Level 1 Analysis

advertisement

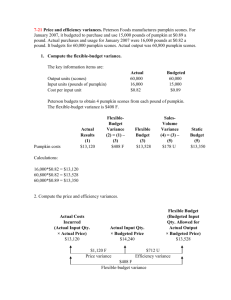

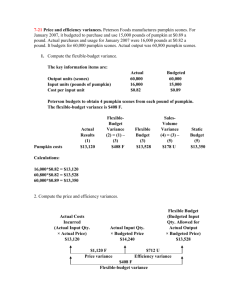

Explain the various factors and considerations used in determining if a variance is overor underapplied Under or Over Applied overhead is the difference between the amount of overhead applied to products and the actual overhead costs incurred during the period. Basically, the overhead variances break the under or over applied overhead down into variances that can be used by managers for control purposes. The sum of the overhead variances equals the under or over applied overhead costs for a period. Furthermore, in a standard cost system, unfavorable variances are equivalent to underapplied over head, and favorable variances are equivalent to Overapplied overhead. Unfavorable variances occur because more was spent on overhead than the standards allow. The critical factor in determining whether a variance has been under or over applied is the denominator level of activity (Machine hours, Direct Labor Hours…etc.); if the denominator level of activity is greater than the standard hours allowed for the output of the period, then the volume variance is unfavorable, signifying an underutilization of available facilities and the opposite is true. Why is this type of analysis important to managers? Variance Analysis is an important element of management by exception. Simply put, management by exception means that the manager’s attention should be directed toward those parts of the organization where plans are not working out for one reason or another. It is also important since the variances reveal that the process is not working in the way it is supposed to work. Thus variances can point out new ways of working as also ensure that work is done efficiently. What are some causes of variances? How should they be addressed? Who should be held responsible for these variances? The causes of variances depend on the type of variance and that also decides who should be held responsible. Material Variances – Material variances could be Price Variance – Price variance is if the actual price of the material is different from the standard price. The variances could be due to lower quality purchase of material or taking quantity discount through higher purchase. If materials of higher quality are purchased at a higher price, the purchasing manager is held responsible for price variance. Quantity Variance – This arises if the material used is different that the standard quantity. Possible causes could be either poor quality of higher quality material. Unforeseen breakdown of machinery may also result is quantity variance. The production manager is held responsible for quantity variance Labor Variance – Labor variance could be Rate Variance – The rate paid to labor is different than the standard rate. The reason could be that either lower of higher skilled labor is used. At time labor may be in short supply and so higher wages may need to be paid. If some overtime is done, than also higher wages need to be paid. The human resources manager would be held responsible for rate variance. Efficiency Variance – This arises if the labor time used is different than the standard time. The reason could be lower skilled workers are used or there are unscheduled breakdowns. The production manager would be held responsible for efficiency variance Variable Overhead Variance Variable Overhead Spending Variance - This variance measures the differences in price of the resources used in overhead, and also includes elements of waste. The waste portion of the variance is most directly controllable by plant management. The price portion may or may not be controllable by management, depending on the nature of the item involved. That is, electricity rates normally would not be controllable by management, whereas prices paid for indirect materials might be controllable. Variable Overhead Efficiency Variance – This depends on the base used and is usually labor hours and this variance moves in the same way as the labor efficiency variance and should be the responsibility of the person who has the responsibility of labor efficiency variance. All variances either favorable or unfavorable need to be investigated. A threshold may be fixed at say 5% and all variances above this should be investigated. The causes of the variances should be ascertained and the processes changed so as to ensure that the variances do no recur. If it is found that variances are due to incorrect standards in which case the standards themselves need to be changed. 7-21 Price and efficiency variances. Peterson Foods manufactures pumpkin scones. For January 2007, it budgeted to purchase and use 15,000 pounds of pumpkin at $0.89 a pound. Actual purchases and usage for January 2007 were 16,000 pounds at $0.82 a pound. It budgets for 60,000 pumpkin scones. Actual output was 60,800 pumpkin scones. 