Fringe Benefits Tax Information

advertisement

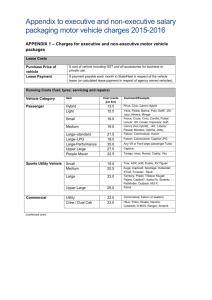

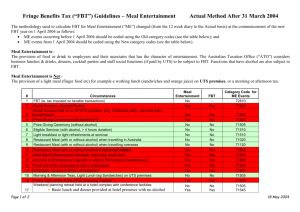

FBT Background Fringe Benefits Tax (FBT) was introduced in 1986 by the Federal Government to tax the value of benefits provided by employers to employees and their associates (3rd parties) on benefits which are provided in place of, or in addition to, the employees "cash" salary. Motor vehicles remain one of the most popular and beneficial salary packaging options available. The success and high demand for motor vehicle salary packaging can be attributed to the fact that motor vehicles enjoy concessional FBT treatment. The information below is provided as a guide only. SupaNova is not responsible for the accuracy of the information provided. SupaNova strongly recommends that you and your employer seek your own independent tax advice in relation to any Vehicle FBT issue. Please refer to the Australian Taxation Office website (www.ato.gov.au) for the latest information regarding Vehicle Fringe Benefits Tax. The FBT Year The FBT year is from 1 April to 31 March, inclusive. Motor Vehicles and FBT A motor vehicle fringe benefit arises when a motor vehicle is made available for the use of an employee or an associate of the employee for private use. Such an arrangement exists with the Novated Lease facility where the employee Novates ("sub-leases") the vehicle to their employer and generally has unrestricted access to the vehicle for private travel. Under a Novated Lease there is no requirement to use the vehicle for business related travel and no need to retain a log book to document your travel. The FBT is simply based on the total amount of kilometres the vehicle travelled during the full FBT year. Under a Novated Lease arrangement the employer usually charges the FBT to the employee's salary package. The FBT is collected by the employer who subsequently attends to remitting the monies as required to the ATO. Methods for calculating FBT There are two methods in common use for determining the applicable FBT to a Novated Lease. These are commonly referred to as the Statutory Fraction Method or the Employee Contribution Method: 1) Novated Lease using the Statutory Fraction Method This method determines the amount of FBT payable on a motor vehicle based solely on the total number of kilometres travelled each FBT year, regardless as to the level of business or private use involved in this travel. The Taxable Value on a vehicle under the Statutory Fraction Method is calculated by the following formula: (A x B x C) - E Taxable Value = --------------D Where; A = the capital cost of the car B = the statutory fraction C = the number of days in the FBT year when the car was used or available for private use of employees D = the number of days in the FBT year E = the employee contribution (where applicable) The taxable value is then multiplied by the Gross up Factor (currently 2.064662) and again by the Fringe Benefit Tax Rate (of 46.5%) to determine the total fringe benefits tax payable on the vehicle. Determining the capital cost of the car The Capital Cost of a car is the original purchase price (GST inclusive) + fitted accessories + dealer delivery charges (GST inclusive). Registration and stamp duty charges are not included in the capital cost of the vehicle. Determining the Statutory Fraction The statutory fraction for the FBT year is determined by assigning the total kilometres travelled during the FBT year (or annualised kilometres if the car is only held for part of an FBT year) to the appropriate annual kilometre bracket: Total kilometres travelled during the FBT year Statutory fraction Distance travelled during the FBT year Prior 10 From 10 From 1 From 1 From 1 May 2011 May 2011 April 2012 April 2013 April 2014 (1 April to 31 March) 0 – 14,999km 26 % 20 % 20 % 20 % 20 % 15,000 – 24,999km 20 % 20 % 20 % 20 % 20 % 25,000 – 40,000km 11 % 14 % 17 % 20 % 20 % More than 40,000km 7% 10 % 13 % 17 % 20 % 2) Novated Lease using the Post Tax Contribution Method (Employee Contribution Method) The Contribution Method is well established in tax law and allows an employee to make a contribution towards the running costs of their motor vehicle from their After Tax (Net) Salary. Note: Not all companies offer the Contribution Method as a Salary Packaging option to employees. Please confirm availability with your company representative. The ATO allows the Taxable Value to be reduced by every after tax dollar that an employee contributes towards the running cost of their vehicle. This can negate the FBT liability required to be submitted to the ATO. In practice, this means that, as a substitute for FBT, an after tax contribution may be paid by an employee up to the amount of FBT Taxable Value that would have been required under the Statutory Fraction Method. The underlying fundamental here is that the personal tax the employee pays on the Post-Tax contribution may work out to be cheaper than paying the FBT, which is "Grossed-up" at 46.5%, representing the top tax bracket + Medicare levy. For example: An employee is driving a $30,000 vehicle 20,000 kms p.a. (FBT rate = 20% for this level of travel). The employee may contribute $6,000 p.a. ($30,000 X 20%) toward the running costs of the vehicle and completely remove the F.B.T. that would otherwise have been payable. The employee would still Salary Sacrifice the balance of running costs and lease payments from their pre tax salary without any additional