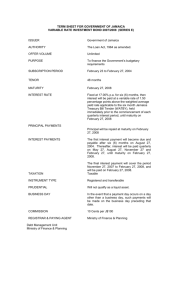

A Lattice Method for Computing the Probability Distribution of the

advertisement

The Distribution of the Value of the Firm and

Stochastic Interest Rates: An Application to Structural

Models of Default Risk

by

S. Lakshmivarahan1, Shengguang Qian1 and Duane Stock2

December 2, 2007

1) School of Computer Science, University of Oklahoma, Norman, OK 73019

2) Division of Finance, Michael F. Price College of Business, University of Oklahoma,

Norman, OK 73019. Contact Author: Duane Stock, email: dstock@ou.edu

1

Abstract

The time evolution of the value of a firm is commonly modeled by the linear, scalar

stochastic differential equation (SDE) of the type d Vt = rV

t t d t + s v ( t )Vt d Wv where the

coefficient rt in the drift term denotes the (exogenous) stochastic short term interest rate

and s v ( t ) is the given volatility of the value process. In turn, the dynamics of the short

term interest rate, d rt , are modeled by a scalar SDE. We solve this pair of equations for a

variety of commonly used interest rate processes which in turn provide explicit expressions

for Vt . We show that Vt exhibits a lognormal distribution when rt is a normal/Gaussian

process defined by a common variety of narrow sense linear SDEs. While we also provide

explicit solutions for Vt when rt evolves according to general linear and some well

known nonlinear SDEs, the distribution of Vt is not explicitly known in many of these

other cases. The results can be applied to many financial situations where modeling value of

the firm is critical. For example, there is a large literature concerning structural models of

yields on corporate debt.

Some structural models assume a constant rate of interest while

others utilize, for example, interest rate models consistent with the popular Vasicek (1977)

model. Our solutions for the distribution of Vt readily permit detailed analysis of the term

structure of default risky yields and credit spreads. More specifically, we analyze how the

probability of default varies with maturity and, in turn, analyze the complex interactions of

maturity, drift in Vt , and variance of Vt upon default risky yields and credit spreads.

2

Introduction

Modeling the value of the firm is one of the more important research topics in

finance. The value of an unlevered firm is the value of expected future cash flows

discounted at a rate appropriate for an all-equity firm whereas the value of a levered

firm is commonly expressed as the value of an unlevered firm plus the gain from

leverage due to a tax shield provided by the debt. Including business disruption costs,

the optimal capital structure can then be characterized as a trade-off between the

interest tax shield and disruption costs. Recent analysis by Hackbarth, Hennessy and

Leland (2007) extends this line of research by examining an optimal mixture of debt;

that is, the optimal mixture of bank debt and market debt (bonds).

Leland and Toft (1996) develop an ambitious model of firm value that addresses

optimal capital structure, optimal debt maturity, and shape of credit spreads. They

describe alternative shapes of credit spread term structures dependent upon various

conditions. Generally, the shapes are either positively sloped throughout or humped.

Recently, Qi (2007) has modified the Leland and Toft (1996) by setting the lower

bankruptcy boundary to be a fraction of bond face value.

The importance of good structural models for credit spreads has been enhanced

with the growth of credit derivatives and the credit crisis of 2007.

More specifically,

notional amounts of credit derivatives grew by over 100% for every year from 2004

through 2006. At the end of 2006, there was 34.5 trillion outstanding. 1 The weakened

credit quality of many financial firms in 2007 caused high volatility in equity markets

and, also, large changes in the value of credit spreads and credit default swaps. For

example, spreads on Citigroup credit default swaps rose 30 basis points in the first

week of November where a basis point is worth $1,000 per year. Eom, Helwege, and

1

“Credit Derivatives Show Surge”, A. Saha-Bubna and E. Barrett, Wall Street Journal, April 28, 2007.

3

Huang (2004) strongly suggest there is a need to improve structural models of credit

spreads because their empirical tests reveal obviously large weaknesses.

Our purpose is two-fold. The first purpose is to derive alternative distributions of

Vt for commonly used processes of short term interest rates. This is desirable

because value of the firm, Vt , processes are strongly dependent on processes of short

term interest rates.

Alternative short term interest rate processes can be classified as

narrow sense linear functions of r, generally linear in r, or nonlinear in rt. The resulting

distributions of Vt can be easily compared to distributions where rt is assumed

constant.

The second purpose is to apply these Vt distributions to structural models of

credit spreads. We develop equations for default risky spot rates and credit spreads

utilizing Vasicek (1977) interest rate processes, a popular narrow sense linear model

very commonly used in structural models. Probability of default is determined by a first

passage approach where default occurs if value of the firm pierces certain lower

thresholds. Probability of default depends on all parameters of the Vasicek (1977)

model including mean reversion parameters. Probability of default may be expressed as

a function of expected Vt and variance of Vt . More specifically, greater maturity

increases both expected Vt and, also, variance of Vt. Thus, the impact of increasing

maturity upon spread is complex. Surprisingly, probability of default may or may not

increase with maturity.

The next section describes models of firm value and the following section

describes the framework for solutions of firm value.

Then we describe solutions in

the cases where interest rate processes are narrow sense linear. Finally, we describe an

application of our theoretical results to modeling credit spreads of corporate bonds as

4

dependent upon features of a popular interest rate process.

1. Models of Firm Value Dependent Upon Interest Rate Processes

The time evolution of the value, Vt , of a firm is routinely modeled by a linear,

scalar, stochastic differential equation (SDE)

dVt

= rt dt + s v ( t ) dWv , t

Vt

,

(1.1)

where the instantaneous drift rt denotes the (exogenous) stochastic short-term interest

rate process and s v ( t ) is the instantaneous volatility. See, for example, Acharya and

Carpenter (2002). The dynamics of rt are commonly modeled by a (scalar) SDE of the

type

drt = a ( rt , t )dt + s ( rt , t )dWr ,t ,

(1.2)

where the instantaneous drift, a ( rt , t ) and the volatility, s ( rt , t ) are smooth

functions. It is further assumed that the Wiener increment processes dWv and dWr

are correlated where

E éê( dWv , t

ë

with

)( dWr ,t ) ùûú= r ( t )dt

(1.3)

r ( t ) £ 1 . It is worth noting that in this framework the flow of information is

only one way: rt affects Vt and not vice versa. Our first purpose in this paper is to

solve for Vt and characterize the distribution of the process Vt for different choices

of the rt processes.

Models utilized for the rt process can be divided into linear and nonlinear models.

