2QFY13 Earnings Plunge 73%")

Results Review, 13 August 2013

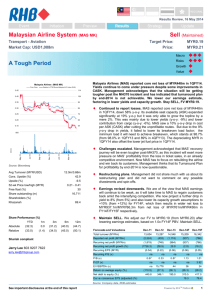

Electricity Generating (EGCO TB)

Neutral (Maintained)

Utilities - Electric

Market Cap: USD2,276m

Target Price:

Price:

THB142

THB135

Macro

2QFY13 Earnings Plunge 73%

Risks

Growth

Value

Electricity Generating (EGCO TB)

Relative to Stock Exchange of Thailand Index (RHS)

170

121

160

116

150

111

140

106

130

101

120

96

110

8

7

6

5

4

3

2

1

91

0

0

.

2

0

0

Egco’s 2QFY13 earnings plunged 73% y-o-y to THB1.8bn (24% y-o-y) .

0

after stripping out 2QFY12’s extraordinary gains. Earnings from BLCP 0

were stable, while contributions from Quezon Power rose (+36%) after 0

Egco increased its stake in the plant. It still has major catalysts: Quezon

Power’s expansion and the Khanom power plant (negotiations still

ongoing). Maintain NEUTRAL with a THB142 TP.

Jun-13

Apr-13

Feb-13

Dec-12

Oct-12

Aug-12

Vol m

Price Close

Source: Bloomberg

Avg Turnover (THB/USD)

Cons. Upside (%)

Upside (%)

52-wk Price low/high (THB)

Free float (%)

110m/3.58m

7.4

5.4

116 - 166

44

Shareholders (%)

EGAT

TEPDIA Generating BV

Thai NVDR

25.4

23.9

10.3

Shariah compliant

2

.

2

0

.

2

2QFY13 earnings plunged 73% y-o-y to THB1.8bn. This accounted for

63% of our FY13 forecast. After stripping out accounting gains of

THB4.3bn in 2QFY12, Egco’s earnings for the quarter would have fallen

by just 24% y-o-y. 2QFY13 sales surged 92% y-o-y to THB4.6bn, while

operating profit skyrocketed 340% y-o-y to THB1.2bn. The company’s yo-y net interest expense increased 187% to THB1.1bn, as it also included

a net forex loss of THB712m as well as THB38m in other finance costs.

Meanwhile, earnings from its associates declined 16% y-o-y to THB1.9bn

in 2QFY13, while tax expenses surged 227% y-o-y to THB287m.

Pre-forex earnings for its major power plants increased 4% y-o-y to

THB2bn. While BLCP power plant’s earnings were stable at THB534m,

net profit for Egco’s Quezon Power in the Philippines rose 36% y-o-y to

THB519m, as it boosted its stake from 45.87% to 98%. Meanwhile, Gulf

Power Generation’s earnings dropped 12% y-o-y to THB529m due to

lower electricity sales, while Nam Theun Power Company’s earnings fell

20% y-o-y, on the back of lower water levels. On a more positive note,

both Egco Cogeneration Ltd’s and Nong Khae Cogeneration Company’s

operations have normalised after suffering from disruptions last year.

Major catalyst. Egco aims to expand capacity at its Quezon Power plant

(the result of a 50:50 venture with the Manila Electric Company, which is

the sole off-taker) by another 500MW. The plant is expected to begin

commercial operations in 2017. Meanwhile, the 900MW Khanom project

is still under negotiations with the Electricity Generating Authority of

Thailand (Egat) as its sole off-taker. We expect the talks to be concluded

by year-end.

