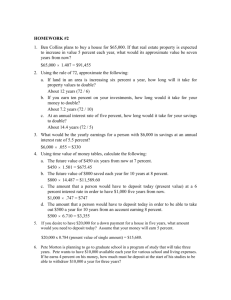

Deposit Interest Calculation Standard

advertisement

Daily Deposit Interest Calculation Standardisation

33-41 LOW ER MOUNT STREE T

DUBLIN 2

Standard for Daily Deposit

Interest Calculation

Requirements Specification

Issued:

May 2007

Updated:

February 2008

Page 111

Version 4

Daily Deposit Interest Calculation Standardisation

Contents

Contents ............................................................................................................................. 2

Introduction ........................................................................................................................ 3

Deposit Interest Calculation Standard ............................................................................. 4

Processing Requirements ................................................................................................. 5

Clearing of Funds ............................................................................................ 6

Bounced Cheque and Unpaid Direct Debit Treatment ................................. 8

Appendix 1 – Worked Example .................................................................... 11

Page 211

Version 4

Daily Deposit Interest Calculation Standardisation

Introduction

Deposit accounts offered by credit unions are typically demand deposit accounts.

Many credit unions do not offer these accounts to their members. The most

common type of deposit account currently offered by credit unions is that which

typically calculates deposit interest in the same way that dividend is calculated on

members shares. Other credit unions utilize a variable deposit interest rate to

calculate the return. Currently there is no standardisation across the credit union

movement in respect of deposit interest calculations. This document specifies

requirements in respect of deposit interest calculations for variable interest rate

deposit accounts.

Minor accounts offered by credit unions in Northern Ireland to under 16’s are

considered to be deposit accounts as such members, under legislation, are not

entitled to hold shares. However, the processing of such deposit accounts is in

line with the processing of regular share accounts and so for the purpose of daily

interest calculations are treated as share accounts accruing dividend points on a

daily basis. See Standard for Daily Accumulation of Dividend Points for Dividend

Calculation for more details.

The purpose of this document is to specify requirements for the calculation

of deposit interest on a daily basis for variable interest deposit accounts.

The Irish League of Credit Unions proposed a motion to BDM 2007 to require all

credit unions to adopt and implement this standard by 1/10/2007 and bring credit

unions more in line with industry norm interest calculations today. This motion

was passed overwhelmingly by the movement.

Page 311

Version 4

Daily Deposit Interest Calculation Standardisation

Deposit Interest Calculation Standard

The proposed standard suggests that deposit interest is calculated on a

daily basis in the same way as loan interest is calculated. Deposit interest

payable (accrued) to the member is calculated daily and lodged to the

members deposit account on an annual basis.

[Int. Payable=(Current Dep Bal. x No. Days x Int. Rate)/(No. Int. Days in Yr x 100)]

The resulting interest payable is rounded in accordance with normal

rounding rules. By performing the full calculation in a single formula

calculation and rounding at the end this minimises rounding errors. For

example with a deposit interest rate of 3% and a deposit balance of

£/€981.10, deposit interest for 4 days is calculated as follows:(981.10 x 4 x 3.0)/(365 x 100)= 0.32255342465.

This is rounded to €/£0.32.

Note:- Deposit interest is capitalised on an annual basis at 30 th

September. ie deposit interest paid in respect of the year closed-off is

added to the year end deposit balance before the new financial year

starts.

Unpaid Deposit Interest due is recorded and accumulated following

transactions on members accounts. These unpaid deposit interest

amounts are added to calculated daily interest accrued values to give

Total Deposit Interest Payable to the member as follows: [ Total Dep Int. Payable = Dep. Int. Accrued + Unpaid Dep. Int. ]

See worked example in Appendix 1.

Note: The remainder of this report refers only to the calculation of

Deposit Interest Accrued, however Total Interest Payable is

obtained using the above formula.

Page 411

Version 4

Daily Deposit Interest Calculation Standardisation

Processing Requirements

Deposit interest payable is calculated on a daily basis and posted to members

deposit account balances annually during the normal end-of year process at 30th

September.

Req 1.0 Daily Deposit Interest Calculation

The system must calculate Deposit Interest Payable on a daily basis

using the following formula:

[Int. Payable=(Curr. Dep Bal. x No. Days x Int. Rate)/(No. Int. Days in Yr x 100)]

Req 1.1 Deposit Interest Calculation Rounding

The systems interest calculation must be rounded as follows: If

greater than or equal to x.xx5, round up to the nearest cent/pence. If

the interest calculation is less than x.xx5, round down to the nearest

cent/pence.

Req 1.2 Total Deposit Interest Payable

The system must calculate the Total Deposit Interest Payable by

adding the unpaid interest accumulated up to the last transaction or

incident on the members deposit account to the interest calculated

for the period since the last transaction or incident on the members

deposit account as follows: [ Total Dep Int. Payable = Dep. Int. Accrued + Unpaid Dep. Int. ]

Req 1.3 Leap Year APR Calculation

The system must calculate interest for a period in a leap year using

the day count formula (Actual/366). Where there is a crossover

interest calculation period from a leap year to a normal year or from

a normal year to a leap year, the interest calculation must be done

for the old and new years separately. The two un-rounded interest

payable amounts must then be added together and rounded after the

addition using normal rounding rules as defined above.