F.B.T. being incurred. Calculations show that the benefits provided by using the Contribution Method will be an improvement on the existing arrangements (Statutory Fraction) for many employees, particularly those whose salaries are under or close to the top marginal tax rate. Choosing the Statutory Fraction or Contribution Method The statutory formula method must be used unless the employer elects to use the contribution method. The employer may elect to use the contribution method for any or all of the employer's cars and the fact that a particular method was used in a previous year does not affect the choice of methods in subsequent years. There is no need to notify the Tax Office of the method chosen; the employer's business records are sufficient evidence of this. Your Account Manager is best suited to provide you with information and budgets based on both methods. It is recommended you provide this information to your independent financial advisor or Accountant and they will make an informed decision as to which method will suit your individual circumstances. You may also access our package calculators contained within SupaNova’s Internet Websites to calculate your own scenario prior to contacting your Account Manager. SupaNova is happy to supply the information to make this decision but we are not in a position to recommend nor select which method is best for you. Estimating Annual Kilometres Estimating your annual kilometres is an extremely important exercise and should be given due consideration to avoid an unexpected additional expense at the end of the FBT year. It is important to read the information contained within this document under the headings "How FBT is treated if you Novated the car for part of the FBT year" and "Here is a comprehensive explanation of calculating annualised kilometres". If your actual annual (or annualised) kilometres place you into a different Statutory Percentage bracket than the one you budgeted for then there will be a variation in the amount of FBT you have to pay at the end of the FBT year. Eg: If an employee with a vehicle that has a capital cost of $30,000 budgets they will travel 26,000 kilometres per FBT year (25,000 to 39,999 km is the 11% Statutory Fraction), we have budgeted for an FBT bill of; $30,000 x 11% x 2.064662 x 46.5% = estimated FBT liability of $3,168. If the employee actually travel 24,000 kilometres per FBT year (15,000 to 24,999 km is the 20% Statutory Fraction), the result is; $30,000 x 20% x 2.064662 x 46.5% = actual FBT payable of $5,760.41. Based on this scenario the employee has under-budgeted their FBT liability by $2,592.41. The employer may request that the employee to repay this shortfall. This would have a significant impact on the employee's take home pay. To avoid the same situation re-occurring for the next FBT year we strongly recommend that the novation arrangement be revised. Unless you are 100% certain of meeting a kilometre target it is best to be conservative. Based on the above example, if your annual (FBT year) travel is around the 25,000 kilometres, but you are not 100% certain you will travel 25,000 kilometres or greater, it is recommended you estimate 24,000 kilometres. This way your salary deductions will be based on 20% Statutory Fraction so if you fall short of travelling 25,000 kilometres during the FBT year you will still have the correct amount of FBT deducted from your salary. On the other hand, if your are successful in travelling 25,000 kilometres or greater you will have surplus FBT money in your fund as you will only need to pay FBT based on the 11% Statutory Fraction. Remember that variances in kilometres not only affect your FBT liability, they also have an effect on increased or decreased running costs such as fuel, maintenance and tyres and could also impact on the re-sale price of the vehicle at the end of the lease. When does the FBT capital cost reduce? Safeguards have been built into ATO legislation to ensure that the true base value of a car cannot be artificially reduced in order to minimise ones FBT liability. They also apply where a leased car is re-leased on termination of the lease. Under ATO legislation, the base value is determined at the time the car was first held by the employer or an associate and according to whether, at the time, it was owned or leased. This means that once a vehicle is under a Novated Lease, the capital cost will remain the same until the car passes through 4 FULL FBT years. On the anniversary of the 4th FULL FBT year, the capital cost may be reduced to 66.6% of the original capital cost. The capital cost ruling is in no way tied to the lease term, it is solely linked to number of FULL FBT years over which the car was held by the employer (under a Novated Lease the vehicle is deemed to be held by the employer). An example is an employee who purchases a vehicle (either new or second hand) with a capital cost of $43,000. They take a 2 year lease and at the end of the 2 year lease they wish to re-lease the vehicle (ie take out a new 2 year Novated Lease on the same vehicle). As the vehicle has not been held for 4 FULL FBT years, the capital cost will still be $43,000 for this new 2 year lease, even though the car's present value and the new lease value would both be less than $43,000. Another example: An employee purchases a company car, which the company has only held for 2 years. The employee purchases this vehicle under a Novated Lease arrangement. The capital