1,000 must be separately listed, including the name of the stock and the fact that the income was derived from a capital gain. If you receive a dividend from a stock in the form of additional stock (rather than as a cash dividend in excess of $1,000) and your receipt of such additional stock does not subject you to any additional Federal or State income taxation, do not report the receipt of such additional stock. • For dividends, capital gains or interest derived from securities held in brokerage accounts, list the name of the issuer of the security rather than the brokerage firm. • For a capital gain from the sale of real property, enter only the name of the municipality and the state where the property is located. Do not list the street address or house number of the property. Enter the name of the buyer. • For mutual funds or other managed funds over which the individual holding the interest does not exercise discretion, report the name of the specific fund if income is in excess of $1,000 received during the calendar year, e.g., Dreyfus Premier Core Value Fund – Class A. Do not report the amount of income received, individual assets owned by or transactions by the fund. Rather, the fund itself is considered to be the source of the income, even though the $1,000 income includes dividends, interest, or capital gains earned with respect to stocks, bonds, etc., held by the fund. Judges are required to report income from any individual mutual fund in a tax shelter annuity or IRA. • Do not enter or attach any information that is not explicitly required by the Statement or Instructions, such as a brokerage statement or a list of the number of shares of stock owned, any account numbers, or actual income amounts earned. 6 • For unearned income derived from a business, list the name of the business only. • For rents, enter only the name of the municipality and the state in which the property is located. Do not list the street address or house number. Enter the name of the payor. If a judge, spouse or unemancipated child holds an interest in an entity that receives income from rents, but the judge, spouse or unemancipated child receives this unearned income in the form of investment income, e.g., a partnership distribution, this income should be reported in the “investment income” category rather than the “rents” category. In the case of a partnership that owns rental properties and receives rental income, where the judge’s interest is in the partnership itself rather than in the rental property owned by the partnership, only report the partnership distribution(s) you received during the preceding calendar year, and not the rental income received by the partnership. • For distributions from a trust, enter the names of the trust, the settlor and the trustee, the nature of the trust and a checkmark in the appropriate box indicating the beneficiary. • For distributions from an estate, enter the names of the decedent and executor or administrator and a checkmark in the appropriate box indicating the beneficiary. Do not report life insurance benefits received as a beneficiary upon the insured’s death. Report a pension distribution a judge receives upon the pensioner’s death under Pensions IG. • For gifts, list the source of any gifts valued at more than $1,000 received by the judge, the judge’s spouse, or the judge’s unemancipated children. The name of the source must be reported if the value of any single gift is more than $1,000 or if the aggregate value of gifts from that source is greater than $1,000 in a calendar year. The Code of Judicial Conduct restricts the acceptance of gifts by judges. • The reporting requirements relating to distributions from trusts and estates and inter vivos gifts do not apply where the settlor, decedent or donor is a member of the judge’s household or relative within the third degree of consanguinity of the judge or the judge’s spouse, or the spouse of that relative. 7 SECTION III. ANY INTEREST HELD IN LAND OR BUILDING IN ATLANTIC CITY (OTHER THAN JUDGE’S RESIDENCE) Judges are required to report on any interest that they, their spouse or their unemancipated children have in any property or building, located in any city in which casino gambling is permitted, that is, in Atlantic City. Excluded from this reporting requirement is the judge’s residence. General Instructions • Report any ownership, holding, or control of an interest in any land or building in any city in which casino gambling is authorized, that is, in Atlantic City. The address and lot location of the building or land must be specified. This reporting requirement is applicable to the judge, the judge’s spouse, and the judge’s unemancipated children. It does not include the judge’s residence. • If the interest is in