Forecasts and Valuations

Dec-11

Dec-12

Dec-13F

Dec-14F

Dec-15F

Total turnover (THBm)

7,661

14,057

18,865

18,875

15,565

Reported net profit (THBm)

4,990

10,979

6,421

6,504

4,418

Recurring net profit (THBm)

4,990

6,953

6,421

6,504

4,418

Recurring net profit growth (%)

(26.7)

39.4

(7.7)

1.3

(32.1)

9.5

13.2

12.2

12.4

8.4

5.25

6.00

5.25

5.25

5.25

Core EPS (THB)

DPS (THB)

Kannika Siamwalla, CFA 66 2862 9744

License No.23517

Dividend Yield (%)

kannika.si@th.oskgroup.com

Return on average equity (%)

Core P/E (x)

P/B (x)

P/CF (x)

EV/EBITDA (x)

Net debt to equity (%)

Our vs consensus EPS (%)

3.9

4.4

3.9

3.9

3.9

14.2

10.2

11.1

10.9

16.1

8.8

17.5

9.3

8.9

5.8

1.23

1.05

1.00

0.95

0.93

115

57

17

16

28

10.3

12.7

8.6

8.1

13.6

2.3

45.2

36.0

31.4

25.1

(8.3)

(1.9)

(33.4)

Source: Company data, RHB Estimates

See important disclosures at the end of this report

Powered by Enhanced Datasystems’ EFATM Platform

Electricity Generating (EGCO TB)

13 August 2013

Figure 1: 2Q13 earnings breakdown

FYE Dec. (THB m)

2Q13

2Q12

y-o-y

chg

YTD

2013

YTD

2012

y-oy

chg

Revenue

EBIT

Net interest expense

Associates

PBT

Tax

MI

Net profit

EPS (THB)

EBITDA margin (%)

4,610

1,245

(1,107)

1,987

117

(287)

18

1,835

3.49

40

2,404

283

(385)

2,365

115

(88)

6

6,710

12.74

27

92%

340%

187%

-16%

1%

227%

185%

-73%

-73%

48%

9,235

2,467

(956)

3,161

1,476

(582)

(11)

4,044

7.68

41

4,308

521

(412)

3,650

321

(109)

(14)

8,158

15.49

29

114%

374%

132%

-13%

360%

432%

-17%

-50%

-50%

43%

Source: RHB estimates

Figure 2: Major operating variables

Net profit before

forex (THB m)

%

y-o-y

2Q13

2Q12

KEGCO

-28

-39

(28)

Quezon

519

382

36

EGCO Cogen

GEC (GCC, NKCC,

SCC, GYG)

28

-50

N/A

78

36

117

GPG

529

604

(12)

BLCP

534

532

-

NTPC

245

307

(20)

Lower electricity sales

Lower electricity sales according to PPA,

with lower overall expenses.

Electricity sales was lower due to lower

water levels

Rayong

33

117

(72)

Increase in deferred tax

Conal

17

17

-

Other joint ventures

98

59

66

2053

1965

4

Net profit before forex

Comment

Availability payment (AP) and total

expenses increased

Increased stake in Quezon as of June

2012

Higher electricity sales this year from this

plant, as there was plant interruption in FebOct 2012

Higher electricity sales from NKCC, as the

plant was damaged in April-Sept 2012

Stable earnings

Source: RHB estimates

See important disclosures at the end of this report

2

Electricity Generating (EGCO TB)

13 August 2013

Financial Exhibits

Profit & Loss (THBm)

Dec-11

Dec-12

Dec-13F

Dec-14F

Total turnover

7,661

14,057

18,865

18,875

15,565

Cost of sales

(5,589)

(9,673)

(12,796)

(12,796)

(12,597)

Gross profit

Gen & admin expenses

Operating profit

Operating EBITDA

Depreciation of fixed assets

Operating EBIT

Dec-15F

2,072

4,384

6,069

6,079

2,967

(1,678)

(2,362)

(1,878)

(1,878)

(1,878)

1,089

394

2,022

4,190

4,200

2,367

4,833

6,961

6,971

3,859

(1,973)

(2,811)

(2,770)

(2,770)

(2,770)

394

2,022

4,190

4,200

1,089

5,200

5,578

4,136

4,156

4,156

Other recurring income

449

415

449

449

449

Interest income

-

-

90

104

Net income from investments

Interest expense

Exchange gains

Other non-recurring income

Pre-tax profit

(694)