1. Compute the flexible-budget variance. The key information items are: Output units (scones) Input units (pounds of pumpkin) Cost per input unit Actual 60,800 16,000 $0.82 Budgeted 60,000 15,000 $0.89 Peterson budgets to obtain 4 pumpkin scones from each pound of pumpkin. The flexible-budget variance is $408 F. Pumpkin costs Actual Results (1) $13,120 FlexibleBudget Variance (2) = (1) – (3) $408 F Flexible Budget (3) $13,528 SalesVolume Variance (4) = (3) – (5) $178 U Static Budget (5) $13,350 Calculations: 16,000*$0.82 = $13,120 60,800*$0.82 = $13,528 60,000*$0.89 = $13,350 2. Compute the price and efficiency variances. Actual Costs Incurred (Actual Input Qty. × Actual Price) $13,120 Actual Input Qty. × Budgeted Price $14,240 $1,120 F Price variance Flexible Budget (Budgeted Input Qty. Allowed for Actual Output × Budgeted Price) $13,528 $712 U Efficiency variance $408 F Flexible-budget variance 3. Comment on the results in requirements 1 and 2. The favorable flexible-budget variance of $408 has two offsetting components: (a) Favorable price variance of $1,120––reflects the $0.82 actual purchase cost being lower than the $0.89 budgeted purchase cost per pound. (b) Unfavorable efficiency variance of $712–-reflects the actual materials yield of 3.80 scones per pound of pumpkin (60,800 ÷ 16,000 = 3.80) being less than the budgeted yield of 4.00 (60,000 ÷ 15,000 = 4.00). (The company used more pumpkins (materials) to make the scones than was budgeted.) One explanation may be that Peterson purchased lower quality pumpkins at a lower cost per pound. How can determining the causes of these variances help the company improve? Determining the causes of variances would help the company improve as managers’ attention could be focused on problematic areas, if for example materials of higher quality are purchased at a higher price, such price increase should be taken into account when preparing the budget for the next period. If lower quality materials have been purchased, the purchasing manager should be advised not to use lower quality materials as this would result in a lower product quality. In the case of Quantity Variances could be a result from an unexpected machinery breakdowns, for example, hence managers would need to put a maintenance schedule for the machines to avoid such unpleasant problems. In the case of an Unfavorable Efficiency Variance which mostly result from hiring unskilled workers, management can start arranging training courses for such unskilled labor so as they achieve the company’s standards In short, all variances either favorable or unfavorable need to be investigated. A threshold may be fixed at say 5% and all variances above this should be investigated. The causes of the variances should be ascertained and the processes changed so as to ensure that the variances do no recur. If it is found that variances are due to incorrect standards in which case the standards themselves need to be changed. 7-18 Flexible-budget preparation and analysis. Bank Management Printers, Inc., produces luxury checkbooks with three checks and stubs per page. Each checkbook is designed for an individual customer and is ordered through the customer’s bank. The company’s operating budget for September 2007 included these data: Number of checkbooks 15,000 Selling price per book $20 Variable cost per book $8 Fixed costs for the month $145,000 The actual results for September 2007 were: Number of checkbooks produced and sold 12,000 Average selling price per book $21 Variable cost per book $7 Fixed costs for the month $150,000 The executive vice president of the company observed that the operating income for September was much less than anticipated, despite a higher-than-budgeted selling price and a lower-than-budgeted variable cost per unit. As the company’s management accountant, you have been asked to provide explanations for the disappointing September results. Bank Management develops its flexible budget on the basis of budgeted peroutput-unit revenue and per-output-unit variable costs without detailed analysis of budgeted inputs. 1. Prepare a level 1 analysis of the September performance. Level 1 Analysis Actual Results (1) 12,000 a $252,000 d 84,000 168,000 150,000 $ 18,000 Units sold Revenue Variable costs Contribution margin Fixed costs Operating income Static-Budget Variances (2) = (1) – (3) 3,000 U $ 48,000 U 36,000 F 12,000 U 5,000 U $ 17,000 U Static Budget (3) 15,000 c $300,000 f 120,000 180,000 145,000 $ 35,000 $17,000 U Total static-budget variance 2. Prepare a level 2 analysis of the September performance. Level 2 Analysis Units sold Revenue Variable costs Contribution margin Fixed costs Operating income Actual Results (1) 12,000 a $252,000 d 84,000 FlexibleBudget Flexible Variances Budget (2) = (1) – (3) (3) 0 12,000 b $12,000 F $240,000 e 96,000 12,000 F 168,000 150,000 24,000 F 5,000 U $ 18,000 $19,000 F Sales Volume Static Variances Budget (4) = (3) – (5) (5) 3,000 U 15,000 c $300,000 $60,000 U f 120,000 24,000 F 144,000 145,000 36,000 U 0 180,000 145,000 $ (1,000) $36,000 U $ 35,000 $19,000 F $36,000 U Total flexible-budget Total sales-volume variance variance $17,000 U Total static-budget variance a 12,000 × $21 = $252,000 d 12,000 × $7 = $ 84,000 b 12,000 × $20 = $240,000 e 12,000 × $8 = $ 96,000 c 15,000 × $20 = $300,000 f 15,000 × $8 = $120,000 3. Why might Bank Management find the level 2 analysis more informative than the level 1 analysis? Explain your answer. Level 2 analysis provides a breakdown of the static-budget variance into a flexiblebudget variance and a sales-volume variance. The primary reason for the staticbudget variance being unfavorable ($17,000 U) is the reduction in unit volume from the budgeted 15,000 to an actual 12,000. One explanation for this reduction is the increase in selling price from a budgeted $20 to an actual $21. Operating management was able to reduce variable costs by $12,000 relative to the flexible budget. This reduction could be a sign of efficient management. Alternatively, it could be due to using lower quality materials (which in turn adversely affected unit volume).