Following Arnold (1974), linear models can be further subdivided into two subclasses.

The single factor model in (1.2) is called a narrow sense linear model if

5

a (rt , t )= a1 (t )rt + a2 (t )

,

(1.4)

and

s ( rt , t )= s r (t )

(1.5)

That is, the drift term is linear in rt and the volatility term is not a function of rt .

In

contrast, the model is called a general linear model if a ( r, t ) is of the form (1.4) and

s ( rt , t )= b1 (t )rt + b2 (t ) ,

where ai (t ), bi (t ), i = 1, 2 and s r (t ) are smooth functions of time t .

(1.6)

Finally, the

model is called nonlinear if either a ( rt , t ) and/or s ( rt , t ) are nonlinear functions of

the short rate rt .2

Similarly, Black (1995) defines three classes of rt processes by considering “a

simple random process without worrying about the forces that influence the interest

rate”. Thus, if

drt = s (rt , t )dWr ,t ,

(1.7)

then, rt is (1) a normal/Gaussian process if s ( rt , t ) is independent of rt , (2) a

lognormal process if

s ( rt , t )= s (t )rt , and (3) a square root process if

1

s ( r , t )= s (t )rt 2 .

The above classifications have a lot in common as given in Tables 1a,b,c. The

narrow sense linear models of Merton (1973), Vasicek (1977), Ho-Lee (1986), Hull and

White (1990) and generalized Hull and White (2000) are special cases of the Heath,

Jarrow and Morton (1992) model and define normal/Gaussian processes.

The nonlinear models of Black, Derman and Toy (1990) and Black and Karasinki

(1991) are in fact narrow sense linear SDE’s in ht = ln rt implying ln rt is a normal

2

See Cairns (2004) for more on the classification of interest rate models.

6

process and hence rt is a lognormal process (Johnson et. al. (1994)). The general

linear models of Dothan (1978) and Brennan and Schwartz (1979) give rise to

lognormal processes. The nonlinear models of Cox, Ingersoll and Ross (1985) and

Pearson and Sun (1994) define the so called square root processes.

There are essentially two ways of solving the system (1.1) - (1.2). The first method

T

is to define a vector Markov process X t = (Vt , rt )

and express (1.1) - (1.2) in a

single equation

dX t = f ( X t , t )dt + s ( X t , t )dBt ,

where f ( X t , t ) =

T

( f1 ( X t , t ), f 2 ( X t , t ))

T

dBt = ( dB1,t , dB2,t )

, s ( X t ,t )

is

(1.8)

a

2´ 2

matrix

and

is a vector of two independent Wiener increment processes. It

can be verified that if (1.2) is linear, then so is (1.8). In this case we can solve (1.8)

explicitly using the methods in chapter 8 of Arnold (1974). However, since solving

even the simple linear vector equations can be very demanding, in this research we use

a simpler alternative approach that exploits the one way dependence of Vt on rt . We

first solve the scalar SDE (1.2) for rt and using the solution in (1.1), we then

recover Vt is a lognormal process when rt º r , a constant. However, it is very

unappealing to assume interest rates are constant in many cases. For example, the V t

process is critical in valuing corporate bonds whose value clearly depends on the level

of interest rates. We show that Vt also exhibits a lognormal distribution where rt is a

normal process defined by the narrow sense linear models in Table 1. The results are

quite different when rt is a lognormal process defined by general linear models or by

narrow sense linear models in ln rt .

In these cases, while we derive expressions for

the exact solution of Vt , its distribution is not lognormal. Similar conclusions apply

7

when rt evolves according to the nonlinear models. (See Table 1.)

To our knowledge this is the first attempt to quantify the sensitivity of the solution,

Vt of (1.1) and its distribution with respect to the various interest rate models. One

general result is that the distribution of Vt varies widely from lognormal to other

classes of distributions as we vary interest rate models across the narrow sense linear,

general linear and nonlinear models. Thus, two important open questions are: (1) What

is an appropriate model for the distribution of Vt and (2) in the framework given by

(1.1) - (1.2), what classes of interest rate models can give rise to a well defined Vt

process?

2.

The Framework for the Solution

In this section we develop a framework for solving (1.1) - (1.2). Setting

g t = ln Vt and applying Ito’s lemma, (1.1) becomes (Kloeden and Platen (1992))

æ

ö

1

dg t = çç rt - s v2 (t )÷

dt + s v (t )dWv ,t .

÷

÷

çè

ø

2

(2.1)

The following result can be easily verified.

Lemma 2.1

Let dW1,t and d W 2,t be two independent standard Wiener increment

processes. The two correlated processes d Wv ,t and d W r ,t in (1.3) can be expressed

as linear functions of dW1,t and d W 2,t given by

dWr ,t dW1,t ,

(2.2a)

and

dWv ,t = r (t )dW1,t + 1- r 2 (t )dW2,t

(2.2b)

Substituting (2.2) in (2.1) and (1.2), we get

8

drt = a (rt , t )dt + s (rt , t )dW1,t ,

(2.3)

and

é

ù

1

dg t = êrt - s v2 (t )údt + s v (t )éêr (t )dW1,t + 1- r 2 (t )dW2,t ù

.

ú

êë

ú

ë

û

2

û

(2.4)

Integrating (2.4), it follows that

gt = g0 +

ò

t

0

rs ds -

1 t 2

s v ( s )ds +

2 ò0

ò

t

0

s v ( s )r ( s )dW1, s +

ò

t

0

s v ( s ) 1- r 2 ( s )dW2, s

(2.5)

The following two properties of the Wiener process are easily verified (Shiryaev

(1999), Oksendal (2003), Kuo (2006)).

Lemma 2.2. If Wt is a standard Wiener process, then, for c>0,

Wt =

1

W2 .

c ct

(2.6)

If c > 1 ( < 1 ), this is equivalent to time stretching (compression). Here t is called the

“physical time” and t = c 2t is called the “operation time”.

Let f : Â ® Â be a square integrable function on any finite interval such that

T (t ) =

ò

t

0

f 2 (t )dt < ¥

,

for all 0 < t < ¥

,

(2.7)

is a strictly increasing function with unique inverse.

Lemma 2.3 Relation between Ito integrals and Wiener process

The Ito integral

ò

0

t

f ( s )d Ws

9

with f(s) > 0 for 0 ≤ s ≤ t is equivalent to the standard Wiener process W t where

t = T (t ) =

ò

0

t

f 2 ( s )ds .