22

154

(703)

(1,369)

(1,303)

(1,222)

-

205

-

-

-

4,310

-

-

-

5,371

11,826

7,497

7,607

4,626

Taxation

(255)

(779)

(1,008)

(1,035)

Minority interests

(126)

(68)

(68)

(68)

(141)

(68)

Profit after tax & minorities

4,990

10,979

6,421

6,504

4,418

Reported net profit

4,990

10,979

6,421

6,504

4,418

Recurring net profit

4,990

6,953

6,421

6,504

4,418

Dec-11

Dec-12

Dec-13F

Dec-14F

Dec-15F

394

2,022

4,190

4,200

1,089

1,973

2,811

2,770

2,770

2,770

Source: Company data, RHB Estimates

Cash flow (THBm)

Operating profit

Depreciation & amortisation

Change in working capital

Operating cash flow

Interest received

(799)

1,568

-

Interest paid

(694)

Tax paid

(255)

Cash flow from operations

Capex

Other investing cash flow

Cash flow from investing activities

Dividends paid

Proceeds from issue of shares

Increase in debt

(2,114)

2,719

-

(499)

6,462

90

6,557

104

(703)

(1,369)

(1,303)

(779)

(1,008)

(1,035)

4,175

4,323

619

1,236

339

(41,679)

(233)

15,441

106

(26,238)

3,212

(3,159)

(2,764)

(2,764)

(414)

(352)

3,564

(1)

315

314

(2,764)

(132)

3,727

154

(1,222)

(141)

2,518

4,224

4,224

(2,764)

933

1,635

-

-

-

2,497

23,832

(5,474)

(1,463)

(1,788)

Other financing cash flow

219

279

Cash flow from financing activities

884

22,587

(7,924)

(3,913)

(4,239)

4,148

3,611

4,334

723

2,504

Cash at beginning of period

7,748

8,402

Total cash generated

1,609

(2,414)

Forex effects

Implied cash at end of period

(22)

9,335

(205)

5,782

313

(537)

313

313

-

-

-

3,611

4,334

6,838

Source: Company data, RHB Estimates

See important disclosures at the end of this report

3

Electricity Generating (EGCO TB)

13 August 2013

Financial Exhibits

Balance Sheet (THBm)

Dec-11

Dec-12

Dec-13F

Dec-14F

Total cash and equivalents

10,685

5,026

4,489

5,212

7,716

6,884

10,015

10,015

10,015

10,015

Accounts receivable

Dec-15F

Other current assets

2,550

4,805

5,304

5,304

5,191

Total current assets

20,119

19,846

19,808

20,532

22,923

Total investments

39,685

39,232

37,709

41,619

41,619

Tangible fixed assets

13,023

49,912

49,017

46,246

43,476

129

334

974

975

975

Total non-current assets

52,837

89,478

87,699

88,840

86,069

Total assets

108,992

Total other assets

72,956

109,324

107,508

109,372

Short-term debt

536

11,724

1,251

4,788

-

Accounts payable

327

1,237

1,237

1,237

1,237

1,152

Other current liabilities

Total current liabilities

Total long-term debt

Other liabilities

853

1,811

1,811

1,397

1,716

14,772

4,298

7,422

2,389

11,521

24,165

29,165

24,165

27,165

1,186

2,067

2,067

2,067

2,067

Total non-current liabilities

12,707

26,232

31,232

26,232

29,232

Total liabilities

14,423

41,004

35,530

33,654

31,621

5,265

5,265

5,265

5,265

5,265

44,065

53,520

57,177

60,917

62,571

Share capital

Retained earnings reserve

Other reserves

8,649

8,649

8,649

8,649

8,649

57,978

67,433

71,090

74,831

76,484

555

887

887

887

887

0

0

0

0

0

Total equity

58,533

68,320

71,977

75,717

77,371

Total liabilities & equity

72,956

109,324

107,508

109,372

108,992

Shareholders' equity

Minority interests

Other equity

Source: Company data, RHB Estimates

Key Ratios (THB)

