The mystery of Germany`s crazy bonds By Matt O`Brien May 8 at 11

advertisement

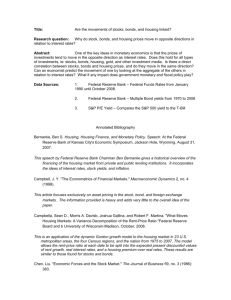

The mystery of Germany’s crazy bonds By Matt O'Brien May 8 at 11:14 AM Source: Bloomberg Germany's borrowing costs have shot up from nothing to slightly more than that in violent fashion, and it's either a sign that Europe's economy is finally beginning to recover or that the European Central Bank's efforts to do so are coming up short. It's not clear which. Just a few weeks ago, it looked like it would only be a matter of time until investors were paying for the privilege of lending to Germany for 10 years. In other words, that Germany's 10-year bond yield would slip from its low of 0.05 percent and into negative territory. Since then, though, it rocketed up to as much as 0.78 percent on Thursday, before falling back a bit to 0.59 percent later in the day. That's a massive one-day swing, given that bond yields usually only move a couple of hundredths of a percentage point on any given day. Still, it's worth keeping a little perspective here. These aren't through-the-looking-glass borrowing costs, but they're at least pushing up against the looking glass -- by any historical standard, they're still crazily low. That said, it is disconcerting how quickly Germany's bonds have sold off — bond prices go down when yields go up — and Europe's stocks have, too. This has narrowed the gap between interest rates in the United States and Europe, which has made holding money in euros more attractive — and, in turn, pushed the euro back up. What's going on? Well, Europe's bond yields were lower than ours to begin with because of their lower growth and lower inflation. But then in January, with inflation falling into negative territory, the ECB announced that it would start buying bonds with newly-printed money — aka quantitative easing — to try to jumpstart its economy. This, as you can see above, sent bond yields on what seemed like an inexorable journey to zero and below. Indeed, as much as $1.9 trillion worth of euro zone debt had negative yields by February. Investors were betting that they could buy bonds at near-to-subzero yields and then sell them back to the ECB a few months later for an easy profit. Now, the ECB clarified that it wouldn't buy bonds yielding less than -0.2 percent, which set a little bit of a ceiling on how low borrowing costs could go, but still left plenty of room for them to set records for alltime lows. And they did. At least until now. It's hard to tell what's going on, though, because it's hard to tell what QE does to borrowing costs. The simple story is that buying bonds should push their prices up, and, as a result, their yields down. But the problem is things aren't that simple, because QE also makes markets expect more growth and inflation — which go the other way and push bond yields up. That's why, as I've pointed out before, interest rates actually rose every time the Federal Reserve started buying bonds and fell every time it stopped. But, again, the problem is things aren't even as simple as that. Just look at Japan. It also started buying bonds, and also saw interest rates start to rise when it did, until its central bank chief said that they shouldn't rise — and then they didn't. In other words, even though higher borrowing costs are usually a sign that QE is working, it isn't always the case. So, what about Europe? It's tempting to say that, with euro zone growth and inflation prospects looking a little brighter, rates are rising in Germany because QE has already boosted the economy. But if that were the case, we'd expect stocks to still be going up, and they haven't in the past few weeks. So the fact that stocks and bonds have both been selling off at the same time that the euro has been strengthening tells us that monetary policy is actually getting tighter — the opposite of what we'd expect if it was QE making rates go up. But why would this be? Well, part of it might be that markets think the recovery isn't as strong as it looked a few weeks ago, but, thanks to QE, isn't as weak as it would need to be for policymakers to do any more; kind of a reverse Goldilocks. The other part might be that the United States has been so weak that markets now think the Federal Reserve will put off raising rates until later in the year, which, in turn, has made the dollar fall against the euro — weakening Europe's outlook, too. But there's a less interesting possibility. Markets might just be full of sound and fury, signifying nothing. They do that quite a bit. Specifically, so many people might have been betting — especially with borrowed money — that German yields would keep falling that if they started rising just a little they'd then start rising a lot as people ran for the exits to pay back what they owed before bond prices fell even more. Or, in finance-speak, bond trades got "crowded." If that's the case, then the wild swings in German bond prices are just an overreaction to the initial overreaction that prices would only keep going up. It wouldn't tell us anything other than that markets are prone to alternating paroxysms of greed and fear. So there you have it -- Germany's bond sell-off either means that Europe is recovering, that it isn't, or nothing at all. Sometimes markets aren't the clearest.