Module1.2

advertisement

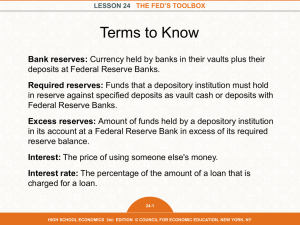

Purposes of a Central Bank • Supervise a nation’s money supply and payments system. • Act as the chief regulator of the nation’s financial institutions • Be “lender of last resort” when financial system has liquidity problems. • Implement nation’s monetary policy (setting interest rates, controlling money supply, and so forth). • Act as the national government’s “fiscal agent” (i.e. depository bank) 1 Central Banks of U.S. • Bank of the United States 1791-1811 • Second Bank of the United States 1816-1832 Free Banking Era 1837-1863 National Banking System Era 1863-1914 • Federal Reserve System 1914-present First two banks failed because of (a) a general distrust in centralized power, (b) too many regions of country felt they weren’t being treated fairly. 2 Banknote 3 What is a Banknote? • In U.S. past, various private banknotes served as money as they were supposed to be redeemable for bullion on demand. • Could take gold, silver, U.S. government bond, or another bank’s banknotes to a bank. (a) Get in exchange banknotes from the current bank, or (b) leave amount in bank as a demand deposit (denominated in banknotes from the current bank). • A loan from the bank came in the form of banknotes from that bank. • Today, all paper money consists of “banknotes” issued by a nation’s central bank. 8/27 4 No Central Bank 1832-1914 • Banknotes carried the default risk of the bank that issued it. • What a good cost depended on the banknote used to pay for it. • At one time, there were 15,000 different banks issuing banknotes. • Discount books were published by dealers who dealt in banknotes listing what they would pay for a given banknote. • The different banknotes made commerce difficult. 5 Free Banking Era 1837-1863 • Federal legislation in 1837 removed restraints on banking. • Money supply was unstable during era No standard currency, only various private banknotes “Hard currency” (gold/silver) much preferred No coordinated payments system • All banks became state-chartered and unregulated No deposit insurance or capital requirements No supervision over lending or accounting practices Many financial shenanigans (bogus banknotes, unwillingness to redeem, etc.) Frequent bank failures 6 National Banking System Era 1863-1914 National Banking Acts of mid-1860s • Purpose was to strengthen the banking system, to try to make all banks federally chartered, and move toward a more uniform currency. • State chartered banks had to pay 10% annual tax on their banknotes, but began to focus on checking accounts • Federally chartered “National Banks” could issue banknotes without being taxed. But must be printed by the U.S. Mint to prevent counterfeiting. • Banknotes had to be backed by U.S. government bonds. • Banks had to maintain minimum reserve requirements and submit to periodic bank examinations under auspices of Comptroller of the Currency. 7 Meaning of the Term “Reserves” The term “reserves” refers to the proportion of deposits that are not used to buy financial claims or lent out to clients. i.e., the money the bank has immediately available to meet withdrawal requests. 8 National Banking System Era Problems “Run” on a bank (everybody attempts to withdraw at once). Pyramiding of reserves. Banks were allowed to count deposits at other banks as reserves. Thus, a “run” on one bank could result in a “run” on others -- contagion. Call loans. Typical of loans during this era. Were due when “called in” by the bank. Banks low on reserves called in loans. Caused borrowers to draw down their own deposits or default. Caused more bank illiquidity and more “calls.” Bank panics would spread, dragging economy into recession. 9 Boom/Bank Panic/Recession Cycle • Economy starts improving. Loan demand starts increasing. System builds upon itself. Eventually banking system makes too many bad loans. • A few run low on cash. Since accounts not insured, people panic. • Everybody runs to get their money out of bank. Makes crisis worse. Banks call in loans. • Disrupts businesses. Employees laid off. They take savings out of bank. Bank’s cash situation gets worse. Banks fail. Country goes into recession. • Major panics since Civil War: 1873, 1893, 1907, 1930-32 10 Panic of 1907 • Stock market fell close to 50% • Contraction of liquidity by a number of New York City banks caused a loss of confidence among depositors • Bank runs across the country (despite most banks being solvent) • Was no central bank to inject liquidity • Bank failures. • From repeated boom/bank panic/recession cycles, people began to learn. Panic of 1907 was last straw. • Commission charged to investigate the crisis proposed solution that led to the creation of Federal Reserve System. 11 Bank Insolvency • When a bank’s liabilities exceed its assets • Whether bank gets shut down by regulators is a judgment call • Depends upon whether situation is temporary or hopeless • So a bank may fail for either reasons of illiquidity or insolvency 12 Federal Reserve Act of 1913 • Federal Reserve Act of 1913 (passed in Dec but went into effect in 1914) designed to to create a central banking system designed to assure that no region or group had an unfair say. to provide for an “elastic” standardized currency in the form of Federal Reserve Notes that could be adjusted in amount to meet the needs of a changing economy. to serve as lender of last resort to keep banks liquid. improve payments system (check clearing). provide more vigorous supervision of banks. 