Dec-11

Dec-12

Dec-13F

Dec-14F

Dec-15F

Revenue growth (%)

(11.0)

83.5

34.2

0.1

(17.5)

Operating profit growth (%)

(73.7)

413.3

107.2

0.2

(74.1)

Net profit growth (%)

(26.7)

120.0

(41.5)

1.3

(32.1)

EPS growth (%)

(26.7)

120.0

(41.5)

1.3

(32.1)

Bv per share growth (%)

5.8

16.3

5.4

5.3

2.2

Operating margin (%)

5.1

14.4

22.2

22.3

7.0

Net profit margin (%)

65.1

78.1

34.0

34.5

28.4

Return on average assets (%)

7.1

12.0

5.9

6.0

4.0

Return on average equity (%)

8.8

17.5

9.3

8.9

5.8

Net debt to equity (%)

2.3

45.2

36.0

31.4

25.1

DPS

5.25

6.00

5.25

5.25

5.25

Recurrent cash flow per share

1.18

2.35

7.93

8.21

4.78

Source: Company data, RHB Estimates

See important disclosures at the end of this report

4

Electricity Generating (EGCO TB)

13 August 2013

SWOT Analysis

Has domestic expertise as well as strong connections

within the utilities industry via its major shareholder,

Egat

The domestic

utilities industry

operates in an

open market,

which allows for

new players to

enter the fray

Despite Egat’s 25% stake, Egco is allowed to operate

with the flexibility of an independent company

Actively seeking

investment

opportunities in

the domestic

and regional

markets

The power

sector is

enjoying steady

growth in

demand, which

will lead to more

solicitations for

IPPs in the

future

A conservatively-run company

P/E (x) vs EPS growth

P/BV (x) vs ROAE

14%

51%

0.80

11%

29%

0.60

6

7%

9%

4

-16%

0.40

6%

2

-38%

0.20

3%

0

-60%

0.00

0%

P/B (x) (lhs)

Jan-15

1.00

Jan-14

8

Source: Company data, RHB Estimates

17%

Jan-13

10

EPS growth (rhs)

20%

1.20

Jan-12

73%

P/E (x) (lhs)

1.40

Jan-11

12

Jan-15

96%

Jan-14

14

Jan-13

118%

Jan-12

140%

16

Jan-11

18

Return on average equity (rhs)

Source: Company data, RHB Estimates

Company Profile

Electricity Generating (Egco) was one of the first independent power producers to list on the SET, with Rayong Electricity Generating

Company Ltd and Khanom Electricity Generating Company Ltd as its main assets. The company currently has total of 5,275MW in

effective capacity.

See important disclosures at the end of this report

5

RHB Guide to Investment Ratings

Buy: Share price may exceed 10% over the next 12 months

Trading Buy: Share price may exceed 15% over the next 3 months, however longer-term outlook remains uncertain

Neutral: Share price may fall within the range of +/- 10% over the next 12 months

Take Profit: Target price has been attained. Look to accumulate at lower levels

Sell: Share price may fall by more than 10% over the next 12 months

Not Rated: Stock is not within regular research coverage

Disclosure & Disclaimer

All research is based on material compiled from data considered to be reliable at the time of writing, but RHB does not make any representation or

warranty, express or implied, as to its accuracy, completeness or correctness. No part of this report is to be construed as an offer or solicitation of an offer

to transact any securities or financial instruments whether referred to herein or otherwise. This report is general in nature and has been prepared for

information purposes only. It is intended for circulation to the clients of RHB and its related companies. Any recommendation contained in this report does

not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This report is for the

information of addressees only and is not to be taken in substitution for the exercise of judgment by addressees, who should obtain separate legal or

financial advice to independently evaluate the particular investments and strategies.

RHB, its affiliates and related companies, their respective directors, associates, connected parties and/or employees may own or have positions in

securities of the company(ies) covered in this research report or any securities related thereto, and may from time to time add to, or dispose off, or may be

materially interested in any such securities. Further, RHB, its affiliates and related companies do and seek to do business with the company(ies) covered

in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies),

may sell them or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory or

underwriting services for or relating to such company(ies), as well as solicit such investment, advisory or other services from any entity mentioned in this

research report.

