Lecture 4 - People.vcu.edu

Econ 604 Advanced Microeconomics

Davis

Spring 2005

10 February 2005

Reading. Chapter 4 (pp. 103 to 113)

Chapter 5 (pp. 116-144)

Problems: To collect: Ch. 3: 3.2, 3.4, 3.5, 3.7

Next time: Ch.4 4.2, 4.4, 4.6, 4.7,

4.9

Lecture #4.

REVIEW

III. Preference and Utility.

A. Axioms of Rational Choice

Completeness

Transitivity

Continuity

B. Utility

1 . Nonuniqueness of Utility Measures

2. The Ceteras Paribus Assumption

3. Utility form Consumption of Goods

4. Arguments of Utility Functions

5. Economic Goods

C . Trades and Substitution

1. Indifference curves and the Marginal Rate of Substitution

2. Indifference Curve Map

3. Indifference Curves and Transitivity

4. Convexity of Indifference Curves .

5. Convexity and Balance in Consumption

D. An Alternative Derivation (in terms of n variables)

E. Examples of Utility Functions

1. Cobb-Douglas Utility (exhibit Diminishing MRS)

2. Perfect Substitutes (Linear –exhibit constant MRS)

3. Perfect Complements (Lexographical – 0 MRS)

4. CES Utility (Exhibit a constant elasticity of substitution between inputs)

5. The Notion of Homotheticity (e.g., the MRS depends only on the ratio of the goods consumed).

Question: How might we define geometically this notion of homotheticity?

F. Generalizations to More than Two Goods

1

Some additional observations about utility.

The notion of utility that we’ve developed is based on relatively weak assumptions, and we can include a number of unconventional arguments. Consider some of these

. a.

Addictive Behavior: If utility for a good at a given time is a function of past consumption of the good, then we write

U t

(X t

, Y t

, S t

) where S t

=

X t-1

where S t

denotes all previous consumption.

In fact consumption in previous periods is often unobservable, so economists often write,

U t

(X t

*

, Y t

,) where X t

* =

X t

- X t -1.

This implies that utility increases from the consumption of X in the current period derives from increases in the consumption of X over the previous period.

Sometimes, related functions, such as those illustrating tastes for fairness are also of interest. b. Second Party Preferences. It is not necessary that individuals confine attention only to individual well being. For example, we might write

U i

(X, Y,, U j

) where i and j denote different individuals. U i

>0 implies altruistic tendencies, U j

<0 implies malevolence.

Preview_______________________________________________

IV. Utility Maximization and Choice

A. An Introductory Illustration. The two good case. (This is largely a graphical representation)

1. The Budget Constraint

2. First Order Conditions for a Maximum

3. Second Order Conditions for a Maximum

4. Corner Solutions

B. The n-Good Case

1. First Order Conditions

2. Implications of First Order Conditions

3. Interpreting the LaGrangian Multiplier

4. Corner Solutions

5. Some exercises with constrained utility maximization

C. Indirect Utility Function

D. Expenditure Minimization

2

LECTURE_____________________________________________

IV. Utility Maximization and Choice. This chapter continues our development of rational choice from a utility function. In the last chapter, we introduced the utility function. Now we consider rational decisions, given a budget constraint. As we will see, although the theory has several variants, they all appeal to a single basic theme.

The basic idea is simple: Suppose that we can divide each of n possible goods into

“boxes” that cost $1 each. Now suppose that the individual goes to a store with a fixed budget. The individual will maximize utility by purchasing those “$1 boxes” that yield the highest marginal utility. Now, of course, goods don’t all cost $1 per box. In this case, we can convert them all to dollar sized boxes by dividing the marginal utility by the price. Thus, given a vector of choices, 1, …., n, the consumer will maximize utility by picking so that

U

1

/p

1

= U

2

/p

2

= … = U n

/p n

.

If this condition does not hold, the consumer will increase utility the most by purchasing the product that yields the highest MU per dollar spent. A purchase, incidentally, will reduce the marginal utility, and bring the equation back toward equality. On the other hand, if a price falls suddenly the equation is out of equality, and the newly inexpensive good yields higher marginal utility per dollar spent. The rational consumer will purchase more units of that good.

Observe that humans need not have super calculating capabilities to make decisions that follow with this rule. All they need to be able to decide is which of the n available options yields the most “bang for the buck”

In what follows, we develop this rationale in more detail, starting with the 2 good case, and then proceeding to the more general case of n goods.