cost for the employee's novated lease is the original capital cost that applied when the company first "held" the vehicle, not the purchase price when the employee purchases the vehicle from their employer. Upon the anniversary of the 4th full FBT year from the time the vehicle was originally "held" by the employer, the employee will be entitled to reduce the capital cost to 66.6%. In another example, an employee has a Novated Lease on a vehicle that has been Novated for 2 years. They sell the vehicle to a fellow employee (of the same company). The employee purchasing the vehicle will pay FBT based on the original capital cost at the time the seller originally novated the car as this is deemed the earliest date that the employer "held" the vehicle. On the anniversary of the 4th full FBT year since the seller originally novated the vehicle, the capital cost will reduce to 66.6% for the new owner. Days Unavailable For Private Use Days unavailable for private use are audited by the Australian Taxation Office (ATO) and employees must always ensure they are acting within the ATO and employer's guidelines when claiming unavailable days. If after reading this information you are uncertain as to whether you are entitled to claim an unavailable day you must always discuss your situation with your employer or your tax advisor. The FBT payable on a Novated Lease vehicle may be reduced where the vehicle has not been made available for use by an employee for any full 24 hour period of any day during the FBT year, subject to complying with the stringent ATO guidelines covering the treatment of Days Unavailable For Private Use. To claim Days Unavailable For Private Use, your employer must have records to verify to the ATO that the car has NOT been made available for private use either of an employee or their associates for a certain period of time during the FBT year. The vehicle must be securely stored at the employer's premises, the keys must be handed to the employer, their must be strict procedures prohibiting use of the vehicle and a log must be maintained by the employer recording the time and date the vehicle was dropped off and the time and date the vehicle was collected. If your vehicle is stored somewhere other than your employer's premises you must contact your employer to determine whether or not you may claim unavailable days. There are strict criteria governing this situation and more often than not you will be unable to claim unavailable days unless there is a specific arrangement between the employer and the storage facility to satisfy the ATO requirements. For example if you leave your vehicle at the Airport whilst attending business travel you will only be able to claim unavailable days if your employer and the Airport parking station have an arrangement whereby the Airport attendants will carry out the required procedure to allow the employer to claim the unavailable days. It is not sufficient to simply park your car there then claim unavailable days without prior approval from your employer. Vehicles undergoing ordinary servicing requirements fall outside of this Taxation Determination and can not be claimed as unavailable days. Vehicles undergoing voluntary panel or paint work can generally not be claimed. If in doubt, ask your employer or taxation advisor. How Days Unavailable For Private Use effect your FBT Calculation. It is very important to understand that Days Unavailable For Private Use do not have any impact in determining the number of kilometres travelled by a vehicle in the FBT year. The formula for determining the number of kms travelled in the FBT year is as follows: A x C ----B Where: A = the number of kilometres travelled in the period during the year when the car was owned or leased by the employer. (All the days even if Days Unavailable For Private Use claimed!) B = the number of days in that period C = the number of days in the FBT year The result of this equation is then compared to the Statutory Fraction matrix to determine the Statutory Fraction to be used for the vehicle. Example: An employee collects their vehicle on September 30, 2001 and during the next 6 months (212 days) travels 12,500 kms. During this time the vehicle accumulates 30 Days Unavailable For Private Use while the driver is overseas and the vehicle is held at the company premises. The equation to determine the number of Kms travelled in the year is; 12,500 X 365 ------------ = 21,521 p.a. 212 The Statutory Fraction applicable to the above kilometre reading would be 20.00%. You will note that the 30 Days Unavailable For Private Use have no bearing on this equation as they do not reduce the number of days in the period. Once you have established what the correct Statutory Fraction is then this figure is incorporated into the FBT equation as follows: (A x B x C) - E Taxable Value = --------------D Where; A = the capital cost of the car B = the statutory fraction C = the number of days in the FBT year when the car was used or available for private use of employees D = the number of days in the FBT year E = the employee contribution (where applicable) The taxable value is then multiplied by 2.064662 and again by 0.465 to determine the total fringe benefits tax payable on the vehicle. An example of how Days Unavailable For Private Use works; The employee's vehicle is left at the employer's premises at 10am Monday 31/7/2000. The vehicle is logged in and the keys are handed to the employer. The employee returns from