the form of a corporate or partnership interest, report the name of the corporation or partnership as well. SECTION IV. ADDITIONAL INFORMATION OR EXPLANATIONS Use this section for any necessary explanations as to any items reported on the Statement or to request a filing extension (see below). Additional information or explanations should not be reported on any other portion of the Statement. Indicate the box or section being explained or supplemented. (Attach additional pages if necessary.) SECTION V. CERTIFICATION Prior to their submission completed Financial Reporting Statements must be signed and dated by the judge personally (not by a preparer, if prepared by other than the judge). Statements must have an original signature, not a facsimile or stamped signature. Please make sure that you have used the most recent version (“Revised December 2004”) of the Statement. Make sure also that you have used the Statement specifically designated for use by municipal court judges. 8 FILING PROCEDURE Submit only one Statement, even if you are assigned to more than one municipal court or more than one joint municipal court. Each municipal court judge must file a completed and signed original Judicial Financial Reporting Statement covering the preceding calendar year by April 15 of the current year by submitting the Statement to the judge’s Assignment Judge. Faxed Statements will not satisfy the filing requirements of the Rule. The Assignment Judge will in turn forward the Statements received for that vicinage to the Administrative Director of the Courts for filing with the Supreme Court. A judge who heard cases in more than one vicinage during the reporting year should submit a Statement to the Assignment Judge of only one vicinage and should so advise the Assignment Judge(s) of the other vicinage(s) in which he or she heard cases. Request for Extension to File Financial Reporting Statement – If a judge experiences a hardship that precludes the filing of the Financial Reporting Statement by April 15, up to a 60-day extension can be requested for good cause. The judge should complete the identifying information on the Statement, explain the reason for the extension request in Section IV and submit the form along with a written extension request to the judge’s Assignment Judge for consideration. Inquiries – Inquiries regarding the Judicial Financial Reporting Statement, the reporting requirements, or the filing of an amended Reporting Statement should be directed to the Advisory Committee on Judicial Financial Reporting at the following address: Helen E. Szabo, Esq., Secretary Advisory Committee on Judicial Financial Reporting Administrative Office of the Courts, P.O. Box 037 Trenton, New Jersey 08625-0037 Phone: 609-984-7150; Fax: 609-984-6968 Revised December 2004 9 REVISED FORM FOR 2004 REPORTING YEAR Judicial Financial Reporting Statement (pursuant to Rule 1:18B) (Applicable to Municipal Court Judges) ① Judge Reporting (last name, first name, middle initial) ④ Primary Chambers or Office Address ② Judge in Which Municipal Court(s) I. Earned Income in excess of $1000 (do not list actual amount) List name of source of earned income – Check (9) box of recipient ③ Vicinage/County Judge Spouse Child A. Salary 1. 2. 3. 4. 5. 6. B. Bonuses 1. 2. 3. C. Royalties 1. 2. D. Fees 1. 2. E. Commissions 1. 2. F. Profit Sharing 1. 2. G. Pensions 1. 2. Revised December 2004 Page 1 of 3 II. Unearned Income in excess of $1000 (do not list actual amount) List source of unearned income – Check (9) box of recipient A. Investment Income (dividends, capital gains, interest (other than interest on savings or checking accounts or on certificates of deposit), etc.) 1. Judge Joint Spouse Child Joint Spouse Child 2. 3. 4. 5. 6. 7. B. Rents (enter municipality and state where property is located and name of payor) 1. 2. 3. C. Trusts (enter name of trust, name of settlor of trust, name of trustee, and nature of trust) 1. 2. 3. D. Estates (enter name of estate, decedent, and executor or administrator ) 1. 2. 3. E. Gifts (enter name of person or entity giving gift) 1. 2. 3. III. Any Interest Held in Land or Building in Atlantic City Other Than Judge’s Residence (do not list actual value) List address of land or building – Check (9) box of person with interest Judge 1. 2. 3. Revised December 2004 Page 2 of 3 IV. Additional information or explanations (list all additional information or explanations here; indicate applicable box or section of Statement): V. Certification (Judge must personally sign; original signature required) I certify that all information provided above is accurate, true and complete to the best of my knowledge. Date: _________________________ Revised December 2004 Signature:______________________________________ Page 3 of 3