A. An Introductory Illustration. The two-good case.

1. The Budget Constraint. Assume consumers have available 2 goods, X and Y that may be purchased at price P

X

and P

Y

, respectively. They may spend up to their total income I on these products. This budget constraint may be written

P

X

X + P

Y

Y < I

I/ Py

To graph this in a two dimensional space, write it in

I = PxX + PyY slope/intercept form

Y= I/P

Y

- (P

X

/P

Y

)X

Notice that the slope of this constraint is -P

X

/P

Y

I/ Px

X

3

All consumption bundles up to those along the budget constraint are available.

However, only the assumption that more is preferred to less is necessary in order to conclude that a rational consumer will confine his or her attention to points on the budget frontier.

2. First Order Conditions for a

Maximum. Now overlay on this budget constraint some indifference

I/ Py curves, as shown in the pane on the next page. Observe that with the usual ordering (U

3

>U

2

>U

1

) the consumer maximizes utility at point C. At this point, the slope of the budget constraint and the MRS are equal, or

U x

/U y

= P

Or, alternatively, x

/P y

.

U x

/P x

= U y

/P y

.

3. Second Order Conditions for a Maximum. As long as the indifference curves are convex, this point of tangency will be a unique solution. (Thus, the second derivative of Y with respect to X must be strictly positive.) “Wiggles” in indifference curves undermine this unique tangency result. For example, in the figure shown in to the left, a non-convexity in the indifference curves implies that the point D is a point of tangency, but not a point of maximum utility. Rather C maximizes utility.

4. Corner Solutions Also, it may be the case that due either to relative prices or to weak preferences for a good, consumers may consume only one good. This is a “corner solution.” In the illustration, only units of good X are optimally consumed.

I/ Py

I/ Py

I = PxX + PyY

D

I = PxX + PyY

I = PxX + PyY

C

I/ Px

C

I/ Px U

1

C

U

3

U

1

U

2

U

3

U

3

U

2

X

X

I/ Px U

1

U

2 X

4

Our first order conditions must be modified to allow for this solution.

B. The n-Good Case. The graphical results derived above carry over directly to the case of n goods, a case which is better evaluated analytically.

1. First Order Conditions

Consider the utility function

Utility = U(x

1

, x

2

, …., x n

)

We maximize subject to the constraint (expressed in implicit form)

I- p

1 x

1

- p

2 x

2

-

….

- p n x n

= 0

Following the Lagrangian technique, we write

L = U(x

1

, x

2

, …., x n

) +

(I-p

1 x

1

-p

2 x

2

-…. - p n x n

) and taking first order conditions, yields

L / x

1

L / x

2

=

=

U/

U/

x x

1

2

-

-

p p

2

1

=

=

0

0

.

.

.

L / x n

=

U/

x n

-

p n

= 0

L /

= I-p

1 x

1

-p

2 x

2

-…. - p n x n

= 0

This is n+1 equations in the n+1 variables x

1

, x

2

,… x n

,

, which can be solved for a maximum as long as the equations are linearly independent.

2. Implications of First Order Conditions . Notice that for any two goods i and j above, we solve the above as

U xi

/U xj

= p xi

/p xj

This is the tangency condition derived for the case of two goods.

3. Interpreting the LaGrangian Multiplier . Notice also, solving for

yields

=

Or, equivalently

U x1

/p x1

= U x2

/p x2

=…. = U xn

/p xn

.

5

= M U x1

/p x1

= MU x2

/p x2

=…. = MU xn

/p xn

.

Thus,

reflects the marginal utility of an extra dollar of income. Notice that in an equilibrium, this marginal utility is equal for all goods.

Finally, taking

and any particular good i yields p x1

= M U x1/

That is, for any good purchased, the price of the good reflects the individual’s utility for the last unit consumed. That is, price is the marginal utility of the good relative to the marginal utility of income.

4. Corner Solutions The first order conditions hold only for interior maxima. When “corner” solutions arise, we have to rewrite the first order conditions

L / x i

=

U/

x i

-

p i

< 0 (i= 1,… n) and if

L / x i

=

U/

x i

-

p i

< 0 then x i

= 0.

These conditions, called Kuhn-Tucker conditions are solutions for linear programming. To interpret the latter condition (e.g,. the strict inequality) rewrite it as p i

> MU xi

/

That is, the price exceeds the marginal utility of a good, so none of it is purchased.