their trip and collects the vehicle at 8pm Tuesday 1/8/2000 and the vehicle has not been used during this period. The employee can not claim unavailable days as the car was not unavailable for a full 24 hours on either day. The car was only unavailable for part of Monday and part of Tuesday If the vehicle were picked up at noon on Wednesday 2/8/2000 the employee would be able to claim 1 unavailable day, being Tuesday 1/8/2000 as the car was unavailable for the entire 24 hours of that day (Midnight to Midnight). How FBT is treated if you Novated the car for part of the FBT year If you enter into a new salary packaging arrangement part way through the FBT year, you are not required to travel your nominated annual kilometres from the 1st day of packaging to the end of that FBT year for the purpose of establishing your Statutory Fraction. In fairness to the employee, the amount of kilometres travelled over the time the vehicle was packaged during the partial FBT year are annualised in order to estimate how many kilometres the driver would have travelled if they had the car for the full FBT year. To calculate annualised kilometres, the average kilometres travelled per day must be determined, then multiplied by the number of days in the FBT year. For example, where a car is acquired exactly halfway through the FBT year, and then travels 12,000 kilometres up the end of that FBT year, this would give annualised kilometres of 24,000 and the Statutory Fraction would be the one applicable for 24,000 kilometres not 12,000 kilometres. Here is a comprehensive explanation of calculating annualised kilometres; Starting odometer reading, minus; Odometer reading at the end of FBT year = *Actual Kilometres Travelled to date The number of days from when you 1st packaged the vehicle to the end of the FBT year = **Days vehicle held to date Actual Kilometres Travelled to date, divided by; Days vehicle held to date = ***Average daily kilometres Average Daily Kilometres, multiplied by the number of days in the FBT year = ****Annualised Kilometres. Here are 2 examples; A new car was packaged on the 20th of June and had 0 kilometres on day 1. As at 31 March the following year (end of FBT year) the car travelled 23,000 Kilometres* From the 20th of June to the 31st of March there are 286 days (inclusive)** 23,000 kilometres / 286 days = Average Daily Kilometres of 80.42 per day*** 80.42 x 365 = Annualised Kilometres 29,353.**** In this example the driver's annualised kilometres were 29.353, therefore their Statutory Fraction is 11%. The 11% Statutory Fraction is used to calculate the annual FBT liability. This amount is then pro-rata so that the driver only pays an amount proportionate to 286 days. Therefore if the capital cost of the vehicle was $20,000, the formula for calculating the FBT is; $30,000 x 11% X 46.5% x 2.064662 = $3,168.22 (This is the FBT for 365 days) Because the car was only held for 286 days we pro-rata the cost as follows; $3,407.76 / 365 x 286 = $2,485.50 (This is the actual pro-rata payable) Note: If an employee changes vehicles part way through an FBT year the above procedure applies for both the vehicle exiting packaging and the vehicle entering packaging. Each vehicles FBT liability is pro-rata. ie you do not add the kilometres travelled in the old car to the kilometres travelled in the new car. Bearing the above in mind, if the employee has substantial seasonal variances in travel, they may be paying different Statutory Fractions for each vehicle over their respective part periods of the FBT year that they were packaged. For example, an employee changes their vehicle exactly half way through the FBT year; The car being sold travelled 12,000 kilometres over the 6 months it was novated. This annualises to 24,000 kilometres therefore its Statutory Fraction is 20%. The new car ends up travelling 14,000 kilometres over the 6 months to the end of the 2nd half of the FBT year. This annualises to 28,000 kilometres therefore its Statutory Fraction is 11%. A common misunderstanding is the assumption that we add the 2 figures together for both cars (which equals 26,000 kilometres) and apply the 11% Statutory Fraction to each car. Fringe Benefits Tax and your Group Certificate From 1 April 2006, employers subject to FBT are required to record the grossed-up taxable value of fringe benefits on the group certificate or payment summary of any employee who receives relevant benefits with a total taxable value exceeding $2000. A similar requirement applies to some employers who provide benefits which are exempt from FBT. Car benefits arising from occasional travel to a major population centre by employees, and their families, living in a remote area are excluded from these reporting requirements. Odometer records Odometer records are a record of the total kilometres travelled by the car during the FBT year, they are captured by SupaNova each time you purchase fuel or your vehicle is serviced. Without accurate odometer readings the SupaNova reporting will be rendered useless and as such the employee may miss their nominated Statutory Fraction bracket and not know until the end of the FBT year. The Tax Office does not produce an official odometer record form, SupaNova provide employees with an odometer reading declaration form to complete and return at the end of each FBT year. This document is audited by the ATO and employees and employers are liable for any consequence arising from the incorrect completion of this form.