13 Today’s Federal Reserve System • 12 district Federal Reserve Banks • About 3,000 member commercial banks • 7-member Board of Governors • 12-member Federal Open Market Committee (FOMC) • All kinds of advisory committees 14 12 District Federal Reserve Banks 1 to 12, or A to L 15 7-Member Board of Governors • 7 Governors appointed by President, confirmed by Senate • No two Governors from same Federal Reserve District • Governors have staggered 14-year terms. • Governors’ terms are nonrenewable. • Which Governor is to be Chairman is determined by the President • Chairman has 4-year term and may be reappointed (Alan Greenspan since 1987-2006, followed by Ben Bernanke 20062014, now Janet Yellen). • When new Chairman is named, old one leaves (regardless of time left in underlying appointment as a Governor) . 16 About 3,000 Member Commercial Banks All nationally-chartered banks are members of the Fed. 17% of state-chartered banks also belong (for 36% of all banks, but 76% of all banking assets) Dependent upon assets, all member banks must own stock in the Federal Reserve Bank of its district. Just get 6% dividend ($1.4 billion in total in 2009). After dividends, rest of the profits distributed to the Federal Government (see chart next slide). Each District Bank has a 9-member board: • 6 elected by member banks in district, 3 appointed by the Board of Governors • with the restriction 3 from banking, 3 from business, 3 to represent the public. 8/29 17 Distributions (in billions) 18 About 3,000 Member Commercial Banks Membership advantages prestige stock get to vote but not as important as in past. Fed services (such as, payment system) now available to nonmember banks for a fee. Nonmember banks still have to post reserves, but done at a member bank. Fed regulates all depository institutions without regard to membership. 19 12-Member FOMC FOMC has 12 members (8 permanent, 4 rotating) • The 7 Governors are permanent members • President of FRB of New York has a permanent seat (because FRB of NY carries out FOMC’s open market directives) • Presidents of 4 other FRBs rotate through 1-year terms • Chairman of Board of Governors is Chair of the FOMC • FOMC meets 8 times per year 20 FOMC Meeting 21 FOMC • Decides when and how much to expand or contract money supply. • Instructs FRB of New York to conduct open market operations, which involve buying and selling of US Government and agency securities. • Works mostly with primary approved dealers. • Buying securities increases the money supply, selling decreases money supply. 22 Primary Approved Dealers Bank of Nova Scotia, New York Agency BMO Capital Markets Corp. BNP Paribas Securities Corp. Barclays Capital Inc. Cantor Fitzgerald & Co. Citigroup Global Markets Inc. Credit Suisse Securities (USA) LLC Daiwa Capital Markets America Inc. Deutsche Bank Securities Inc. Goldman, Sachs & Co. HSBC Securities (USA) Inc. Jefferies LLC J. P. Morgan Securities LLC Merrill Lynch Mizuho Securities USA Inc. Morgan Stanley & Co. LLC Nomura Securities International, Inc. RBC Capital Markets, LLC RBS Securities Inc. SG Americas Securities, LLC UBS Securities LLC. When Fed buys securities, credits the dealer’s reserves at the Fed. When Fed sells securities, debits the dealer’s reserves at the Fed. 23 Elaborate System of Checks and Balances 9/3 24 Functions of the Federal Reserve • Sets reserve requirements • Propose discount rates • Regulates banking institutions • Holds reserve balances • Regulates consumer finance • Lends through discount window • Oversees district FRBs • Furnishes currency • Transfers funds among dep institutions • Handles US Treasury bank account • Specifies open market operations • Set Fed Fund target rate • Decides on discount rates 25 • Carries out open market operations Regulatory Responsibilities of the Fed 26 Independence of the Fed • Created by Congress, not under its control, but gets a lot of pressure. • Governors appointed by, but not answerable to President Government has no “power of the purse” as Fed is very profitable • • Fed operates this way because monetary policy has historically been a non-partisan issue • An independent Fed can take necessary but unpopular steps • Government generally content with Fed independence, can always blame the Fed when economy falters 27 Central Bank Independence vs. Inflation 28 Fed Balance Sheet (in millions), Dec 2006 Assets Gold & Coin Loans to depository institutions Repurchase agreements US Treasury securities Liabilities & Capital 14,037 488 36,000 778,938 Agency securities 0 Foreign currency 0 Other 44,431 873,894 Federal Reserve Notes Rev Repurchase agreements 782,733 32,126 Deposits Depository inst balances US Treasury 12,772 4,820 Other 10,712 Capital 30,731 873,894 29 Liabilities and Capital • Depository institution balances (reserves). Depository institution balances are kept at the Fed to meet required reserves (RR). Relationships: RR k (DEP ) T R balance at F ed vault cash TR RR ER where TR is total reserves, ER is excess reserves, DEP is institution’s total deposits, and k is a “simplistic” reserve requirement • Before crisis of 2007, balances at Fed (for meeting RR and clearing checks) earned no interest, but now they do (.25%). 