RHB and its employees and/or agents do not accept any liability, be it directly, indirectly or consequential losses, loss of profits or damages that may arise

from any reliance based on this report or further communication given in relation to this report, including where such losses, loss of profits or damages are

alleged to have arisen due to the contents of such report or communication being perceived as defamatory in nature.

The term “RHB” shall denote where applicable, the relevant entity distributing the report in the particular jurisdiction mentioned specifically herein below

and shall refer to RHB Research Institute Sdn Bhd, its holding company, affiliates, subsidiaries and related companies.

All Rights Reserved. This report is for the use of intended recipients only and may not be reproduced, distributed or published for any purpose without prior

consent of RHB and RHB accepts no liability whatsoever for the actions of third parties in this respect.

Malaysia

This report is published and distributed in Malaysia by RHB Research Institute Sdn Bhd (233327-M), Level 11, Tower One, RHB Centre, Jalan Tun Razak,

50400 Kuala Lumpur, a wholly-owned subsidiary of RHB Investment Bank Berhad (RHBIB), which in turn is a wholly-owned subsidiary of RHB Capital

Berhad.

Singapore

This report is published and distributed in Singapore by DMG & Partners Research Pte Ltd (Reg. No. 200808705N), a wholly-owned subsidiary of DMG &

Partners Securities Pte Ltd, a joint venture between Deutsche Asia Pacific Holdings Pte Ltd (a subsidiary of Deutsche Bank Group) and OSK Investment

Bank Berhad, Malaysia which have since merged into RHB Investment Bank Berhad (the merged entity is referred to as “RHBIB”, which in turn is a whollyowned subsidiary of RHB Capital Berhad). DMG & Partners Securities Pte Ltd is a Member of the Singapore Exchange Securities Trading Limited. DMG &

Partners Securities Pte Ltd may have received compensation from the company covered in this report for its corporate finance or its dealing activities; this

report is therefore classified as a non-independent report.

As of 12 August 2013, DMG & Partners Securities Pte Ltd and its subsidiaries, including DMG & Partners Research Pte Ltd do not have proprietary

positions in the securities covered in this report, except for:

a)

As of 12 August 2013, none of the analysts who covered the securities in this report has an interest in such securities, except for:

a) Electricity Generating

Special Distribution by RHB

Where the research report is produced by an RHB entity (excluding DMG & Partners Research Pte Ltd) and distributed in Singapore, it is only distributed

to "Institutional Investors", "Expert Investors" or "Accredited Investors" as defined in the Securities and Futures Act, CAP. 289 of Singapore. If you are not

an "Institutional Investor", "Expert Investor" or "Accredited Investor", this research report is not intended for you and you should disregard this research

report in its entirety. In respect of any matters arising from, or in connection with this research report, you are to contact our Singapore Office, DMG &

Partners Securities Pte Ltd.

Hong Kong

This report is published and distributed in Hong Kong by RHB OSK Securities Hong Kong Limited (“RHBSHK”) (formerly known as OSK Securities Hong

Kong Limited), a subsidiary of OSK Investment Bank Berhad, Malaysia which have since merged into RHB Investment Bank Berhad (the merged entity is

referred to as “RHBIB”), which in turn is a wholly-owned subsidiary of RHB Capital Berhad.

RHBSHK, RHBIB and/or other affiliates may beneficially own a total of 1% or more of any class of common equity securities of the subject company.

RHBSHK, RHBIB and/or other affiliates may, within the past 12 months, have received compensation and/or within the next 3 months seek to obtain

compensation for investment banking services from the subject company.

