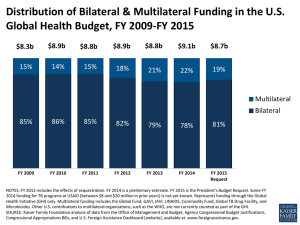

Examinations and Collection Abroad

advertisement

Examinations and Collection Abroad Marian Bette CIAT correspondent Netherlands Tax and Customs Administration Buenos Aires, 24 april 2013 1 Content of presentation • International cooperation between tax administrations • International Tax Audits • International Tax Collection International Cooperation Statutory framework for international cooperation - national legislation - bilateral treaties and TIEAs - multilateral regulations Organizing international cooperation - 1 central liaison office: competent authority for exchange of information on taxes and collection - 1 Expert Group International Tax Auditing - Expert EoI contactpoints in tax offices 3 International tax audits • • • • • Statutory building blocks Assistance in person/presence of officials abroad Simultaneous tax audits International Frameworks Bilateral agreements with Belgium and Germany Multilateral Controls in EU Joint audits Bilateral agreements Belgium & Germany • Intensify cooperation with neighbouring countries • CA-mandated officials Multilateral Controls (EU) Key elements - Memberstates agree - coordinated financial control - of one or more related taxable persons - control has complementary or common interest Organization framework - MLC coordinator in each Member state - audits carried out by local auditors in conjunction with CA 6 MLC: Steps Key steps - initiative - start up meeting: strategy -> intra community control plan - execution of the audit - concluding meeting -> joint report Key goals - ensure correct tax (EU and national legislation) - MLC is part of standard audit activity - share knowledge about audit practices - test and improve MLC procedures 7 MLC: Facts and Figures NL participates in 20 new MLCs annually (65% initiative of NL) 2011 topics: internet services, alcoholic beverages, carrousel fraud, real estate, migrant labour and second hand cars 2011 revenue: 583 million euro in tax & 18 million euro in penalties Revenue for Netherlands: 68 million 5 cases no Dutch assessments but valuable EoI 8 H M Revenue & Customs Federale Overheidsdien FINANCIEN Finanzamt für Großbetriebsprü ung MLC: Lessons learnt from practice Taxes VAT Income Tax Behavioural effects Decrease in use of avoidance schemes Structural contacts between Tax Auditors Other effects Direct line of communication improves quality of exchanged info 450 requests for information with average reply in 3 weeks 280 spontaneous exchanges of information & guaranteed use 10 Taking simultaneous audits outside Europe 11 Joint audits (FTA) Key elements - two or more countries joining: single audit team - examine crossborder transactions/issues - joint presentations to & shares information with countries - CA on the team Main objectives - added value - common or complementary interest - domestic audit not sufficient: obtain a complete picture 12 Joint audit: Steps Key steps - preparation process - selection process - planning meeting - auditing process - joint information requests - examinations - meetings with taxpayer - final stages : concluding meeting and joint report 13 International tax audits - recap • Completing the puzzle • Linking CA and Auditor expertise • Agreement on procedural steps • Awareness legalities • Communication, communication, communication! Collection abroad Policy Policy: incorporate broad mutual assistance provisions on the collection of taxes in all relevant international instruments & apply them in practice Framework • Broad tax collection assistance under the EU Directive 2010/24/EU (as of 1-7-2013: 28 EU members) • Non EU countries: 25 DTC’s with tax collection provision • Multilateral convention (reservations on tax collection) Effective cooperation in collection Considerations: workload and reciprocity Solution: - step by step approach - direct approach 16 Dutch farmers abroad with tax debts 17 Case in brief 1. 2. 3. Work with treaty partner: agreement on permission to directly contact tax debtors Extra measure: contact with banks and help for tax debtors And in the Netherlands: passport alert and threat of imprisonment Results - More than 90% of the farmers paid their taxes - Regarding the others, further assistance from treaty partner - Finally, with some exceptions, all have paid 18 Lesson learnt : be creative and innovative Benefit: not over-burden treaty partner This approach may be viable if there is a huge imbalance in factual reciprocity it is about a high number of tax payers with substantial debts it is not possible for the treaty partner to collect by applying less burdensome collection measures 19 GRACIAS!