Introduction to CM

advertisement

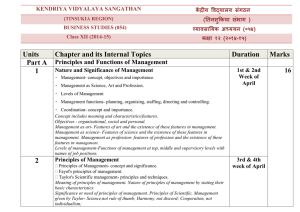

Cost Management Introduction Learning Objectives 1. Similarities and differences between financial accounting and cost accounting 2. Cost accounting’s support to MA & FA 3. Business functions in the value chain 4. Dimensions of performance from customer’s perspective 5. Planning & control decisions of managers Learning objectives 6. Different roles of management accounting 7. Guidelines followed by management accountants 8. Management accounting & organisation structure 9. Professional ethics & MA Limitations of FA • • • • • • • No operating details of particular departments Does not ensure control over material use; does not help in wastage avoidance Costs are not assigned to products, departments, divisions, etc. No standards for comparison Loss is not analysed taking idle time, defective material, etc. Does not help in pricing decisions No information for managerial decisions such as shut down or continue, deciding about product-mix, buy or manufacture, etc. Management accounting • Extension of managerial aspect of cost accounting. • Uses tools of both financial a/c & cost a/c for decision making and control. • Cost accounting- cost control is of prime importance. • Management accounting- primary emphasis is on decision making (Mgt. a/c employs many techniques from OR, statistics, etc.) GROUNDS OF DIFFERENCE FINANCIAL ACCOUNTING COST ACCOUNTING Purpose B/S, P&L A/C, CFS General Purpose Cost Information for planning, decision making & control Special purpose: Different costs for different purposes For Whom? External Users Internal Users Coverage Total organisation Segmental (product, process, job, depart., etc.) Control Does not provide for control of Provides elements of cost Principles GAAP Need driven Need Statute demands Optional, need driven except when cost a/c record rules provide Reporting Time Accounting Year Need based (planning and control) Basis measurement of Monetary terms Use of standards No standards to performance and efficiency Information Historical Could be physical also (like labour hours, machine hours,etc.) compare Standards are used evaluate Projects past into future Strategic decisions & MA Strategy formulation Building resources and capabilities Implementing strategy Building resources and capabilities • Current assets • Long term productive assets • Intangibles Planning and Controlling Management Accounting System Planning Budgets Control Accounting System Performance Evaluation Performance Reports Feedback Management Decision Planning and Controlling What is planning? Setting goals Predicting results Deciding how to attain goals Planning and Controlling What is control? Deciding and taking actions Deciding on performance evaluation and feedback Roles of MA- Problem solving This involves comparative analysis for decision making. This role asks: Of the several alternatives available, which is the best? Scorekeeping This involves accumulating data and reporting reliable results to all levels of management. This role asks: How is the business doing? Attention Directing This involves helping managers properly focus their attention. This role asks: Which opportunities and problems should be emphasized first. Attention directing should focus on all opportunities to add value to an organization, not just cost-reduction opportunities. Cont…. • Strategic decisions and planning decisions: problem solving role is most important • Control decisions: the later two roles are important Key Themes in Management Decision Making Customer Focus Value Chain and Supply Chain Analysis Key Success Factors: Cost and Efficiency, Time, Quality, Innovation Continuous Improvement and Benchmarking Customer Focus continue investing sufficient (but not excessive) resources in customer satisfaction such that profitable customers are attracted and retained. Value Chain and Supply Chain Analysis 1. Treat each of the business functions in the value chain as an essential and valued contributor. 2. Integrate and coordinate the efforts of all business functions in addition to developing the capabilities of each individual business function. Key Success Factors operational factors that directly affect the economic viability of the organization Cost –continuous pressure to reduce costs. Quality – customers are expecting higher levels of quality Key Success Factors Time – organizations are under pressure to complete activities faster and to meet promised delivery dates more reliably. Innovation – continuing flow of innovative products or services is a prerequisite to the ongoing success of most organizations. Continuous Improvement and Benchmarking Continuous improvement by competitors creates a never-ending search for higher levels of performance within many organizations. Value Chain The term “value chain” refers to the sequence of business functions in which usefulness is added to the products or services of an organization. The term “value” is used because as the usefulness of the product or service is increased, so is its value to the customer. MA provides decision support across value chain Value Chain R&D Design Production Management Accounting Marketing Distribution Service MA’s support to managers- Key Guidelines 1. Cost-benefit approach 2. Full recognition of behavioral as well as technical considerations 3. Using different costs for different purposes Partial Organization Chart, Manufacturing Company President Line Function Staff Function Production Vice-President Financial VicePresident Production Supervisor Machining Foreman Assembly Foreman Controller Internal Audit Cost Financial Treasurer Systems Ta x Current Factors Affecting Cost Management A. Global Competition • demand for more cost information but also for more accurate information quickly Current Factors Affecting Cost Management B. Growth of the Service Industry service sector of the economy has increased in importance deregulation of many services has increased competition in the service industry Current Factors Affecting Cost Management C. Advances in Information Technology Computer aided operations – information accumulation and supply of information to management instantaneously. The emergence of e-commerce allowing buyers and sellers to come together electronically Current Factors Affecting Cost Management D. Advances in Management Environment Just-in-time manufacturing Computer-integrated manufacturing Current Factors Affecting Cost Management E. Customer Orientation value to the customer for establishing competitive advantage Companies to compete in technology, manufacturing, speed of delivery and response Current Factors Affecting Cost Management F. New Product Development high proportion of production costs are committed during the development and design stage cost control- use of target costing and activitybased management Current Factors Affecting Cost Management G. Total Quality Management Continual improvement and elimination of waste A philosophy of total quality management Current Factors Affecting Cost Management H. Time as a Competitive Element • Time is the crucial element in all phases of the value chain. • Decreasing non-value-added time appears to go hand-in-hand with increasing quality