Combining Lemmas 2.2 and 2.3, and setting c 2 =

ò

0

t

f ( s )dWs = WT (t ) =

T (t )

t

, it follows that

T (t )

Wt

t

(2.8)

Applying (2.8) to the last two terms in (2.5) we obtain

ò

0

t

s v ( s )r ( s )dW1, s = W1,T1(t ) =

T1 (t )

W1,t ,

t

(2.9a)

where

T1 (t ) =

ò

t

0

s v2 ( s )r 2 ( s )ds .

(2.9b)

Also,

ò

t

0

s v ( s ) 1- r 2 ( s )dW2, s = W2,T2 (t ) =

T2 (t )

W2,t

t

,

(2.10a)

where

T2 (t ) =

ò

t

0

s v2 ( s )(1- r 2 ( s ))ds .

(2.10b)

Substituting (2.9) and (2.10) in (2.5) and simplifying, it follows that

é T (t )

ù

é 1 t

ù

T2 (t )

é t

ù

Vt = V0 exp êò rs ds úexp ê- ò s v2 ( s )ds úexp êê 1 W1,t +

W2,t úú . (2.11)

êë 2 0

ú

t

êë t

ú

14444êë420444443úû144444444

42 4444444443û1444444444444

42 44444444444443û

I

II

III

Since s v (t ) is assumed to be deterministic, the second factor, I I , in (2.11) is

deterministic. From the independence of W1,t and W2,t , it follows that the sum of the

10

two terms in the exponent of the third factor I I I in (2.11) is Gaussian from which we

infer that the third factor I I I in (2.11) is lognormal. Thus, the distribution of Vt in

(2.11) critically depends on the properties of the rt process in (2.3).

For later reference, we consider two special cases.

Case 1: s v (t )= s v , a constant and r (t )º r , a constant.

In this case,

T1 (t )= s v2r 2t and T2 (t ) = s v2 (1- r 2 )t .

(2.12)

Substituting these into (2.11) and simplifying we get

é t

ù

1

é

ù

Vt = V0 exp êò rs ds - s v2t úexp ês v r W1,t + 1- r 2 W2,t ú .

êë 0

ú

ë

û

2

û

{

Case 2: s v (t )= s v

,

}

(2.13)

r = 0 . In this case (2.13) reduces to

é

ù

1

é t

ù

Vt = V0 exp êò rs ds úexp ês vW2,t - s v2t ú ,

êë

2 3ú

û14444444

û

14444êë420444443ú

42 44444444

I

(2.14)

II

where the second factor I I in (2.14) is called a Brownian martingale or the stochastic

exponential (Shiryaev (1999), Kuo (2006)). In the following section we solve (2.3) for

rt for various choices of a ( rt , t ) and s ( rt , t ).

3. Narrow Sense Linear Solutions

Setting

a (rt , t )= q (t )- c (t )rt and s r (rt , t )= s r (t ) ,

(3.1)

in (2.3), we get a narrow sense (time varying) linear model known as the generalized

Hull and White (2000) model given by

drt = - c (t )rt dt + q (t )dt + s r (t )dW1,t

(3.2)

11

Since all the other narrow sense linear models in Table 1 are special cases of (3.2), we

first concentrate on solving (3.2).

Defining

ò

c (t ) =

t

0

c ( s )d s ,

(3.3)

from chapter 8 of Arnold (1974) and Gard (1988) we get

F ( t ) = e - c (t ) ,

(3.4)

as the fundamental solution of (3.2). Hence the solution of (3.2) is given by

rt = rt (det )+ rt (ran ) ,

(3.5a)

where

rt ( det ) = e

- c (t )

r0 +

ò

t

e

- éëc (t )- c ( s )ùû

q ( s )ds ,

0

(3.5b)

and

rt ( ran ) =

ò

t

e

- éëc (t )- c ( s )ùû

0

s r ( s )dW1, s .

(3.5c)

T3 (t )

W1,t ,

t

(3.6a)

By lemmas (2.2) and (2.3), we obtain

rt ( r a n ) = W1,T3 (t ) =

where

T3 (t ) =

ò

t

0

s r2 ( s )e

- 2 éëc (t )- c ( s )ùû

ds .

(3.6b)

Combining (3.5) and (3.6), it is immediate that

rt = rt ( det )+

T3 (t )

W1,t

t

~ N ( rt ( det ), T3 (t )) .

(3.7a)

(3.7b)

Hence

12

é T (t ) ù

é t

ù

é t

ù

exp êò rs ds ú= exp êò rs (det )ds úexp êê 3 W1,t ú

ú.

ú

êë 0

ú

t

ëê 0

û

û

êë

ú

û

(3.8)

Substituting (3.8) in (2.11) and simplifying we get an expression for Vt .

éæ T t

ù

ö

é t ïì

T3 (t ) ÷

T2 (t )

1 2 ïü ù

êçç 1 ( )

ú

÷

ê

ú

Vt = V0 exp ò í rs ( det )- s v (t )ý dt exp êç

+

W1,t +

W2,t ú. (3.9)

÷

÷

êë 0 ïîï

ú

ç

ï

2

t

t ÷

t

êçè

ú

ï 43û

þ

ø

1444444444444442 4444444444444

ë

1444444444444444444

42 44444444444444444443û

I

II

The first factor I in (3.9) is a deterministic function and the second factor I I in (3.9)

is a lognormal variate (Johnson et al. (1994)).

We summarize this result in the following:

Theorem 3.1: Let the interest rate rt evolve according to a narrow sense linear scalar

SDE of the type (3.2). Then, rt is a normal or Gaussian process and the solution Vt ,

called the value process in (1.1), is a lognormal process given by (3.9).

We now

enlist a number of corollaries as special cases.

Case 1: Let s v (t )º s v , and r (t )º r be constants. Then, using (2.12) in (3.9) we

get

éæ

é t

1 2 ù

ç

Vt = V0 exp êò rs ( det )ds - s v t úexp êêçç s v r +

0

ú

2

êççè

ëê

û

ë

ù

T3 (t ) ö

÷

2

÷

W1,t + s v (1- r )W2,t ú

÷

ú. (3.10)

÷

t ø

÷

ú

û

Case 2: Hull and White (1990) model: Setting c (t )º c and s r (t )º s r in (3.5) (3.6), it follows that

rt HW ( det ) = e - ct r0 +

rt

HW

( ran )=

ò

t

e

- c(t - s )

0

T3HW (t )

W1,t ,

t

q ( s )ds ,

(3.11)

13

HW

3

T

(t ) = s

2

r

ò

t

e

s r2 é

ds =

1- e ê

ë

2c

- 2 c(t - s )

0

2 ct

ù .

