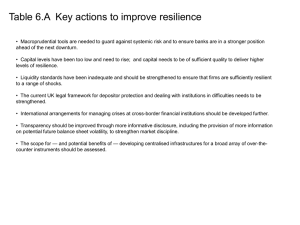

Market value puts Tier 2 banks ahead of peers

advertisement

Market value puts Tier 2 banks ahead of peers Contrary to the popular belief that the banking industry is dominated by the big four - First Bank, GT Bank, UBA and Zenith Bank - which are considered to be in the tier one or industry leaders, market sentiments, particularly in the post-banking reforms seem to favour the tier two banks, comprising, Access Bank, Diamond Bank, FCMB and Skye bank, based on some indices, according to Renaissance Capital (Rencap). Tier one capital is the core measure of a bank’s financial strength from a regulator’s point of view. It is composed of core capital, consisting primarily of common stock and disclosed reserves (or retained earnings). It may also include non-redeemable non-cumulative preferred stocks. The essence is its ability to provide protection against unexpected losses. The tier one capital ratio is the ratio of a bank’s core equity capital to its total assets, while the tier two risk based capital ratio on the other hand is the ratio of a bank’s core (equity capital) to its total risk-weighted assets. Risk-weighted assets are the total of all assets held by the bank which are weighted for credit risk, according to a formula determined by the CBN. The analysts had in October last year on who will be industry leaders said that “post audit, we expect Guaranty Trust Bank, First Bank , UBA and Zenith Bank (the big four) to emerge as clear system leaders with a collective equity share of 54 percent against 35 percent pre-audit. With a 35 percent asset share post–audit, we estimate these banks could add 19 points to their asset market shares over the next couple of years, all other things remaining constant.” They also observed that rather than follow the big four, tier two banks, such as Access, Fidelity, Diamond, FCMB, Skye and Stanbic IBTC, “will take advantage of the current market environment to buy scale and position their businesses for leadership status.” Specifically, the analysts in an industry update, released to BusinessDay posited that the big four banks currently trade at an estimate of about two times higher than its market price, which is price to-book ratio (P/B). This, according to them, represents 66 percent premium to the tier two banks which on the other hand, are currently trading below their current prices by 0.88 times. P/B ratios are commonly used to compare banks, because most assets and liabilities of banks are constantly valued at market values. A higher P/B ratio implies that investors expect management to create more value from a given set of assets, all else equal (and/or that the market value of the firm’s assets is significantly higher than their accounting value). The ratios also give some idea of whether an investor is paying too much for what would be left if the company went bankrupt immediately. Interestingly, the analysts also said that the 2011 Return on Average Equity (ROAE) of the big four currently at 29 percent, “does not differ materially from that of the tier two banks (23 percent) on our estimates.” Return on Average Equity shows a company’s performance over a fiscal year. It can give a more accurate depiction of a company’s corporate profitability, especially in instances where the value of the shareholders’ equity has changed considerably during a fiscal year. Interestingly, the share prices of the big four as at Wednesday stood at First Bank 13.15; GT Bank,16.90; UBA 10.50 and Zenith 13.00 with tier two at Access Bank 7.99; Diamond Bank 7.61; FCMB 7.68 and Skye bank 8.25. The analysts said that the premium of the big four banks is being exaggerated, adding that the valuation gap between the big four banks and the tier two counterparts can primarily be explained through liquidity. They further observed that the tier two banks are currently trading at $0.7 million a day, on average, down from $1.5 million in 2008. However, they said that as average daily volumes have fallen 51 percent since 2008, tier two bank valuations have fallen 49 percent over the same period. The resort to playing value now, according to the analysts, is as a result of the fact that liquidity levels at the stock exchange will continue to improve over the second half of this year based on, among others, lower rates, higher average oil prices and production, resilient depositor growth and regulatory clarity. They observed with interest the fact that liquidity levels of the tier two banks have been improving and trading around $1.2 million a day, adding “as more tier two banks begin to trade over $1 million a day, we believe their re-rating will gather momentum.” Consequently, the analysts said that taking a critical look at the stocks of all the banks that passed the Central Bank of Nigeria (CBN)’s audit test, opportunities abound in the sector. “This opportunity favours the four tier two banks which are trading at significant discount to the sector’s big four banks. The tier two banks are trading at 40 percent to the big four banks despite their weighted average 2011E RoAE being only seven percentage points over (23 percent against 29 percent).” “Although we are very positive on our universe of investible banking stocks, we do not believe that the current valuation gap between the big four and tier two banks is sustainable. We say this because we believe that the current valuation gaps in the sector are driven primarily by liquidity and not operating performance,” they said." JOHN OMACHONU BUSINESSDAY June 11, 2010