6

Risk Disclosure Statements

The prices of securities fluctuate, sometimes dramatically. The price of a security may move up or down, and may become valueless. It is as likely that

losses will be incurred rather than profit made as a result of buying and selling securities. Past performance is not a guide to future performance. RHBSHK

does not maintain a predetermined schedule for publication of research and will not necessarily update this report

Indonesia

This report is published and distributed in Indonesia by PT RHB OSK Securities Indonesia (formerly known as PT OSK Nusadana Securities Indonesia), a

subsidiary of OSK Investment Bank Berhad, Malaysia, which have since merged into RHB Investment Bank Berhad, which in turn is a wholly-owned

subsidiary of RHB Capital Berhad.

Thailand

This report is published and distributed in Thailand by RHB OSK Securities (Thailand) PCL (formerly known as OSK Securities (Thailand) PCL), a

subsidiary of OSK Investment Bank Berhad, Malaysia, which have since merged into RHB Investment Bank Berhad, which in turn is a wholly-owned

subsidiary of RHB Capital Berhad.

Other Jurisdictions

In any other jurisdictions, this report is intended to be distributed to qualified, accredited and professional investors, in compliance with the law and

regulations of the jurisdictions.

DMG & Partners Research Guide to Investment Ratings

Kuala Lumpur

Hong Kong

Singapore

Malaysia

Tel : +(60) 3 9280 2185

Fax : +(60) 3 9284 8693

Central, Hong Kong

Tel : +(852) 2525 1118

Fax : +(852) 2810 0908

Tel : +(65) 6533 1818

Fax : +(65) 6532 6211

Jakarta

Shanghai

Phnom Penh

Buy: Share price may exceed 10% over the next 12 months

Trading Buy:Malaysia

Share price

may exceed 15% over the next 3 RHB

months,

however longer-term outlook remains uncertain

Research Office

OSK Securities Hong Kong Ltd.

DMG & Partners

Neutral: Share

mayInstitute

fall within

over known

the next

months

(formerly

as 12

OSK

Securities Hong Kong Ltd.)

Securities Pte. Ltd.

RHB price

Research

Sdn the

Bhdrange of +/- 10%

Take Profit:

Target

price

has

been

attained.

Look

to

accumulate

at

lower

levels

Level 11, Tower One, RHB Centre

12th Floor

10 Collyer Quay

Sell: Share price may

more than 10% over the next 12 monthsWorld-Wide House

Jalanfall

TunbyRazak

#09-08 Ocean Financial Centre

Lumpur

19 Des Voeux Road

Singapore 049315

Not Rated: Stock isKuala

not within

regular research coverage

DISCLAIMERS

This research is issued by DMG & Partners Research Pte Ltd and it is for general distribution only. It does not have any regard to the specific investment

objectives,PTfinancial

situation

andIndonesia

particular needs of any

specific

recipient

of this research

report.

You should independently

evaluate

particular

RHB OSK

Securities

RHB

OSK (China)

Investment

Advisory

Co. Ltd.

RHB OSK Indochina

Securities

Limited

(formerly known

as PT OSK

Nusadana Securities

known as

OSK

(China) Investment

(formerly

known as in

OSK

Indochina

Securities

Limited)

investments

and consult

an independent

financial adviser(formerly

before making

any

investments

or entering into

any transaction

relation

to any

securities

or

Indonesia)

Advisory Co. Ltd.)

No. 1-3, Street 271

investment instruments

mentioned in this report.

Plaza CIMB Niaga

14th Floor

Suite 4005, CITIC Square

1168 Nanjing West Road

Fax : +(6221) 2598 6777

Fax : +(8621) 6288 9633

Sangkat Toeuk Thla, Khan Sen Sok

Phnom Penh

The information

contained herein has been obtained from sources we believed

to be reliable but we do not make any representation

or warranty nor

Jl. Jend. Sudirman Kav.25

Shanghai 20041

Cambodia

accept anyJakarta

responsibility

or liability

as to its accuracy, completeness or correctness.

Opinions and views expressed in this

subject

Selatan 12920,

Indonesia

China

Tel:report

+(855) are

23 969

161 to change

without notice. Tel : +(6221) 2598 6888

Tel : +(8621) 6288 9611

Fax: +(855) 23 969 171

This report does not constitute or form part of any offer or solicitation of any

offer to buy or sell any securities.