ú

û

Setting rt (det )= rt HW (det ) and T3 (t )= T3HW (t ) in (3.9), it follows that Vt H W is

lognormal.

Case 3: Ho-Lee (1986) model: Setting c (t )º 0 in (3.11), we obtain

rt HL ( det ) = r0 +

ò

0

t

q ( s )ds ,

rt HL (ran )= s rW1,t ,

(3.12)

T3HL (t )= s r2t .

Again by setting rt (det )= rt HL (det ) and T3 (t )= T3HL (t ) in (3.9), we see that

Vt H L is lognormal.

Setting c (t )º c , q (t )º q and s r (t )= s r in

Case 4: Vasicek (1977) model:

(3.11) we get

rtV ( det ) = e - ct r0 +

rtV ( ran )=

T3V (t ) =

qé

1- e - ct ù

ê

ú

ë

û,

c

T3V (t )

W1,t ,

t

s r2

(1- e2c

2 ct

)

(3.13)

.

Substituting these into (3.9), we readily see that VtV is lognormal.

Case 5: Merton (1973): Setting q (t )º q , c (t )º 0 and s r (t )º s r , we get

rt M (det )= r0 + qt ,

14

rt M (ran )= s rW1,t ,

(3.14)

T3M (t )= s r2t .

which on substitution into (3.9) implies that Vt M is lognormal.

Case 6: Let rt º r . Then s r (t )º 0 , T3 (t )º 0 , rt ( ran )º 0 , rt (det )º r . For this

choice, (3.9) implies that Vt is lognormal. If we further assume that s v (t )º s and

r t º r , then (2.13) and (3.9) it follows that

éæ 1 ö

ù

ú .

Vt = V0 exp êçç r - s v2 ÷

t

+

s

W

÷

v 2,t

êëçè

ú

ø

2 ÷

û

(3.15)

æV ö

éæ 1 ö 2 ù

ú

÷

ln ççç t ÷

~ N êçç r - s v2 ÷

÷

÷

÷t , s v t ú ,

êëçè

2 ø

è V0 ÷

ø

û

(3.16)

Since

the lognormal probability distribution of Vt is given by

æV ö

÷

pt ççç t ÷

÷=

è V0 ø÷

é

ê

ê

1

exp êêæVt ÷

ö

ê

2ps v t çç ÷

ê

÷

÷

çè V0 ø

êë

ù

ö æ s v2 ÷

ö ïü

ïìï çæVt ÷

ïý ú

çç r ÷

t

í ln çç ÷

÷

ú

÷

÷ çè

ïï è V0 ø

2 ÷

ø ïþ

ïú.

î

ú

2s v2t

ú

ú

ú

û

(3.17)

The mean and variance of Vt are given by Johnson et. al. (1994).

E Vt V0ert and Var (Vt )= V02e 2rt éêe s v t ë

2

1ù

ú

û

(3.18)

Examples of plots of (3.18) are given in Figures 1 and 2. Figure 1 gives examples

of the Vt distribution when rt is constant and the probability densities of VT at

T = 5, 10, 15, 20 are generated from (3.17).

VT increases with T and moves the VT

distribution curve toward the right, while, at same time, the variance of VT also

15

increases with T.

Figure 2 gives examples of the Vt distribution when rt follows Vasicek’s

(1977) model. First, we build a Vasicek system in Figure 2a to be very similar to the

constant interest rate model illustrated in Figure 1; that is, we set

q

= r0 , r = 0 and

c

use a small s r . We compute and plot the VT distribution at T = 5, 10, 15, 20 in

Figure 2a.

As expected, the distributions in Figures 1 and Figure 2a are very similar.

In Figure 2b, we introduce positive correlation ( r = 0.9 ) where the VT distribution

now has a lower peak and fatter tails than in Figure 2a.

Then, in Figure 2c, we

introduce negative correlation ( r = - 0.9 ) and the VT distribution shows a higher

peak and less fat tails.

We furthermore consider general linear models of rt as given in Table 1.

see Appendix A.

Please

Generally, we cannot determine the distribution of Vt . Next

consider nonlinear models of rt such as Black and Karasinki (1991); Black, Derman

and Toy (1990); and Cox, Ingersoll, and Ross (1985). In these cases we also cannot

determine the distribution of Vt . Please see Appendix B for details.

The above results may be used to derive expressions for the distribution of Vt .

Assuming positive drift, E Vt grows with time as does the variance around that

expected value. In cases below we refer to a specific time as T which is a terminal or

intermediate date for a stage in the life of the firm, such as maturity of the firm’s debt.

For brevity, we concentrate on narrow sense linear models in Table 2. As given in that

table, it is useful to represent log Vt V0

2

as distributed N μ 't , σ 't

where μ 't is a

2

drift unique to the particular interest rate process and σ 't is a variance also unique to the

16

particular process.

For example, in the Vasicek model,

1

1

T' r0 e cT T r0 v2T

c c

c 2

and

T' 2 2 v T3V T T T3V T v2T

.

Then, E Vt , Var Vt , and probability densities can be generally expressed as given

2

at the top of Table 2 where all depend upon particular μ 't and σ 't values.

The more complex drift and variance terms for the different rt processes can be

compared to the constant r case where the drift term is merely

variance merely T' v2T .

2

1 2

r v T

2

and the

In Merton (1973), is needed to prevent arbitrage in

the drift and ρ is needed in the variance. Furthermore, Vasicek (1977) requires both θ

and mean reversion parameter c in the drift.

4. Application to Structural Models of Credit Spreads

4.1 Expressions for Risky Spot Rates and Credit Spreads

The first structural model of credit spreads was given by Merton (1974) where

he assumed a constant short term interest rate.

Leland (1994) and Leland and Toft

(1996) also assume a constant interest rate and thus, as in Merton (1974), there is no

correlation of stochastic changes in interest rates and stochastic changes in firm value.

Of course, it is unappealing to not allow interest rates to change in a model of bond

valuation. In contrast, Longstaff and Schwartz (1995) and Collin-Dufresne and

Goldstein (2001) models include both a Vt

process and, also, a rt process. Their

usage of dual processes is as we describe in Section 1. The rt process used by both is

17

a Vasicek (1977) model that is narrow sense linear.

Eom, Helwege, and Huang (2004)

provide a characterization of these and other popular structural models in an appendix.

The above structural models do not provide the distribution of Vt .

