Folie mit WIFO-Logo

advertisement

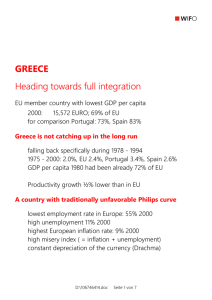

BELGIUM Administrative center and leading in industry productivity A small country divided by language 2.7% of EU population 3% of income Flames in the north, Wallonians in the South, Bilingual Brussels as informal capital of the EU Administrative center: Council and Commission Founding member of EU Pre integration with neighbors BENELUX D:\106739878.doc Seite 1 von 6 Economic Performance About average long run and short run growth: Output + 2.3% 1975-2000 The same for productivity growth 5th in GDP /capita: 24,100 in 2000 (EU: 22,500 EURO) 3rd in GDP/hour Low employment rate: 59% (EU: 65%, US 71%) Moderate unemployment and inflation Top productivity in manufacturing: 61,700 EURO 1999 2nd only to Ireland despite rather traditional structure Structure-productivity paradoxon High share of services: Brussels as “capital” of European Union D:\106739878.doc Seite 2 von 6 Disappointing growth drivers Low research intensity; 1.6 & of GDP Very low rate of patenting: 1/3 of EU Low share of ICT and technology driven industries Medium position of use of ICT (less than Netherlands, Denmark) Average position in education (high share of tertiary education) Low innovation rate, but high share of co-operations, joint ventures Low market capitalization, but high venture capital Out of all determinants of long run growth Only tertiary education PC use and co-operations are above average The ability to market incremental innovations and firm capabilities guarantees competitiveness D:\106739878.doc Seite 3 von 6 Policy Belgium is an open economy High export/import share High inward/outward FDI (in both directions, inwards slightly larger) Founding member and center of EU Difficult regional structure (Flames vs. Wallonians) High tax rates and tax wedges Tax rate GDP 49% (3% above EU average) Social expenditures and social contribution high Highest statutory corporate tax(together with Italy) 40% High effective rate (together with Germany, France, Portugal Government expenditure/GDP 50% (down from 63% early 80s.) Debt still high higher than GDP : 107% (2001) No specific activating labor market policy With coordination problems federal/regional level Considerable regulation of labor and partly product markets D:\106739878.doc Seite 4 von 6 Traditional industry structure in manufacturing 3.5% of European production 9% of exports Both with rising trend 2nd highest labor productivity in EU (surpassed by Ireland) High share of capital intensive basic goods industries basic chemicals + oil Steel, cement, textiles food industry low skill industries car manufacturing Low shares of Technology driven industry ICT industries High skill industries Successful dynamic industries Pharmaceuticals increased to 9% of EU exports Audio/video apparatus Publishing and printing Low and non increasing export unit value Low quality/high productivity characteristics Large firms: Fortis (bank), Tractebel (conglomerate), Almanij (bank), Delhiaize (retail), Dexia (bank) No leader in a manufacturing industry D:\106739878.doc Seite 5 von 6 Overall evaluation Success partly against the odds Traditional structure in industry High share of administration/government High taxes, still regulated markets Debt larger than GDP No large industrial firms (top 5: banks and finance) Difficult regional structure Large center, Wallonia and Flandern Skill drain to administrative jobs A position between “dominating” neighbors (Germany, F, NL) Upgraded by becoming the Center of Europe D:\106739878.doc Seite 6 von 6