Bangkok

DMG & Partners Research Pte Ltd is a wholly-owned subsidiary of DMG & Partners Securities Pte Ltd, a joint venture between OSK Investment Bank

RHB OSK Securities (Thailand) PCL

Berhad, Malaysia which have since merged into RHB(formerly

Investment

Bank Berhad (the merged entity is referred to as “RHBIB” which in turn is a whollyknown as OSK Securities (Thailand) PCL)

owned subsidiary of RHB Capital Berhad) and Deutsche Asia

Pacific

Pte Ltd

(a subsidiary

of Deutsche Bank Group). DMG & Partners Securities

10th

Floor, Holdings

Sathorn Square

Office

Tower

Pte Ltd is a Member of the Singapore Exchange Securities Trading

Limited.

98, North

Sathorn Road, Silom

Bangrak, Bangkok 10500

DMG & Partners Securities Pte Ltd and their associates, directors, and/or Thailand

employees may have positions in, and may effect transactions in the securities

Tel:and

+(66)

862 9999

covered in the report, and may also perform or seek to perform broking

other

corporate finance related services for the corporations whose securities

Fax : +(66) 108 report.

0999

are covered in the report. This report is therefore classified as a non-independent

As of 12 August 2013, DMG & Partners Securities Pte Ltd and its subsidiaries, including DMG & Partners Research Pte Ltd, do not have proprietary

positions in the subject companies, except for:

a)

As of 12 August 2013, none of the analysts who covered the stock in this report has an interest in the subject companies covered in this report, except for:

a) Electricity Generating

DMG & Partners Research Pte. Ltd. (Reg. No. 200808705N)

7

Thai Institute of Directors Association (IOD) – Corporate Governance Report Rating 2012