In

contrast, the distributions of Vt we have derived in earlier sections can now be used to

develop compact expressions for default risky spot rates, Rd T , and the spot rate

spread over a case with no default risk, Rdf(T).

Here Rd T Rdf T is denoted as

S T . Our solution of distributions permits spot rates and spreads to be concisely and

explicitly expressed as a function of probability of default. Of course, this combines the

two processes for rt and Vt where the level and volatility of Vt represents default

risk. Debt with no default risk and maturity T has present value at T of

PVdf T PAR . For a bond with default risk, the present value at T is

PVd t | t T PVdf T 1 Pd K , D, T PVdf T Pd K , D, T RR Pd K , D, T .

Here, Pd K , D,T is the first time (first passage) the firm value hits a level where

default occurs. Default occurs when the value of the firm falls below the face

value of the debt ( K ) at time T.

Additionally, as in Giescke (2004), default

occurs before maturity, t < T , when the value of the firm falls below a level, D .

That is, frequently creditors have a right to reorganize the firm if value falls below

D.

Various covenants in bank loans, bonds, and other debt may contain such a

condition. For our purposes, we assume, as given in Giescke (2004), that D is

below K . Thus, Pd K , D,T is the probability the first passage is at t or T .

RR is the recovery rate of principle in case the firm defaults. For our purposes,

18

we assume the recovery rate is a constant, 0.50.

For various short rate models, we have v , r , t , c , as parameters

in the model. By applying the above exact solutions, we can find the distribution

of firm value at any specific time.

thresholds

At a specific time, if we also know the default

K , D , then we easily can find the default probability

Pd K , D, t at

time t. With this, we can further derive the default risky bond price at maturity

T , PVd T , from the default-free bond present value, PVdf T , the PAR value of

the bond.

The risky spot rate and spread are derived from the default-free spot rate

Rdf T and the default risky bond price at maturity, PVd T .

PVd 0 PVd T e

Rdf T T

PVd 0 is the present value of the bond which may default at T. Of, course,

PVd 0 PVd f 0 due to the risk of default.

To define the risky spot rate, Rd T , we easily construct a default risky bond,

which sells at PVd 0 at present, and is valued at PAR at maturity. So,

PVd 0 e

Rd T T

PAR PVd f T

.

After substituting,

PVd T e

Rdf T T

e

Rd T T

PAR PVdf T

.

Then, dividing both sides by PVd (T ) and simplifying we obtain

19

Rd T

1

1

ln

Rdf T

T 1 1 RR Pd K , D, T Pd K , D, T

and

S (T ) Rd T Rdf T

1

1

ln

T 1 1 RR Pd K , D, T Pd K , D, T

As long as Pd K , D, T 0 ,and RR Pd K , D, T 1 ,

1 1 RR Pd K , D, T Pd K , D, T 1 , which implies that Rd T Rdf T . The

probability of default, Pd K , D, T , can be derived from the alternative distributions of Vt

prescribed above.

4.2 Computations of Risky Spot Rates and Credit Spreads

Given the above equations for Pd K , D, T , Rd T , and S T , we may now

apply the prior alternative solutions for Vt to analyze risky spot rate term structures

and credit spread term structures. Our examination has an analytical advantage

compared to prior research in that we can readily compute expected values and

variances from the above distributions. Assuming, for example, a popular Vasicek

(1977) model of short term interest rates, we can very easily plot E VT and

Var VT , and Pd K , D, T for any parameters of that particular interest rate process.

Then we analyze how complex interactions dictate various levels and shapes of Rd T

and S T term structures.

E Vt values that grow with time obviously tend to reduce default risk

because, in the great majority of

cases, the value of the firm is assumed to drift

20

upward with the passing of time.

In the above cases, the growth rate in firm value is

obviously affected by the level of interest rates and the rt process in the alternative

interest rate models.

However, at the same time that E Vt grows with time, the

variance of Vt also increases with time. At each future point in time, the probability of

default (first passage) can be computed where greater default probability obviously

increases Rd (T ) and S (T ).

A large rate of increase in probability of default due to time passage tends to

increase the relative slope of Rd T and S (T ) even though the slopes may positive

or negative. However, we note that the impact of a first passage probability that grows

with time is complex. That is, first passage probability may grow with time but, S (T )

may or may not increase because the present value of the loss is diminished with

greater time.

Furthermore, it is quite interesting to demonstrate that the probability of

default may not necessarily increase with time.

Figure 3 is one example of how our analysis permits detailed analysis of default

spreads using the Vasicek (1977) model common to many structural models. Here we

assume an initial firm value of 150, θ of 0.03, and no correlation between firm value

and level of interest rates. Other Vasicek parameter values are given in Figure 3.

Expected value of the firm rises with maturity where it is 268 at a maturity of 10. The

square root of Var VT in the second panel increases to 59 at maturity 10. The first

passage probability always grows with maturity which is shown in the third panel

( Pd K , D,T ) and fourth panel which displays the derivative of Pd with respect to T.

The last two panels display Rd T and S(T). Note that Rd T peaks at around

T=3

which is in contrast to R d f . Thus, even though the probability of default

21

consistently increases, its impact on the spot rate weakens because the present value of

the loss declines with time. Similarly, the spread peaks at around T=3 and then

declines.

Figure 4 is another set of graphs depicting default spreads where θ is 0.07 instead

of 0.03. Here expected value of the firm grows more rapidly but so does variance

around expected value. The net effect is to reduce probability of default relative to the

previous figure.

Interestingly, the probability of default peaks and then falls and thus

its derivative becomes negative. For this case, Rd T always increases but S(T) peaks

at about T=2.0, a little bit earlier than our previous figure. The earlier peak

and

subsequent steep decline is due to the peak in the probability of default.

The peak in probability of default Pd is counterintuitive at first glance but can be

partially explained as follows. Assume the D default threshold is relatively low such

that default before T is low. Then, the likelihood of default is largely dependent upon

default potential at the higher threshold K at time T. The passage of time increases

expected value and also increases variance where the net effect on probability of

default is unclear. Greater E Vt may dominate the increase in variance so that

default declines with T.

3

5. Conclusion

The value of the firm, Vt , is the sum of all claims upon it. In the simplest case,

Vt is just the sum of equity and zero coupon debt. More complex cases consider

secured versus unsecured debt, junior versus senior debt, convertible bonds and

preferred stock. A weakness of much of the research concerning Vt is the lack of an

3

See Giesecke (2004) for separate expressions of default before T and at T.