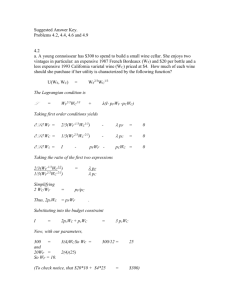

5. Constrained Utility Maximization: Some Examples a. Cobb Douglas Demand Functions . i. General case. To illustrate these points, consider constrained optimization for the Cobb-Douglas utility function, with 2 arguments.

Specifically, let

U(x,y) = x

y

where

+

=1

Define the income constraint as

I - p x x - p y y

To optimize, write the Lagrangian expression

6

L = = x

y

+

( I - p

Taking First order conditions

L / x =

x

-1 y

-

L / y =

x

y

-1

- x x -

p p y x

= p

= y y)

0

0

.

L /

= I-p x x-p y y =

The ratio of the first 2 equations yields

y/

x = p x

/p y

0 or p y y = (1-

)p x x/

Substituting this expression along with p x x into the budget constraint yields

I = p x x + (1-

)p x x/

= p x x/

Solving for optimal x* and y* yields x* = I

/p x y* = I

/p y

Notice what this solution implies. An individual will always spend

percent of his or her income (p x x/I) on good x. Similarly, this individual will spend

percent of his or her income on y (p y y/I).

This constant percentage expenditure of the Cobb-Douglas function makes it very easy to work with. However, it can be limiting. More generally, we would expect the share of income devoted to particular goods to change with income.

Consider first a numerical illustration of the above example. ii. A numerical example. Using the above functional form, suppose that p x

= $.25 , p y

= $1.00 and I = $2.00. Suppose further that

=

=.5. Then x* = 2(.5)/.25 = 4 and y* = 2(.5)/1 = 1

Thus, p x x = $. 25*4 = 1 and p y y = 1(1) =1

Given these optimal choice, U = 4 .5

1 .5 = 2.

- Notice also that

= .5(4) -.5

(1) .5

/.25 = 1. This implies that small changes income will lead to comparable changes in utility. To see this, suppose that income increase to I= 2.1. Then x* = 2.1(.5)/.25 =4.2 and y* =2.1(.5)/1 = 1.05 and U = 4.2

.5

1.05

.5

= 2.1

7

Go back to the I=$2.00, but suppose that p x

increases to $.50. Then x* = 2(.5)/.5 = 2 and y* = 2(.5)/1 = 1

U = 2 .5

1 .5

= 2

.

5 . Thus, with the increase in the price of x, utility falls, but expenditures on x remain unchanged

Thus, p x x = $. 5*2 = 1 and p y y = 1(1) =1.

As a second example, we consider a more general utility function b. CES Utility . CES Demand Now consider an example where expenditures are responsive to economic conditions. Suppose

U(x,y) = x

.5

+y

.5

The Lagrangian expression becomes

L = x 5 +y .5 +

( I - p x x - p y y)

Taking First order conditions

L / x = .5x

-.5 -

L / y = 5y

-.5

-

.

L /

= I-p x x-p y y

= p p x y

=

=

0

0

0

Taking the ratio of the first two equations yields

(y/x)

.5

= p x

/p y,

or, for example, y = (p x

/p y

)

2 x

Substituting into the budget constraint yields

I = p x x + p y

(p x

/p y

)

2 x

Or x* = I/(p x

[1+p x

/p y

]) and y* = I/(p y

[1+p y

/p x

])

Notice here that these demand functions are not constant. Rather they depend on the ratio p x

/p y

, or the relative price of the two goods.

CES with less substitutibility. Consider

U(x,y) = -x .-1 -y .-1

It is easy to show that the first order conditions imply y/x = (p x

/p y

).5

8

Substituting into the budget constraint

Or x* = I/(p x

[1+(p y

/p x

)

.5

]) and y* = I/(p y

[1+(p x

/p y

)

.5

])

These demand functions are less responsive to relative price changes.

C. Indirect Utility Function . As the above examples illustrate, it is often possible to manipulate first order conditions for the optimal values of x

1

, x

2

, … x n

. In general, these optimal values will depend on the prices of all goods and an individual’s income.

That is, x

1

*

= x

1

(p

1

, p

2

,…. ,p n

, I) x

2

* =

.