30 Reserve Requirements (RR) 0 to $10.7 milllion $10.7 million to $55.2 million Over $55.2 million 31 Borrowing at the “Discount Window” • Borrowing from the Federal Reserve Bank’s lending facility, i.e., borrowing at the “discount window,” which is done at district FRB, increases money supply. • Part of Fed’s “lender of last resort” function. • Borrowing at “discount window” done for short term (usually overnight). In normal times, only done occasionally. • Historically, discount window borrowing has carried stigma of bank failure. Banks are wary of “discount window scrutiny.” • All borrowings must be fully collateralized with high-quality securities (usually Treasuries and agency securities). • Fed actually extends three types of credit: primary, secondary, seasonal. Primary rate is also known as the discount rate. 6 years ago: primary 5.75%. Secondary usually 0.50-1.00% higher. Seasonal is for vacation and agricultural areas. Currently: primary 0.75%, secondary 1.25%. 32 Capital Adequacy In addition to reserve requirements, Reserves/Deposits ≥ “10.7/55.2” calculation a bank must satisfy a capital adequacy ratio Capital/“Loans” ≥ h% where h is from 6 to 12, depending on bank. Also (this is new), people who start a bank have to buy stock in the bank (creates paid-in capital entry on balance sheet), i.e., owners must have skin in the game. 33 Things for Sure To Know for Quiz Know everything on all slides of Module 1.1 and up to this slide of Module 1.2. Study all End-of-Chapter Problems and Solutions. “10.7/55.2” schedule. Know how to multiply large numbers by small numbers. Set calculator so can do 6 places to right of decimal point. Friday and Monday 2:00-3:30pm accessibility. Never hurts to send email saying you are coming. 34 Securitization “Simplistic” Example: A bank creates a trust, ie, special purpose vehicle (SPV). Then lends SPV money to buy many loans of a particular type. Go into a pool. SPV then sells bonds, structured into tranches, to investors to pay back bank with proceeds. Loans in pool pay interest and make principal repayments, which flow through to service the bonds and pay them off. Bank makes money two ways: (1) annual fees for operating the SPV, (2) selling the bonds for more than it cost to buy the loans. 35 Mortgage Backed Security (MBS) In simplest form, an MBS is a security whose cash flows are derived from a pool of mortgages. Two types of MBSs: mortgage bonds (created from a pool of mortgages) CDOs (created from a pool of mortgage bonds) MBSs can get extremely complicated. ABS (asset backed security) is same as MBS but cash flows are from a pool of home equity loans, auto loans, student loans, credit card receivables, . . . Now over $1.2 trillion in student loans (but not all have been securitized, i.e., made into ABSs). 36 Repos & Reverse Repos on Fed Bal Sheet Used by Fed for temporary adjustments to money supply. Repurchase agreements. Securities sold by dealers under agreement to repurchase on a certain date at a certain price. (adds reserve balances to the banking system) Reverse repurchase agreements. Securities purchased by dealers under agreement to resell back on a certain date at a certain price. (drains reserve balances from the banking system) repo -- economic equivalent of a collateralized loan reverse repo -- economic equivalent of collateralized borrowing 37 Repos & Reverse Repos on Fed Bal Sheet Repurchase agreement (dealer borrows from Fed) Fed buys securities from dealer for X Dealer repurchases securities from Fed for X+interest Reverse repurchase agreement (dealer loan to Fed) Fed sells securities to dealer for X Fed repurchases securities from dealer for X+interest Repos are used all over the financial world. Need to study repos hard. It is called a repo or reverse repo depending upon how it looks to a dealer. 38 Multiplier 1 L oan M ultiplier 1 k Example. Assume banking system fully loaned up, “simplistic” k = 20%, and money supply is increased by 5,000. If banking system proceeds to again become fully loaned up, total loans will increase by how much? answer 20,000 Reserves will increase by how much? answer 5,000 39 Multiplier Effect (assume “simplistic” k = 20%) week = 0 5,000 deposit (say, money Assets Liabilities from abroad) loans 4,000 5,000 deposits reserves 1,000 week= 1: new loans create 4,000 more in deposits Assets Liabilities loans 7,200 9,000 deposits reserves 1,800 week=2: new loans create 3,200 more in deposits Assets Liabilities loans 9,760 12,200 deposits reserves 2,440 40 Banking System Getting Fully “Loaned Up” week=3: new loans create 2,560 more in deposits week=4: new loans create 2,048 more in deposits week=5: new loans create 1,638 more in deposits Assets Liabilities loans 11,808 14,760 deposits reserves 2,952 Assets Liabilities loans 13,446 16,808 deposits reserves 3,362 Assets Liabilities loans 14,757 18,446 deposits reserves 3,689 41 Banking System Getting Fully “Loaned Up” week=6: new loans create _____ more in deposits week=7: new loans create _____ more in deposits . . . week = infinity Assets loans reserves Liabilities deposits Assets loans reserves Liabilities deposits . . Assets Liabilities loans 20,000 25,000 deposits reserves 5,000 42