22

expression for its expected value and variance as time advances. That is, much of the

research generally describes expected firm value that grows with time where the

instantaneous variance of the process describes the volatility and riskiness of the firm.

There is a need for precision in the distribution of Vt .

One outstanding stream of research that uses the concept of Vt quite intensively

concerns structural models of credit risk. Strong growth in credit derivatives and the

recent credit crises have both increased the demand for improved models of credit risk.

We note that popular structural models commonly utilize simultaneous processes for

Vt and short term interest rates, rt , where changes in Vt are dependent upon the

particular rt process assumed.

to linearity in the rt

Recognizing different classes of models with respect

process, we show that the exact distribution of Vt depends on

the type of rt process assumed. In some cases, Vt is lognormally distributed. For

example, the Vasicek (1977) process commonly assumed in structural models leads to a

lognormal Vt.

A well defined Vt distribution permits us to easily analyze default

probabilities and term structures of credit risk in great detail. Greater passage of time

suggests greater expected firm value but, at the same time, greater variance of Vt so that

the impact of maturity on default probability is complex. The behavior of default

probability with passage of time has a clear impact on term structure of credit spreads

where a strong growth in probability of default increases the slope of the term structure

of credit spreads. It is interesting to note that probability of default may decrease with

greater maturity.

23

References

Acharya, V.V. and J.N. Carpenter (2002) “Corporate Bond Valuation and Hedging

with Stochastic Interest Rate and Endogenous Bankruptcy”, The Review of

Financial Studies, Vol. 15, 1355-1383.

Arnold, L. (1974) Stochastic Differential Equations: Theory and Applications,

John Wiley & Sons, New York, 228 pages.

Black, F. (1995) “Interest rate options”, The Journal of Finance, Vol. 50, 1371-1376.

Black, F., E. Derman and W. Toy (1990) “A one-factor model of interest rates and its

application to treasure bond options”, Financial Analysts Journal, Vol. 46, 33-39.

Black, F. and P. Karasinski (1991) “Bond and option pricing when short rates are

log-normal”, Financial Analysis Journal, Vol. 47, 52 – 59.

Brennan, M. and E. Schwartz (1979) “A Continuous-Time Approach to the Pricing of

Bonds”, Journal of Banking and Finance, Vol. 3, 133-155.

Cairns, A.J.G. (2004) Interest Rate Models: An Introduction, Princeton University

Press, Princeton, N.J., 274 pages.

Collin-Dufresne, P. and R. S. Goldstein (2001), “Do Credit Spreads Reflect

Stationary Leverage Ratios?”, Journal of Finance, Vol. 56, 1929-1957.

Cox, J., J.Ingersoll and S.Ross (1985) “A Theory of the Term Structure of Interest

Rates”, Econometrica, Vol . 53, 385-407.

Dothan, M. U. (1978),“On the term structure of interest rates”, Journal of Financial

Economics, Vol. 6, 59-69.

Eom, Y.H.; J. Helwege; and J. Huang (2004) “Structural Models of Corporate Bond

Pricing: An Empirical Analysis”, Review of Financial Studies, Vol. 17, 499 -544.

Giesecke, K. (2004) “Credit Risk Modeling and Valuation: An Introduction” Chapter

16 in Credit Risk: Models and Management by D. Shimko, Risk Books, London.

Hackbarth, D. ; C. A. Hennessy and H. E. Leland (2007) “ Can the Trade-off

Theory Explain Debt Structure?”, Review of Financial Studies, Vol. 20,

1389-1428.

Heath, D., R. Jarrow and A. Morton (1992) “Bond Pricing and Term Structure of

Interest Rates: A New Methodology for Contingent Claims Valuation”,

Econometrica, Vol. 60, 77-105.

Ho, S.Y. and S.B. Lee (1986) “Term Structure Movements and Pricing Interest Rate

Contingent Claims”, Journal of Finance, Vol. 41, 1011-1029.

24

Hull, J.C. (2000) Options, Futures and other Derivatives, Prentice Hall, (4th

Edition), 698 pages.

Hull, J.C. and A.D. White (1990) “Pricing interest rate derivative securities”, Review

of Financial Studies, Vol. 3, 573-592.

Gard, T.C. (1988) Introduction to Stochastic Differential Equations, Marcel

Dekker Inc, New York, 234 pages.

Johnson, N.L., S. Kotz and N.Balakrishnan (1994) Continuous univariate

distributions, Volume 1. (Second Edition), John Wiley & Sons, Inc., New York,

756 pages (Chapter 14).

Kloeden, P.E. and E. Platen (1992) Numerical Solution of Stochastic Differential

Equations, Springer Verlag, 636 pages.

Kuo, H.H. (2006) Introduction to Stochastic Integration, Springer, New York, 278

pages.

Leland, H. E. and K. B. Toft (1996) “Optimal Capital Structure, Endogenous

Bankruptcy, and the Term Structure of Credit Spreads, “ Journal of Finance,

Vol. 51, 987-1019.

Longstaff,, F. A. and E. S. Schwartz (1995) “ A Simple Approach to Valuing Risky

Fixed and Floating Rate Debt”, Journal of Finance, Vol. 50, 789-819.

Merton, R.C. (1973), “Theory of Rational Option Pricing”, Bell Journal of

Economics and Management Science, Vol. 4, 141-183.

Merton, R. C. (1974) “ On the Pricing of Corporate Debt: The Risk Structure of

Interest Rates,” Journal of Finance, Vol. 29, 449-470.

Oksendal, B. (2003) Stochastic Differential Equations: An Introduction with

Applications, Springer Verlag, New York (sixth Edition), 360 pages.

Pearson, N. and T.S.Sun (1994) “An empirical examination of the Cox-Ingersoll-Ross

model of term structure of interest rates using the method maximum likelihood”,

Journal of Finance, Vol. 54, 929-959.

Qi, H. (2007), “Credit Spread by a Modified Leland-Toft Model” presented at FMA

meetings, Orlando.

Shiryaev, A.N. (1999) Essentials of Stochastic Finance:Facts, Models, Theory,

World Scientific, New York, 834 pages.

Vasicek, O. (1977) “An equilibrium characterization of the term structure”, Journal

of Financial Economics, Vol. 37, 339-348.

25

Appendix A:

General linear models for rt

Consider a general linear (time invariant) scalar SDE, known as the

Brennan-Schwartz (1979) model in Table 1

drt = - crt dt + qdt + s r rt dWr ,t .