.x

n

*

= x x

2 n

(p

(p

1

1

, p

, p

2

2

,…. ,p

,…. ,p n n

, I)

, I)

These expressions are demand functions, which illustrate the relationship between a good, own price, the price of complements and substitutes, and Income. We will study these in later chapters. For the time being, insert these back into the original utility function, to yield

Maximum utility =

=

U(x

1*

, x

2*

, …., x n*

)

U( x

1

*

(p

1

, p

2

,…. ,p n

, I), x

2

*

(p

1

, p

2

,…. ,p n

, I)

….. x n

*

(p

1

, p

2

,…. ,p n

, I))

= V(p

1

, p

2

,…. ,p n

, I)

That is, because an individual optimizes utility in light of a budget constraint, we can write the individual an individual’s optimal utility in terms of prices and the income constraint, because these parameters indirectly determine utility. This indirect utility function will be useful later in the text. Of course, if either prices or income change, so, in general, will the level of utility. This indirect expression will be useful later in the course, when, for example, we attempt to evaluate the effects of a change in costs conditions on outcomes.

2. Example Indirect utility and the Cobb-Douglas function. Consider again the

Cobb Douglas function U = x .

y

, subject to the constraint that I = p x

X + p y

Y.

Suppose again that x

=

=.5. The Lagrangian expression is

L = X 1/2 Y 1/2 +

(I- P x

X -P y

Y)

9

With FONC

L /

X =

L /

Y =

L /

=

1/2X

1/2X

-1/2

1/2

Y

1/2

Y

-1/2

-

- p p x y

=

=

I- p x

X - p y

Y =

By the ratio of the first two expressions

0

0

0

Y/X = p x

/p y

.

Solving this expression for Y (or X) and inserting into the budget constraint allows for expression of the individual demand functions

X* = I/2p x

Y* = I/2p y.

Inserting these into the utility function yields our indirect utility

V = (I/2p x

)

1/2

(I/2p y

)

1/2

= I/(2p x

1/2 p y

1/2

)

Now, we can quantify this in terms of observable parameters. For example, in the case where I = 2, p x

= .25 and p y

= 1. V = 2/(2(1/4))

.5

1

.5

)=2

Importantly, by stating utility in terms of the externally observable parameters, it is possible to study explicitly the effects of changes in a parameter on a system

3. The Lump Sum Principle . Let us develop this example a bit more. Consider the effects of a tax that collected $.50 of revenue. This tax could be collected in one of two ways. One option would be to tax income by $.50. Another would be to tax a good, say X by $.25. (Recall that proportional expenditures are constant in a

Cobb Douglas function. The consumer spends 50% of his income on X in this case. At a price of $.25 (s)he consumes 4 units. At a price of $.50 (s)he consumes 2 units.)

An important point in the economics of taxation is that utility falls less with an income tax (a lump sum tax) than with a tax on goods. To see this, observe that with an income tax I falls to 1.5 and

V = 1.5/[2(.25)

.5

(1)

.5

] = 1.5

With an increase in the price of good X, income stays the same, but p x

increases

V = 2/[2(.5) .5

(1) .5

] = 1.41

10

(In your homework, I will give you a problem that asks you to illustrate this notion graphically)

D. Expenditure Minimization. As we pointed out in chapter 2, maximization problems have associated with them “dual” minimization X

E

1 problems. That logic applies to the E

2

E

3 current situation as well. Rather than maximizing utility subject to a, we might vary possible expenditure levels E

1

, E

2

, and E

3

in order to minimize the expenditures necessary to achieve a level of utility U This is illustrated in the panel to the right.

Mathematically, the problem is to minimize total expenditures, E,

U

1

Y subject to a given utility level, U .

E = p

1 x

1

+p

2 x

2

+…. + p n x n

U = U(x

1

, x

2

, …., x n

)

L = p

1 x

1

+p

2 x

2

+…. + p n x n

+

( U - U(x

1

, x

2

, …., x n

))

This problem is solved in the same way as the maximization problem.

Importantly, however, observe that the optimal amounts of x

1

to x n

will depend on the utility level, here U , and the prices p

1

, …p n

. This relationship is termed an Expenditure function :

Minimal Expenditures = E(p

1

,p

2

, …,p n

, U )

In the next chapter we will use this function to analyze optimal responses to price changes.

Example : Expenditure function from the Cobb-Douglas function and

Given E = p x x + p y y

U = x

.5

y

.5

The Lagrangian expression becomes

L = p x x + p y y +

( U -x

.5

y

.5

)

First order conditions can be used to find p x x = p y y

11

precisely as we found before. Expressing the expenditure function in terms of U, p x

and p y

yields x* = E/2p x and y* = E/2p

Inserting these into the utility target yields y

E = U /2p x

.

5 p y

5

Inserting parameters yields E=2.

12