Lecture 26 Notes

advertisement

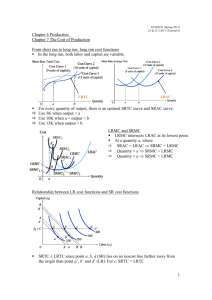

29 March, 2006 Reading: Ch 5. pp. 186-192 Problem #11: Due Friday Lecture 26 REVIEW___________________________________________________: IV. Chapter 5. The Production Process and Costs C. Costs 2. Short Run Costs. c. Algebraic Forms of the Cost Function. d. Sunk costs vs. Variable Costs Preview__________________________________________________________ 3. Long Run Costs a. Long run average costs b. Economies of Scale, Diseconomies of Scale and Long Run Survivability 4. Multi-Output Cost Functions Lecture____________________________________________________________ C. Costs and the Theory of the Firm 3. Long-Run Costs. In the Long run, all costs are variable. As I indicated at the outset of this chapter, the long run may be viewed as the planning horizon, since the project for the firm is to pick the optimal plant size. Information about the Long-Run Average Cost curve is very useful for determining the structure of an industry. a. Long Run Average Costs. The long run average cost curve (LRAC) is the envelope of all short run costs curves. That is, the LRAC is the tangency of all efficient production points on for each plant size. ATC0 ATC1 ATC2 ATC3 Economics of Diseconomies of Scale Scale Efficient Plant Size Q In the above chart, the bold line is the LRAC. Note that the efficient scale of operation is not at the point of minimum marginal costs unless the firm is at an optimal plant size. b. Economies of Scale Economies of Scale arise when LRAC falls as the plant expands. Reasons for Economies of Scale: - Physical Relationships (double a pipe diameter, and flow through expands quadratically) - Gains from specialization and division of labor Diseconomies of scale arise when LRAC increases as the plant expands. Reasons for Diseconomies of Scale Transportation Costs “Crowding” with respect to managerial efficiency Minimum Efficient Scale (MES): The first point where LRAC is at a minimum If a range exists where costs neither increase nor decrease, there exist constant returns to scale. Application: The shape of the LRAC can determine how many firms can survive in an industry. - Suppose that MES is 10,000 units, and that market demand, at a competitive price is 40,000 units. How many efficient firms can survive in the industry? - Suppose that MES is 10,000 units, but that diseconomies of scale set in very soon after achieving the optimal plant size. Can a single firm efficiently service the industry? - Suppose an industry is characterized by continuous diminishing returns to scale. What is the optimal industry structure? c. Measuring Returns to Scale. The notion of scale economies and diseconomies is related to production, and can be measured with a production function. A firm is said to enjoy increasing returns to scale if a constant increase in all inputs causes a more than proportionate increase in output. A firm that enjoys economies of scale does because it realizes increasing returns to scale The firm enjoys constant returns to scale if a constant increase in all inputs causes a constant increase in outputs. A firm with a range of plant choices at MES will enjoy constant returns to scale over this entire range. The firm has decreasing returns to scale if a constant increase in outputs causes a decreasing increment to outputs. Firms with diseconomies of scale may suffer decreasing returns to scale. Increasing, constant or decreasing returns to scale can be determined analytically. Here we introduce this by focusing on a specific form of production function Q = F(K,L) = (KL)a Consider a production function consisting of both Capital and Labor, Q = F(K,L) = K x L. When one unit of each input is used Q = 1. Doubling both inputs increases outputs to 2x2 = 4. This firm has increasing returns to scale. A firm with the production function Q = F(K,L) = (KL).5 has constant returns to scale. To see this, observe that when K = 1, and L = 1, Q =1. When K=2, L = 2, Q =2, etc. A firm with the production function Q = (K,L).25 has decreasing returns to scale When K=1 and L=1, Q =1. When K=2, L=4, Q = 4.25 =1.41 RULE: For any production function of the form Q = F(K,L) = (KL)a The firm exhibits increasing returns to scale if a>.5 The firm exhibits decreasing returns to scale if a<.5 The firm exhibits constant returns to scale if a=.5 Example: Suppose that the production function for Grecko’s Smoothies is F(K, L) = (KL).25 Grecko currently produces with K=4 and L=4. - What is output? - Would Grecko enjoy increasing, decreasing or constant returns to scale if it doubled output to K = 8, L = 8? - How would your answer change if Greko’s production function wast F(K, L) = (KL)1 4. Multiple Output Cost Functions. All of the insights pertaining to single product output apply to a multi-product firm. There are, however some interesting additional cost issues that arise. In finishing this chapter, consider two points: The notion of economies of scope, and economies of scale. To illustrate, we will consider cost conditions for a firm that produces just two products: Q1 and Q2. Denote the cost function for this firm as C(Q1, Q2). a. Economies of Scope: Exist when the joint production of two goods is less expensive that the production of both goods separately. Mathematically, if C(Q1, 0) + C(0, Q2) > C(Q1, Q2) Economies of scope are an important reason why firms produce multiple products. For example, it may be more efficient to produce both cars and light trucks in a single plant than to produce both good separately, the two products may share many parts of the same assembly (such as the chassis) and producing the products separately would require considerable duplicative construction. b. Cost complementarities: These exist in the marginal cost of producing one good increases when the output of another product is increased. Mathematically, when: MC1(Q1, Q2)< 0 Q2 This often arises when one product is a by-product of another. For example there are cost complementarities in the production of in the production of Flouride and Aluminum Ingot from Alumina. Cost complementarities are an important reason for economies of scope. These notions are conveniently expressed algebraically with at quadratic cost function: C(Q1, Q2) = f + Then MC1 = aQ2 + 2Q1 aQ1Q2 + Q12 + Q22 Cost complementarities exist whenever a < 0. Economies of scope exist whenever C(Q1, 0) + C(0, Q2) > C(Q1, Q2) C(Q1, 0) = f + Q12 C(0, Q 2) = f + Q22 Thus, economics of scope exist if 2f+ + Q12+ Q22 > f+ aQ1Q2 +Q12+Q22 Or if f - aQ1Q2 > 0. Comparing the two conditions, it is seen that cost complementarities are a stronger condition than economies of scope. Given a<0, cost complementarities always exist. However, economics of scope may also even without cost complementarities, if the costs of paying fixed set-up costs twice are sufficiently high. Example: Suppose C = 100 - .5Q1Q2 + Q12 + Q22 Do cost complementarities exist? Do economies of scope exist? What about the case where C = 100 + .5Q1Q2 + Q12 + Q22 ? Notice the existence of economies of scope and cost complementarities have a lot to do with the effectiveness of mergers and the sales of subsidiaries. Sales of an unprofitable subsidiary may not reduce losses much, due to cost complementarities. Similarly, due to economies of scope, it may be the case that multi-product mergers are efficient.