(A.1)

From chapter 8 of Arnold (1974), it follows that

é æ s2ö

ù

÷

F (t ) = exp êê- çç c + r ÷

t + s rW1,t ú

÷

ú ,

2 ÷

ø

êë çè

ú

û

(A.2)

is the solution of

drt = - crt dt + s r rt dW1,t ,

and is the fundamental solution of (A.1). The solution of (4.1) is then given by

t

rt = F (t )r0 + q F (t )ò F - 1 (u )du .

1442 443 1444444442

0 444444443

I

(A.3)

II

Combining this with (2.11), it follows that

t

t

t

é

ù

Vt = V0 exp êr0 ò F ( s )ds + q ò F ( s )ò F - 1 (u )duds ú

0

êë 0

144444444444444444444

420 44444444444444444444

43úû

I

é T (t )

ù

é 1 t

ù

T2 (t )

exp ê- ò s v2 ( s )ds úexp êê 1 W1,t +

W2,t úú.

êë 2 0

ú

t

êë t

ú

144444444

42 4444444443û1444444444444

42 44444444444443û

II

(A.4)

III

To our knowledge, all we can claim at this stage is that F (t ) in (A.2) is lognormal

and so is F -

1

(t ). Since the distribution of the second term, I I , in (A.3) is not known,

we do not know the distribution rt in (A.3).

Similarly, we know that the second term, I I , in (A.4) is deterministic and third

term, I I I , in (A.4) is lognormal. Since the first term, I , in (A.4) involves the integral of

rt , its distribution is not known. Hence, while we know the exact form of the solution

26

Vt in (A.4), its distribution is not known. We conjecture that it is not lognormal.

In the special case when q º 0 and the sign of c in (A.1) is changed, we get

Dothan’s (1978) model. In this case

rt = F (t )r0 ,

(A.5)

and

é T (t )

ù

t

é 1 t

ù

T2 (t )

é

ù

Vt = V0 exp êr0 ò F ( s )ds úexp ê- ò s v2 ( s )ds úexp êê 1 W1,t +

W2,t úú.

êë 2 0

ú

êë 420 444444443úû

t

êë t

ú

14444444

144444444

42 4444444443û1444444444444

42

4444444444444

3û

I

II

III

(A.6)

In this case, while F (t ) and hence rt are lognormal, we don’t know the distribution

of the first term, I , which is correlated with the first term,

T1 (t )

W1,t in the

t

exponent of the third term, I I I , in (A.6). Again, we have an explicit expression for Vt ,

but don’t know its distribution.

27

Appendix B: Nonlinear Models for rt

In this section, we consider the class of nonlinear models due to Black and

Karasinki (1991). In this model ht = ln rt evolves according to a scalar, narrow sense

(time varying) linear SDE

d ht = - c (t )ht dt + q (t )dt + s r (t )dW1,t .

(B.1)

By exploiting the similarity between (B.1) and (3.2), we readily obtain

ht = ht (det )+ ht (ran ) ,

h t ( det ) = e

- c (t )

r0 +

ò

t

e

0

(B.2)

- éëc (t )- c ( s )ùû

q ( s )ds ,

and

h t ( ran ) = W1,T3 (t ) =

T3 (t )

W1,t .

t

where c (t ) and T3 (t ) are defined in (3.3) and (3.6b) respectively. Hence

h t = h t ( det )+

T3 (t )

W1,t ~ N éëh t ( det ), T3 (t )ù

û,

t

(B.3)

and

é

rt = exp êêht (det )+

êë

T3 (t ) ù

W1,t ú

ú.

t

ú

û

(B.4)

That is, rt has a lognormal distribution. Combining this with (2.11), we get

é t

ïì

ïü ùú

T3 ( s )

ê

Vt = V0 exp êò exp ïí h s ( det )+

W1, s ïý ds ú

ïï

ïï ú

s

ê 0

îï

þï 43û

ë

144444444444444444

42 44444444444444444

I

é T (t )

ù

é 1 t

ù

T2 (t )

exp ê- ò s v2 ( s )ds úexp êê 1 W1,t +

W2,t úú.

t

ëê 2 420 4444444443ûú

êë t

ú

144444444

1444444444444

42 44444444444443û

II

(B.5)

III

The second factor, I I , in (B.5) is deterministic and the third factor, I I I , in (B.5) is

28

lognormal. The distribution of the first factor, I , in (5.5) is not known. In view of the

similarity between the Black and Karasinki (1991) and Black, Derman and Toy (1990)

model, the above analysis and conclusion carry over to the latter class of models as

well.

Also, we observe that if rt evolves according to the Cox, Ingersoll and Ross

(1985) model, then it can be shown (Chapter 4, Cairns (2004)) that rt has a non-central

chi-squared distribution. Referring to (2.11), in this case, since the first factor, I ,

involves the exponential of the integral of a non-central chi-squared process rt , its

distribution and hence that of Vt are unknown.

29

Table 1: Alternative Models of rt According to Linearity in rt

Table 1a: Narrow sense linear stochastic interest rate models

Merton (1973)

drt = qdt + s r dWr

rt - Gaussian

Vasicek (1977)

drt = (q - crt )dt + s r dWr

rt - Gaussian

Ho-Lee (1986)

drt = q (t )dt + s r dWr

rt - Gaussian

Hull and White (1990)

drt = (q (t )- crt )dt + s r dWr

rt - Gaussian

Generalized Hull and White (2000)

drt = (q (t )- c (t )rt )dt + s r (t )dWr

rt - Gaussian

Table 1b:

General linear stochastic interest rate models

Dothan (1978)

drt = qrt dt + s r rt dWr

rt - lognormal

Brennan-Schwartz (1979)

drt = (q - crt )dt + s r rt dWr

rt - lognormal

Table 1c:

Nonlinear stochastic interest rate models

Cox-Ingersoll-Ross

(1985)

drt = q (m- rt )dt + s r rt dWr

rt

Pearson-Sun (1994)

drt = q (m- rt )dt + s r rt - b dWr

- Non-centered

chi-squared

distribution

rt - modified

Black, Derman and Toy

(1990)

ö

s '(t )

drt æ

1

÷

= ççç q (t )+ s 2 (t )+

ln rt ÷

dt + s r (t )dWr

÷

÷

çè

rt

2

s (t )

ø

or

with

t ln rt

'

æ

s (t ) ö

÷

d h t = ççç q (t )+

ht ÷

dt + s r (t )dWr

÷

÷

çè

s (t ) ø

square root

process

rt - lognormal

,

30

TABLE 2 Distribution of Value of Firm: Narrow Sense Linear Interest Rates Models

éæ 1

Vt

2

2

'

