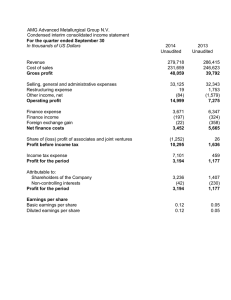

Consolidated financial statements

advertisement