Req 1.4 Interest Rate Changes

When the deposit interest rate changes within an interest calculation

period, the system must calculate the interest calculation for the

period at the old and new interest rates separately. The two unPage 511

Version 4

Daily Deposit Interest Calculation Standardisation

rounded interest payable amounts for the different interest rate

periods must then be added together and rounded using normal

rounding rules as defined above.

There are occasions when a member wishes to close their deposit account midyear before interest has been posted.

Req 1.5 Deposit Account Close-Off

The system must force posting of the unpaid deposit interest

payable to accounts before the final close-off process for the deposit

account. This must result in a deposit interest payable transaction

being created for the total amount of unpaid deposit interest due to

the member in respect of their account. The deposit interest payable

amount must then be transferred to the current deposit account

balance to give the close-off balance to be withdrawn before the

account is finally closed.

Req 1.6 Annual Posting of Deposit Interest Payable

The system must accumulate the deposit interest payable daily on

members deposit accounts and post the interest payable to effect

member balances during the normal end of year process at 30th

September. This end of year process must create interest payable

transactions for the total amount of unpaid deposit interest payable

to each member and must automatically transfer these individual

amounts to effect respective member deposit balances.

Clearing of Funds

Systems and processing must be in place to manage uncleared as well as

cleared funds in accordance with each individual credit union policy.

Consider the situation where a member cheque is received as a deposit

lodgement and subsequently posted against the members deposit account. The

funds associated with cheque received by the credit union may not be cleared by

the banking system for up to 5 days. During the cheque clearing period the credit

union may not be earning deposit interest from their bank in respect of these

funds. The credit union may or may not want to effect the lodgement to the

members deposit balance until the funds have been cleared by the banking

system. Immediate posting of uncleared funds at the credit union will lead to a

deposit interest entitlement for the clearing period before the credit union

receives value for the lodgement made.

Page 611

Version 4

Daily Deposit Interest Calculation Standardisation

Heretofore from a deposit interest calculation point of view, most credit unions

did not distinguish between cleared and uncleared funds as deposit interest was

typically based on a average monthly balance. This calculation frequency and

basis allowed sufficient time for cheques and other funds to be cleared by the

banking system.

With daily deposit interest calculation, credit unions must decide whether or not

they are willing to pay the additional deposit interest cost to members in respect

of members lodging uncleared funds to their accounts.

It is recognised that some credit unions will process cleared and uncleared funds

in the same manner though others may not. If the policy of a credit union is to

treat uncleared funds differently to cleared funds then the credit union IT

processing system must be capable of managing uncleared funds in accordance

with policy.

Req 2.0 Cleared and Uncleared Funds Tracking

IT processing systems must be enabled to identify, track and

manage cleared and uncleared fund transactions.

Credit unions typically offer a standing order loan repayment or lodgement option

to their members in respect of lodgement of funds. In this case funds are

transferred electronically from the members bank account to the credit unions

bank account. Credit unions receive notice of these lodgements(cleared funds)

through their Internet Business Banking package supplied by their bank or

through bank statements received.

Req 2.1 Standing Orders and Exceptions Posting

Following funds received by the credit union to their bank account,

the system must lodge cleared funds in respect of member payments

to credit union bank accounts and these must be posted to the

destination member accounts no later than next day Queries in

respect of unapplied credits must be reported on and followed up the

same day the query arises.

Req 2.2 Funds Clearing Periods

The credit union IT system must record the number of days required

to clear funds in respect of the transaction types to be processed.

These “number of days” values will be used by the IT system in

automatically clearing member funds. When the clearing period for

Page 711

Version 4

Daily Deposit Interest Calculation Standardisation

funds has elapsed, un-cleared funds must then be processed as

cleared funds

Req 2.3 Same Treatment for Cleared and Uncleard Funds

If credit union policy suggests that there is no special treatment for

transactions containing un-cleared funds, then the system must

process such transactions as if the funds were cleared funds

Req 2.4 No Funds Value for Clearing Period

If credit union policy suggest that members will not receive value for

their funds lodged for the clearing period then un-cleared funds

transactions will only be posted and effected to member account

balances next day following the completion of the specified clearing

period for that transaction type. This applies to funds received by

cheque and electronically

Bounced Cheque and Unpaid Direct Debit Treatment

Systems must be capable of efficiently processing the cancellation of bounced

cheques or unpaid direct debit lodgements in accordance with credit union policy.

System must also provide for controlled and automated processing of unpaid

deposit interest adjustments where applicable in respect of lodgements of

uncleared funds.