'2

Vt = V0 e x pêçç r- s

ln a1 bW

1 1 b2W2 ~ N a1 , b1 t b2 t N t , t

êëçè

2

V0

E éëV (T )ù

û= V0e

mT' +

2

s T'

2

,

Var V T V02e

2

T' 2 T'

Model

e 1

2

T'

V

P T

V0

1

e

V

'

T

2 T

V0

VT

'

ln T

V0

2

2 T'

,

2

ö

÷

+t s

÷

÷

ø

v

ù

ú

W

2 , t

ú

û

VT

ln T'

V 1 1

V0

cdf T erf

2 T'

V0 2 2

2

T' and T'

rt Process

rt º r

Constant r

,

2

v

Processes

1

T' r v2 T

2

T' v2T

2

Merton (1973)

drt = qdt + s r dWr

1

1

T' T 2 r0 v2 T

2

2

T' 2 v rT r2T v2T

2

Vasicek (1977)

drt = (q - crt )dt + s r dWr

1

1

T' r0 e cT T r0 v2T

c c

c 2

T' 2 v

Ho-Lee (1986)

drt = q (t )dt + s r dWr

r2

2

1 e 2 cT T r 1 e 2 cT v2T

2c

2c

b1t

b2t

Assume q (t ) = a1e + a2 e , where a1 , a2 , b1 , b2 are constants

2

mT' =

ö

a1 b1T a2 b2T æ

a

a

a

a

1 ÷

e + 2 e + ççç r0 - 1 - 2 - s v2 ÷

T - 12 - 22

÷

÷

b1 b2 2 ø

b12

b2

b1 b2

è

T' 2 v rT r2T v2T

2

Hull and

(1990)

White

d rt = (q (t )- crt )d t + s r d Wr

Assume q (t ) = a1e b1t + a 2e b2t , where a1, a2, b1, b3 are constants

mT' =

a1

a2 ö÷

a1

a2

a1 a2 ö÷

1 - cT æ

1 2

1æ

b1T

b2T

ç

÷

e çç- r0 +

+

÷+ cb + b 2 e + cb + b 2 e - 2 s v T - c çç- r0 + b + b ÷

÷

÷

çè

c

c + b1 c + b2 ø÷

è

1

2 ø

1

1

2

2

T' 2 v

2

r2

2

1 e 2 cT T r 1 e 2 cT v2T

2c

2c

31

Figure 1

Probability Density of VT for Constant r

Model: constant r t=r

Parameters: r = 0.1 V0 = 150

= 0.2

v

1

T

T

T

T

0.9

Probability density of V

T

0.8

=

=

=

=

5

10

15

20

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0

0 100 200

400

600

800 1000 1200

Value of firm V T

1400

1600

1800

2000

32

Figure 2a

Probability Density of VT for Vasicek with σr = 0.1, ρ = 0

Model: Vasicek:

Parameters: r 0 = 0.1 = 0.05 c = 0.5 r = 0.1

= 0.2 = 0 V = 150

0

v

1

T

T

T

T

0.9

Probability density of V

T

0.8

=

=

=

=

5

10

15

20

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0

0 100 200

400

600

800 1000 1200

Value of firm V T

1400

1600

1800

2000

33

Figure 2b

Probability Density of VT for Vasicek with σr = 0.1, ρ = 0.9

Model: Vasicek:

Parameters: r 0 = 0.1 = 0.05 c = 0.5 r = 0.1

= 0.2 = 0.9 V = 150

v

0

1

T

T

T

T

0.9

Probability density of V

T

0.8

=

=

=

=

5

10

15

20

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0

0 100 200

400

600

800 1000 1200

Value of firm V T

1400

1600

1800

2000

34

Figure 2c

Probability Density of VT for Vasicek with σr = 0.1, ρ = - 0.9

Model: Vasicek:

Parameters: r 0 = 0.1 = 0.05 c = 0.5 r = 0.1

= 0.2 = -0.9 V = 150

v

0

1

T

T

T

T

0.9

Probability density of V

T

0.8

=

=

=

=

5

10

15

20

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0

0 100 200

400

600

800 1000 1200

Value of firm V T

1400

1600

1800

2000

35

Figure 3

The Behavior of Default Risky Spot Rates and Spreads Dependent upon the

Distribution of Vt : Probability of Default Increasing with Maturity

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

600

T

E(V )

500

Expectation of V

T

400

300

200

100

0

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 3a

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

120

110

90

80

Volatility of V

T

T

vol(V )

100

70

60

50

40

30

20

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 3b

36

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

0.1

0.09

0.08

d

P (K,D,T)

0.07

0.06

0.05

0.04

0.03

0.02

0.01

0

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 3c

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

0.035

0.03

0.02

d

Derivative of P (T) vs. T

0.025

0.015

0.01

0.005

0

-0.005

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 3d

37

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

Rdf(T)

0.14

Rd(T)

0.13

Spot Rate

0.12

0.11

0.1

0.09

0.08

0.07

0.06

0.05

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 3e

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

0.02

0.018

0.016

df

0.012

d

S(T) = P (T) - P (T)

0.014

0.01

0.008

0.006

0.004

0.002

0

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 3f

38

Figure 4

The Behavior of Default Risky Spot Rates and Spreads Dependent upon the

Distribution of Vt : Probability of Default Humped with Respect to Maturity

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

600

T

E(V )

500

Expectation of V

T

400

300

200

100

0

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 4a

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

120

110

90

80

Volatility of V

T

T

vol(V )

100

70

60

50

40

30

20

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 4b

39

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

0.1

0.09

0.08

0.06

d

P (K,D,T)

0.07

0.05

0.04

0.03

0.02

0.01

0

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 4c

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

0.035

0.03

0.02

d

Derivative of P (T) vs. T

0.025

0.015

0.01

0.005

0

-0.005

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 4d

40

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

Rdf(T)

0.14

Rd(T)

0.13

Spot Rate

0.12

0.11

0.1

0.09

0.08

0.07

0.06

0.05

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 4e

Vasicek: r 0 = 0.06 c = 0.5 r = 0.05

= 0.2 = 0 V = 150 K = 100 D = 75

v

0

0.02

0.018

0.016

df

0.012

d

S(T) = P (T) - P (T)

0.014

0.01

0.008

0.006

0.004

0.002

0

0

1

2

3

4

5

6

Maturity (T)

7

8

9

10

Figure 4f

41