ADVANC

AOT

ASIMAR

BAFS

BANPU

BAY

BBL

BCP

BECL

BKI

BMCL

BTS

CPN

CSL

DRT

EASTW

EGCO

ERW

GRAMMY

HEMRAJ

ICC

IRPC

KBANK

KK

KTB

LPN

MCOT

NKI

NOBLE

PHOL

PS

PSL

PTT

PTTEP

PTTGC

QH

RATCH

ROBINS

RS

SAMART

SAMTEL

SAT

SC

SCB

SCC

SE-ED

SIM

SIS

SNC

SYMC

THAI

TIP

TIPCO

TISCO

TKT

TMB

TOP

TSTE

TTA

2S

ACAP

AF

AIT

AKR

AMATA

AP

ASK

ASP

AYUD

BEC

BFIT

BH

BIGC

BJC

BROOK

BWG

CENTEL

CFRESH

CGS

CHOW

CIMBT

CK

CM

CPALL

CPF

CSC

DCC

DELTA

DEMCO

DTAC

DTC

ECL

EE

EIC

ESSO

FE

FORTH

GBX

GC

GFPT

GL

GLOW

GUNKUL

HANA

HMPRO

HTC

IFEC

INTUCH

ITD

IVL

JAS

KCE

KGI

KSL

L&E

LANNA

LH

LRH

LST

MACO

MAKRO

MBK

MBKET

MFC

MFEC

MINT

MODERN

MTI

NBC

NCH

NINE

NMG

NSI

OCC

OFM

OGC

OSIHI

PAP

PDI

PE

PG

PHATRA***

PJW

PM

PR

PRANDA

PRG

PT

PYLON

S&J

S&P

SABINA

SAMCO

SCCC

SCG

SCSMG

SFP

SITHAI

SMT

SPALI

SPCG

SPI

SPPT

SSF

SSSC

STANLY

STEC

SUC

SUSCO

SVI

SYNTEC

TASCO

TCAP

TCP

TFD

TFI

THANA

THCOM

THIP

THRE

TIC

TICON

TIW

TK

TLUXE

TMT

TNITY

TNL

TOG

TPC

TRC

TRT

TRU

TRUE

TSC

TSTH

TTW

TUF

TVO

UAC

UMI

UP

UPOIC

UV

VIBHA

VNT

WACOAL

YUASA

ZMICO

*** PHATRA was voluntarily delisted from the Stock Exchange of Thailand effectively on September 25, 2012.

AEONTS

AFC

AGE

AH

AHC

AI

AJ

ALUCON

AMANAH

APCO

APCS

APRINT

ARIP

AS

ASIA

BGT

BLA

BNC

BOL

BROCK

BSBM

BTNC

BUI

CCET

CEN

CHUO

CI

CIG

CIMBI***

CITY

CMO

CNS

CNT

CPL

CRANE

CSP

CSR

CTW

DRACO

EASON

EMC

EPCO

FNS

FOCUS

FSS

GENCO

GFM

GLOBAL

GOLD

HFT

HTECH

HYDRO

IFS

IHL

ILINK

INET

IRC

IRCP

IT

JMART

JTS

JUBILE

JUTHA

KASET

KBS

KC

KDH

KIAT

KKC

KTC

KWC

KWH

KYE

LALIN

LEE

LHBANK

LHK

LIVE

LOXLEY

MAJOR

MATCH

MATI

MBAX

M-CHAI

MDX

MJD

MK

MOONG

MPIC

MSC

NC

NNCL

NTV

OSK

PAE

PATO

PB

PICO

PL

POST

PPM

PREB

PRECHA

PRIN

PSAAP

PTL

Q-CON

QLT

QTC

RASA

RCL

RICH

ROJNA

RPC

SAM

SCBLIF

SCP

SEAFCO

SENA

SF

SGP

SIAM

SIMAT

SINGER

SIRI

SKR

SMIT

SMK

SOLAR

SPC

SPG

SSC

SST

STA

SVOA

SWC

SYNEX

TBSP

TCB

TEAM

TF

TGCI

THANI

TKS

TMD

TMI

TNH

TNPC

TOPP

TPA

TPAC

TPCORP

TPIPL

TPP

TR

TTCL

TWFP

TYCN

UBIS

UEC

UIC

UMS

UOBKH

UPF

US

UT

VARO

WAVE

WG

WIN

WORK

*** CIMBI was voluntarily delisted from the Stock Exchange of Thailand effectively on September 25, 2012.

IOD (IOD Disclaimer)

การเปิดเผลผลการสารวจของสมาคมส่งเสริมสถาบันกรรมการบริษัทไทย (IOD) ในเรื่องการกากับดูแลกิจการ (Corporate Governance) นี้เป็นการ

ดาเนินการตามนโยบายของสานักงานคณะกรรมการกากับหลักทรัพย์และตลาดหลักทรัพย์ โดยการสารวจของ IOD เป็นการสารวจและประเมินจากข้อมูลของบรษัทจด

ทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทยและตลาดหลักทรัพย์เอ็มเอไอ ที่มีการเปิดเผยต่อสาธารณะและเป็นข้อมูลที่ผลู้ งทุนทั่วไปสามารถเข้าถึงได้ ดังนั้นผลสารวจ

ดังกล่าวจึงเป็นการนาเสนอในมุมมองของบุคคลภายนอกโดยไม่ได้เป็นการประเมินการปฏิบัติและมิได้มีการใช้ข้อมูลภายในในการประเมิน

อนึ่ง ผลการสารวจดังกล่าว เป็นผลการสารวจ ณ วันที่ปรากฎในรายงานการกากับดูและกิจการบริษัทจดทะเบียนไทยเท่านั้น ดังนั้นผลการสารวจจึงอาจ

เปลี่ยนแปลงได้ภายหลังวันดังกล่าว ทัง้ นี้บริษัทหลักทรัพย์ อาร์เอสบี โอเอส เค จากัด (มหาชน) มิได้ยืนยันหรือรับรองถึงความถูกต้องของผลการสารวจดังกล่าวแต่อย่างใด

2QFY13 Earnings Plunge 73%")