Req 2.5 Reversal of Bounced Cheques and Treatment of Unpaids

If credit union policy suggest that funds value will be given to

members except for the clearing period in respect of bounced

cheques or unpaid direct debits, the IT processing system must

automatically re-adjust the unpaid deposit interest in respect of

necessary transaction reversals as a result of such bounced

cheques or electronic unpaid direct debits. In these cases the

system must calculate the Deposit Interest Payable in accordance

with this standard as follows: [Dep Int. Adj.={Sum(Adjusted Daily Dep Bals for Cancellation Period x No. Days) x

Int. Rate}/(No. Int. Days in Yr x 100)]

[ Corrected Dep Int.= (Unpaid Dep Int. + Dep Int. Adj.) ]

Page 811

Version 4

Daily Deposit Interest Calculation Standardisation

A worked example is shown in Appendix 1 involving a lodgement of £/€100 made

on 21/9/06 by cheque. The deposit interest payable on 21st was £/€0.85.

Deposit interest continued to accrue on £/€1,150 for two days - 22nd and 23rd.

Notification was received that the cheque lodgement made on 21st bounced. A

deposit interest adjustment correction was made to offset the bounced cheque

lodgement posted two days earlier. A transaction reversal was also effected on

23/9/06. The corrected deposit interest payable is calculated as follows: Dep Int. Adj= {(1150+(-100)) x 2 x3}/(365 x 100) = 0.17260273972

As this is a currency amount it is rounded to £/€0.17 in accordance with rounding

rules.

Corrected Dep Int.= (0.85 + 0.17) = £/€1.02

The corrected Deposit Interest Payable on 23/9/06 following reversal of the

bounced cheque lodgement is £/€1.02.

Similarly, the corrected Deposit Interest Payable on 28/9/06 in respect of the

reversal of a withdrawal is calculated as follows: Dep Int Adj= {(900+200-50) x 1+ (900+200) x 2} x 3/(365 x 100) =

0.26712328767

As this is a currency amount it is rounded to £/€0.27 in accordance with rounding

rules.

Corrected Dep Int.= (1.19 + 0.27) = £/€1.46

The corrected Deposit Interest Payable on 28/9/06 is £/€1.46.

Page 911

Version 4

Daily Deposit Interest Calculation Standardisation

Further Information

Should you have any queries or require further information in relation to

implementing the new standard interest calculation basis contact the League

Name:

Joe Timmons

Email:

jtimmons@creditunion.ie

Telephone:

+353 1 6146968

Page 1011

Version 4

Daily Deposit Interest Calculation Standardisation

Appendix 1 – Worked Example

Deposit

No. of

Interest

Deposit Days

calculatio Deposit

Balance Interest n today

Interest

(Start of Payable (Start of calculation

Date

Day)

Today

day)

yesterday

0.00

0

Sep-11

12 1,000.00

1

0.08

0.00

13 1,000.00

2

0.16

0.08

14 1,000.00

3

0.25

0.16

15 1,050.00

1

0.34

0.25

16 1,050.00

2

0.42

0.34

17 1,050.00

3

0.51

0.42

18 1,050.00

4

0.60

0.51

19 1,050.00

5

0.68

0.60

20 1,050.00

6

0.77

0.68

21 1,050.00

7

0.85

0.77

22 1,150.00

1

0.94

0.85

23 1,150.00

2

1.04

0.94

24 1,050.00

1

1.11

1.02

25 1,050.00

2

1.19

1.11

26

850.00

1

1.26

1.19

27

900.00

1

1.33

1.26

28

900.00

2

1.41

1.33

29 1,100.00

1

1.55

1.46

30 1,100.00

2

1.55

1.64

1

0.09

1.64

Oct-01 1,101.64

2 1,101.64

2

0.18

0.09

3 1,101.64

3

0.27

0.18

4 1,101.64

4

0.36

0.27

5 1,101.64

5

0.45

0.36

6 1,101.64

6

0.54

0.45

7 1,101.64

7

0.63

0.54

8 1,101.64

8

0.72

0.63

9 1,101.64

9

0.81

0.72

9 1,102.45

0

0.00

0.63

9

0

0.00

0.63

0.00

Unpaid

Deposit

Interest @

Deposit

Last

Interest

Txn(included

payable Lodgement/ in Dep Int calc

for today Withdrawal today)

1,000.00

0.08

Cash lodgement

0.08

0.09

50.00

0.25

0.09

0.25

0.08

0.25

Dep Interest for 17th

0.09

0.25

0.09

0.25

0.08

0.25

0.09

0.25

0.08

100.00

0.85

0.09

0.85

0.10

-100.00

1.02

0.09

1.02

0.08

-200.00 Withdrawal 1.19

0.07

50.00

1.26

0.07

1.26

0.08

200.00

1.46

0.09

1.46

0.09

0.00

1.64

0.07

0.00

Annual Deposit

0.09

0.00

Interest Paid

0.09

0.00

0.09

0.00

0.09

0.00

0.09 Dep account closed off

0.00

0.09 mid year

0.00

0.09

0.00

0.09

0.00

0.81

0.00

0

-1,102.45

0.00

0

Interest

Adjustment

Calculation

Reversal of

chq

lodgement

made on

21st

Reversal of

withdrawal

made on

25th

Total Dep Interest due to

member on 9th Oct

Deposit Interest Calculation Formula. Interest rate used is 3%, No of days is 365

[Int. Payable=(Current Dep Bal. x No. Days x Int. Rate)/(No. Int. Days in Yr x 100)]

Page 1111

Version 4